By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

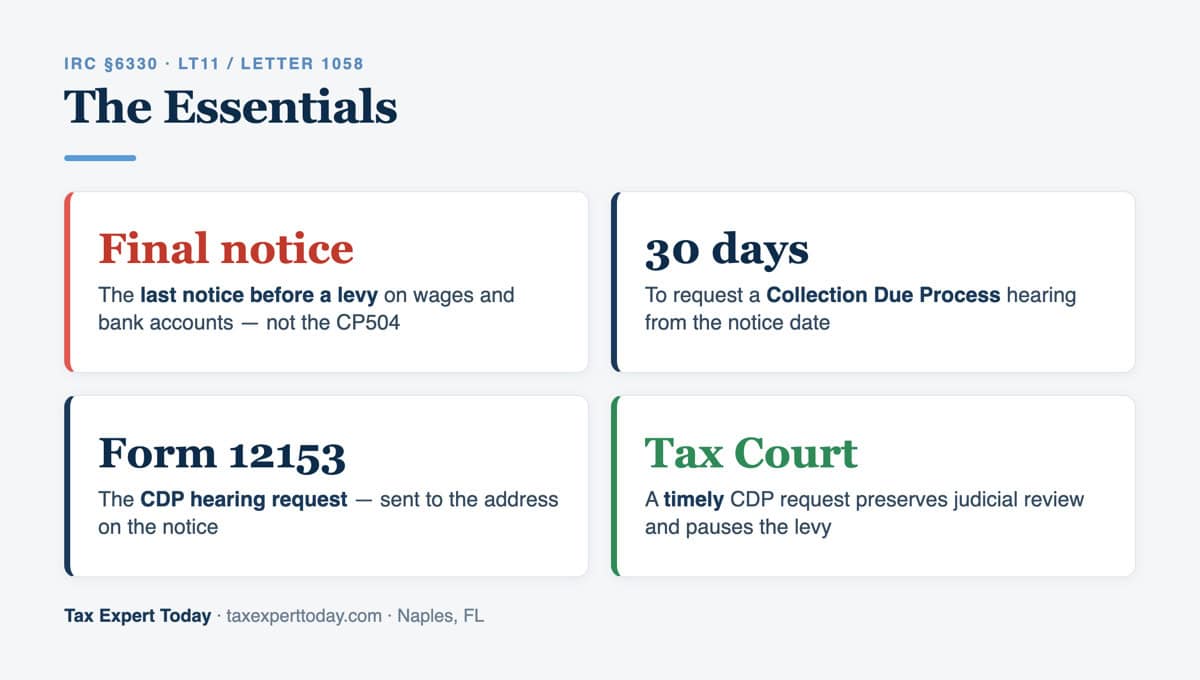

Quick Answer: IRS Letter 1058 (and its near-identical counterpart, the LT11) is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. It is the last notice the IRS sends before it can levy — seize wages, bank accounts, and other property — under IRC Section 6330. It gives you 30 days to request a Collection Due Process (CDP) hearing using Form 12153. Filing a timely request pauses levy action and preserves your right to have the decision reviewed by the U.S. Tax Court.

Published: June 2026

An LT11 or Letter 1058 is the most serious balance-due notice the IRS sends, because it is the one that unlocks enforced collection. It is the end of the notice sequence that begins with the CP14 notice and escalates through the reminder notices and the CP504. But it is not the same as a levy — it is a 30-day warning that comes with a powerful taxpayer right: the Collection Due Process hearing. This 2026 guide explains what the notice means under Internal Revenue Code Section 6330, how to request a CDP hearing on Form 12153 before the deadline, what happens if the 30 days lapse, and what you can actually raise at the hearing.

What Is IRS Letter 1058 / LT11?

Letter 1058 and the LT11 are both the IRS Final Notice of Intent to Levy and Notice of Your Right to a Hearing, sent under IRC Sections 6330 and 6331(d) before the IRS may seize property to collect an unpaid balance. The two are functionally the same notice: the LT11 is typically issued by the IRS Automated Collection System, while Letter 1058 is usually issued by a Revenue Officer assigned to the case. Both carry the same legal effect — they start the 30-day clock and trigger the right to a CDP hearing.

The notice tells you the IRS intends to levy if the balance is not resolved, lists the tax periods and amount owed, and explains your hearing rights. Receiving it means the account has reached the final stage of administrative collection. After the 30-day window closes without a hearing request or a resolution, the IRS may levy wages, bank accounts, and certain other assets, and may file a Notice of Federal Tax Lien. The notice is the point at which acting quickly matters most.

How Is an LT11 Different From a CP504 Notice?

The CP504 is labeled a notice of intent to levy but is not the final notice, while the LT11 / Letter 1058 is the final notice that actually authorizes a levy on wages and bank accounts after 30 days. This distinction is the one taxpayers most often get wrong, and it controls how urgent the response is. The table below compares the two.

| Feature | CP504 | LT11 / Letter 1058 |

|---|---|---|

| Stage | Intermediate notice of intent to levy | Final notice of intent to levy |

| What it can reach | State tax refund only | Wages, bank accounts, and other property |

| CDP hearing right | No | Yes — 30-day window under §6330 |

| Authority | IRC 6331(d) | IRC 6330 and 6331(d) |

Because the LT11 / Letter 1058 is the notice that carries the hearing right, it is the one with a hard 30-day deadline worth protecting. A CP504 should prompt action, but the LT11 is the notice where missing the window has the steepest consequences.

What Is a Collection Due Process (CDP) Hearing?

A Collection Due Process hearing is an independent review of the proposed levy by the IRS Independent Office of Appeals, conducted under IRC Section 6330 before the IRS may collect by force. It is a separate, impartial look at the case by an office that was not involved in the original collection decision. At the hearing, a taxpayer can propose collection alternatives, raise certain defenses, and ask whether the levy is appropriate given the facts.

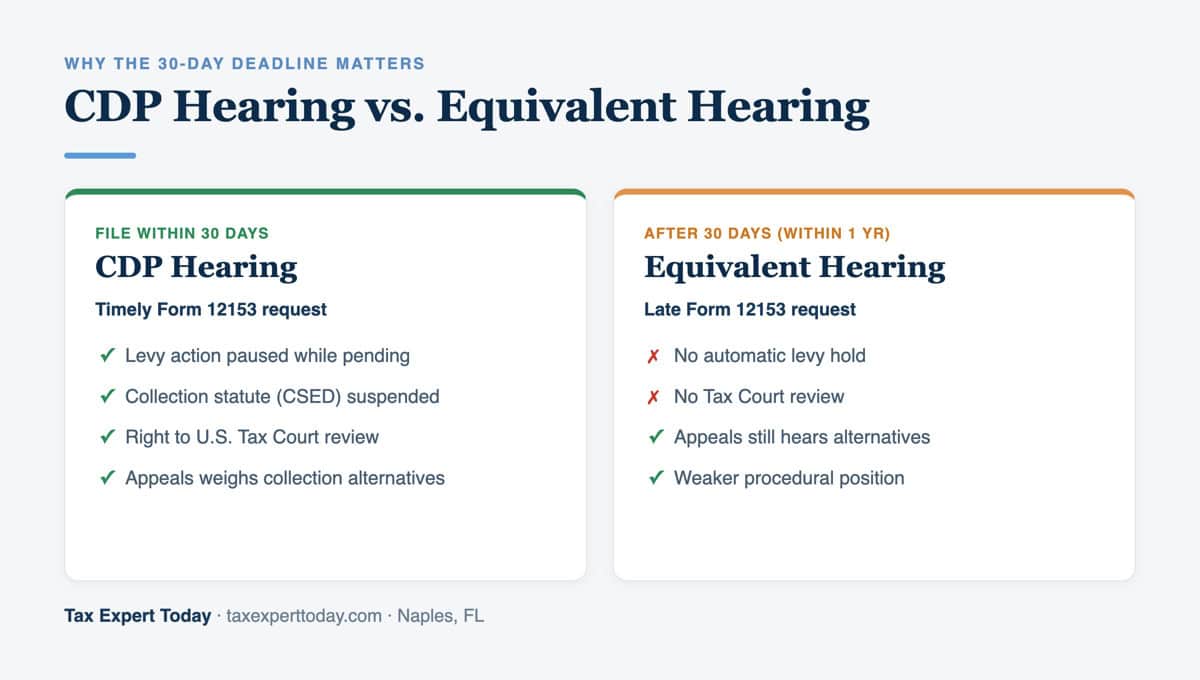

A timely CDP request has two protective effects under Section 6330: it generally suspends levy action while the hearing is pending, and it suspends the running of the collection statute of limitations under Section 6502 for that period. After Appeals issues its determination, the taxpayer has 30 days to petition the U.S. Tax Court for review — the judicial backstop that an equivalent hearing (discussed below) does not provide.

How Do I File Form 12153 and What Is the Deadline?

You request a CDP hearing by completing Form 12153, Request for a Collection Due Process or Equivalent Hearing, and sending it to the address shown on the LT11 / Letter 1058 within 30 days of the notice date. Meeting that deadline is what preserves the full set of rights, including Tax Court review. The core steps are below.

- Note the deadline. Count 30 days from the date on the notice, not the date you opened it. Calendar it immediately, because a late request drops you to an equivalent hearing with fewer rights.

- Complete Form 12153. Identify the tax periods listed on the notice and check the basis for the hearing — typically a collection alternative (installment agreement, offer in compromise, or currently not collectible), and any other issue you want Appeals to consider.

- State what you are proposing. Briefly describe the resolution you want the IRS to consider. You generally need to be in filing compliance (required returns filed) for Appeals to consider an alternative.

- Send it to the address on the notice and keep proof. Use a method that documents the mailing date, and keep a copy of the completed form and the notice.

While the request is pending, penalties and interest continue to accrue on the unpaid balance even though levy action is paused. The hearing addresses how the balance will be collected; it does not stop the underlying charges from running, which is one reason a workable resolution is the goal rather than delay for its own sake.

What Happens If I Miss the 30-Day CDP Deadline?

If you miss the 30-day window, you can still request an Equivalent Hearing using the same Form 12153, generally within one year of the notice, but you give up two important protections. An equivalent hearing does not carry the right to petition the U.S. Tax Court if you disagree with the result, and it does not automatically suspend levy action or the collection statute the way a timely CDP request does. Appeals will still consider collection alternatives, but from a weaker procedural position.

The practical lesson is that the 30-day deadline on an LT11 / Letter 1058 is the single most valuable date in the collection process, and protecting it is almost always worth doing even if the resolution itself is still being worked out. Filing a timely Form 12153 to preserve the CDP right buys time and keeps the Tax Court option open while the financial details are assembled.

What Collection Alternatives Can I Raise at a CDP Hearing?

At a CDP hearing you can ask Appeals to consider collection alternatives to a levy, raise certain defenses, and in limited cases challenge the underlying tax. The most common items raised are below.

- Installment agreement

- A monthly payment plan under IRC Section 6159 that resolves the balance over time and is an alternative to enforced collection.

- Offer in compromise

- A settlement for less than the full balance under IRC Section 7122 where the facts support it — see our offer in compromise guide for who qualifies.

- Currently not collectible status

- A pause on active collection where paying anything would prevent meeting basic living expenses. Interest and penalties continue to accrue.

- Challenge to the liability (limited)

- You may dispute the underlying tax at a CDP hearing only if you did not receive a notice of deficiency or otherwise have a prior opportunity to contest it.

- Spousal defenses and procedural issues

- Innocent spouse relief and arguments that the IRS did not follow required procedures can also be raised for Appeals to weigh.

For relief from the penalties on the balance — as distinct from arranging how to pay it — the standard waivers are covered in our guide on how to get IRS penalties removed. The CDP hearing is about the collection action; penalty abatement is a separate request that can run alongside it.

IRS Letter 1058 / LT11 Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to LT11 and Letter 1058 final notices — preserving the 30-day CDP deadline, preparing Form 12153, and presenting collection alternatives to the IRS Independent Office of Appeals. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 9am to 5pm ET.

Frequently Asked Questions

What is the difference between an LT11 and Letter 1058?

There is no substantive legal difference. Both the LT11 and Letter 1058 are the IRS Final Notice of Intent to Levy and Notice of Your Right to a Hearing under IRC Section 6330. The LT11 is generally issued by the IRS Automated Collection System, while Letter 1058 is generally issued by a Revenue Officer. Both start the same 30-day clock to request a Collection Due Process hearing and both authorize a levy on wages and bank accounts if no action is taken.

How long do I have to respond to an LT11 or Letter 1058?

You have 30 days from the date on the notice to request a Collection Due Process hearing by filing Form 12153. Filing within that window suspends levy action while the hearing is pending and preserves your right to petition the U.S. Tax Court if you disagree with the result. The 30 days run from the notice date, not the date you received or opened it, so the deadline should be calendared immediately.

What happens at a Collection Due Process hearing?

A CDP hearing is an independent review of the proposed levy by the IRS Independent Office of Appeals. At the hearing you can propose collection alternatives such as an installment agreement, offer in compromise, or currently not collectible status, raise spousal defenses or procedural issues, and in limited cases challenge the underlying tax if you had no prior opportunity to do so. Appeals then issues a determination, which you may petition to the U.S. Tax Court within 30 days.

What if I miss the 30-day CDP deadline?

If you miss the 30-day deadline, you can request an Equivalent Hearing using Form 12153, generally within one year of the notice. An equivalent hearing lets Appeals consider collection alternatives, but it does not carry the right to Tax Court review and does not automatically suspend levy action or the collection statute. Because of those lost protections, requesting a timely CDP hearing within the original 30 days is strongly preferable.

Where can I get help with an LT11 or Letter 1058 in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with LT11 and Letter 1058 final notices, preserving the CDP deadline, preparing Form 12153, and presenting collection alternatives to IRS Appeals. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for an LT11 or Letter 1058

An LT11 or Letter 1058 is the notice where the cost of waiting is highest, because the 30-day CDP window closes whether or not the financial picture is ready. The judgment calls are whether to file Form 12153 to preserve the hearing right, which collection alternative fits the facts, whether the underlying liability can still be challenged, and how to present the case to Appeals. Letting the 30 days lapse forfeits the Tax Court backstop and clears the way for a levy, which is the outcome the hearing exists to prevent. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review an LT11 or Letter 1058 and the response options that fit your facts. The 30-day deadline runs from the notice date, so the review is worth starting right away. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 10, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005