By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: To stop an IRS wage garnishment, you generally need to resolve the underlying balance or show that the levy creates a hardship: pay in full, set up an installment agreement, request currently not collectible status, submit an offer in compromise, or request a Collection Due Process hearing if your appeal window is still open. A wage levy is authorized under IRC Section 6331, and the IRS must release it under IRC Section 6343 once one of those conditions is met. Only a portion of your pay is exempt under IRC Section 6334, so acting quickly matters.

Published: June 2026

A wage garnishment, which the IRS calls a wage levy, is one of the most disruptive collection actions because it reaches your paycheck before you ever see it. It arrives only after the IRS has sent its earlier notices and the final notice of intent to levy, so by the time an employer is withholding pay, the account has been in collection for some time. The good news is that a wage levy is also one of the most releasable collection actions once you engage. This 2026 guide explains how a wage levy works, how much of your pay the IRS can take under Publication 1494, and the fastest legitimate ways to stop an IRS wage garnishment.

Can the IRS Garnish My Wages?

Yes. The IRS can garnish wages through a levy under IRC Section 6331, and unlike most creditors it does not need a court judgment first. Before it can reach your paycheck, however, the IRS must have assessed the tax, sent a notice and demand for payment, and issued a final notice of intent to levy with the right to a Collection Due Process hearing — generally the LT11 or Letter 1058.

That sequence matters because it tells you where you are. A wage levy does not appear out of nowhere; it follows the earlier CP14 notice, the reminder notices, the CP504 notice, and the final notice. If you have received the final notice but no levy has started yet, the most important step is protecting your appeal rights — our guide on the IRS Letter 1058 / LT11 and the CDP hearing covers the 30-day window. If the levy has already started, the focus shifts to getting it released.

How Much of My Paycheck Can the IRS Take?

The IRS does not take a fixed percentage of your pay. Instead, a wage levy takes everything above an exempt amount that is set by your filing status and number of dependents under IRC Section 6334(d). The exempt amount is what you keep; everything else in that paycheck goes to the IRS. Your employer figures the exempt amount using the tables in Publication 1494, based on the statement of exemptions you return.

This is why a wage levy can be so severe: it is the reverse of an ordinary garnishment. Rather than taking a slice and leaving you the rest, it leaves you a small exempt slice and takes the rest. The table below illustrates how the pieces fit together.

| Element | How it works |

|---|---|

| Exempt amount (what you keep) | Set by filing status and dependents; figured from the Publication 1494 tables |

| Amount levied | Essentially all take-home pay above the exempt amount |

| Statement of dependents | If you do not return it, the exempt amount defaults to married filing separately with no dependents |

| Duration | A wage levy is continuous under §6331(e) — it keeps attaching to each paycheck until released or paid |

Two points are easy to miss. First, because the levy is continuous under IRC Section 6331(e), it does not stop after one paycheck; it keeps attaching to your wages until the balance is paid or the levy is released. Second, returning the statement of exemptions and dependents promptly is important — if you do not, the exempt amount is calculated as if you were married filing separately with no dependents, which shrinks what you keep.

How Do I Stop an IRS Wage Garnishment?

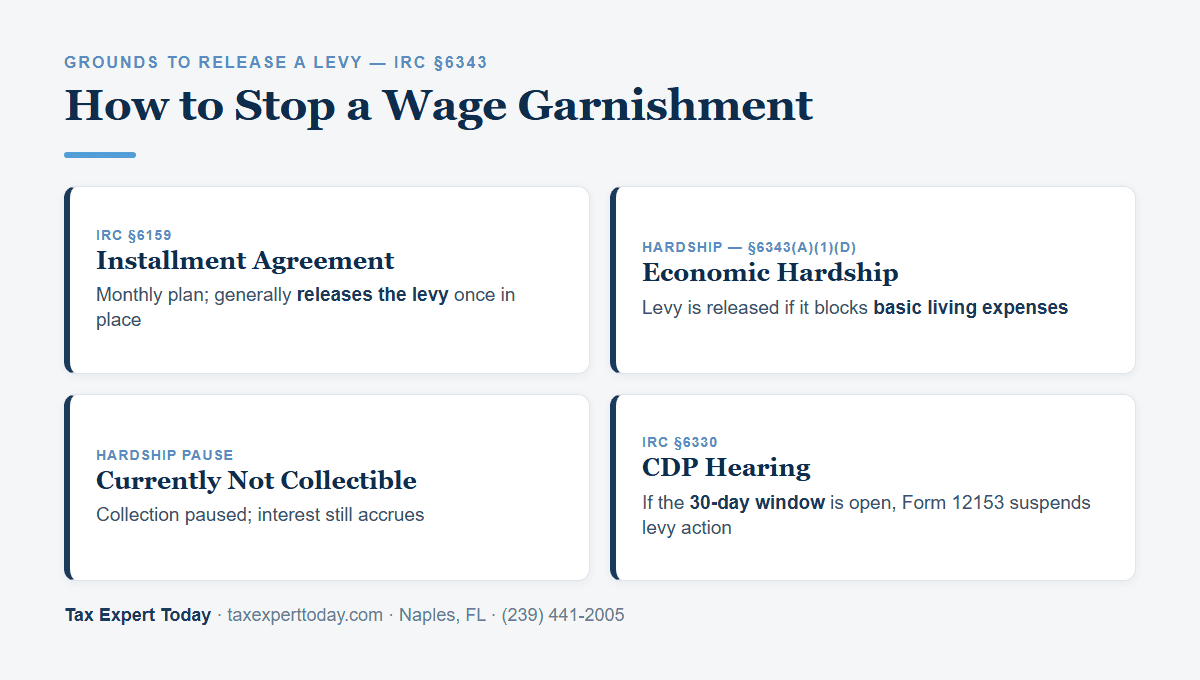

You stop an IRS wage garnishment by resolving the balance or qualifying for a release condition under IRC Section 6343. The fastest ways to stop IRS wage garnishment are usually to enter a payment arrangement or to show hardship, because both give the IRS a basis to release the levy. The main paths are below.

- Pay the balance in full

- Full payment ends the levy because there is no longer a balance to collect. Where that is not possible, the options below resolve it over time or pause it.

- Set up an installment agreement

- A monthly payment plan under IRC Section 6159 generally leads the IRS to release a wage levy once the agreement is in place. On a timely-filed return, an approved agreement also drops the failure-to-pay penalty rate from 0.5% to 0.25% per month — see our guide on the failure-to-pay penalty.

- Request currently not collectible status

- If paying anything would prevent you from meeting basic living expenses, the IRS may place the account in currently not collectible status and release the levy. Interest and penalties continue to accrue while collection is paused.

- Submit an offer in compromise

- A settlement for less than the full balance under IRC Section 7122 where income, expenses, and assets support it — our offer in compromise guide covers who qualifies.

- Request a Collection Due Process hearing

- If the 30-day window from the final notice of intent to levy is still open, filing Form 12153 generally suspends levy action while Appeals considers collection alternatives — see the LT11 / CDP guide.

- Show the levy is improper

- If the tax is not actually owed, the collection period has expired, or the IRS did not follow required procedures, that can be a basis to release the levy. Keep proof of payments and notices.

Whichever path fits, the levy keeps running until the IRS acts, so the priority is opening a resolution quickly and getting the release in writing. Penalties and interest also keep accruing on the unpaid balance throughout — you can estimate that cost with our IRS penalty and interest calculator.

How Fast Can a Wage Levy Be Released?

A wage levy can often be released quickly once the IRS has what it needs, but the timing depends on the path. The IRS is required to release a levy under IRC Section 6343(a) when the liability is satisfied, the collection period expires, a release will facilitate collection, an installment agreement provides otherwise, or the levy is creating an economic hardship.

In practice, the speed comes down to how quickly you can document your situation. When the basis is an installment agreement or hardship, the IRS generally needs current financial information, which is why having pay stubs, expense records, and the relevant financial statement (such as Form 433-F or Form 433-A) ready shortens the timeline. Once the IRS agrees to release the levy, it sends the release to your employer, and your next available paycheck should reflect it. Because the levy is continuous, every pay period that passes before the release is another period of withheld wages — so the practical message is to act before the next payroll cutoff.

Can a Wage Garnishment Be Reversed for Hardship?

Yes. Economic hardship is one of the statutory grounds for releasing a levy under IRC Section 6343(a)(1)(D). If the levy prevents you from meeting reasonable basic living expenses, the IRS is required to release it — releasing the levy does not erase the underlying balance, but it stops the withholding while you arrange a longer-term resolution.

Hardship is evaluated on your facts: income, necessary living expenses, and the effect the levy has on your ability to cover them. Establishing it usually means submitting a collection information statement and supporting documentation. In many cases the hardship release goes hand in hand with placing the account in currently not collectible status or entering an affordable installment agreement, so the levy comes off and the account moves onto a sustainable footing at the same time.

Stop an IRS Wage Garnishment: Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to IRS wage levies — confirming the balance, preparing the financial information the IRS requires, and arranging the installment agreement, hardship release, or other alternative that gets the levy released and the account resolved. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 9am to 5pm ET.

Frequently Asked Questions

How do I stop an IRS wage garnishment fast?

The fastest legitimate ways to stop an IRS wage garnishment are to pay the balance in full, enter an installment agreement under IRC Section 6159, or show economic hardship so the IRS releases the levy under IRC Section 6343. Because a wage levy is continuous and attaches to each paycheck, opening one of these resolutions before your next payroll cutoff is what limits how much pay is withheld in the meantime.

How much of my paycheck can the IRS take in a wage levy?

The IRS leaves you an exempt amount based on your filing status and number of dependents under IRC Section 6334, and levies essentially everything above it. Your employer figures the exempt amount from the tables in Publication 1494. If you do not return the statement of dependents, the exempt amount is calculated as married filing separately with no dependents, which leaves you with less.

Does the IRS need a court order to garnish my wages?

No. Unlike most private creditors, the IRS can levy wages under IRC Section 6331 without a court judgment. It must first assess the tax, send a notice and demand for payment, and issue a final notice of intent to levy with Collection Due Process rights at least 30 days before levying. Once those steps are complete, it can issue the wage levy directly to your employer.

Will an installment agreement stop a wage garnishment?

In most cases, yes. Once an installment agreement under IRC Section 6159 is in place, the IRS generally releases an active wage levy because the balance is being addressed through the agreed payments. On a timely-filed return, an approved agreement also reduces the failure-to-pay penalty rate from 0.5% to 0.25% per month, lowering the cost of resolving the balance.

Where can I get help with an IRS wage garnishment in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with IRS wage levies, preparing the required financial information and arranging the installment agreement, hardship release, or other alternative that gets the levy released. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a Wage Levy

A wage levy is time-sensitive in a way most collection actions are not, because every pay period that passes is wages already withheld. The judgment calls are choosing the release path that fits your finances, assembling the financial information the IRS will require, and getting the release confirmed to your employer before the next payroll run. Those are the steps where experience saves pay periods. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review a wage levy, confirm the balance, and choose the release that fits your facts. Because the levy keeps attaching to each paycheck until it is released, the review is worth starting right away. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 18, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005