By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: An IRS CP14 notice is the first letter the IRS sends when it has assessed tax you owe and not yet received payment. It is the formal “notice and demand for payment” required by IRC Section 6303, and it shows the tax, the failure-to-pay penalty, and interest that have accrued. The notice asks for full payment, usually within 21 days. It is not a levy or a threat to seize property — it is the start of the IRS collection sequence, and you have several ways to respond even if you cannot pay the full balance.

Published: June 8, 2026

A CP14 is the most common notice the IRS sends, and for most people it is the first written confirmation that a balance is owed. It tends to arrive a few weeks after a return is filed with tax due, or after the IRS adjusts a return. The notice can be unsettling, but it is an early, routine step — not a final demand and not an enforcement action. This 2026 guide explains what the CP14 means under Internal Revenue Code Section 6303, how the 21-day window works, how penalties and interest keep building, where the notice sits in the larger collection sequence, and the response options that fit whether you can pay, can pay over time, or believe the bill is wrong.

What Is an IRS CP14 Notice?

An IRS CP14 notice is a balance-due bill telling you the IRS has assessed tax that has not been paid, and it is the agency’s formal notice and demand for payment under IRC Section 6303. The notice lists the tax year involved, the original tax owed, the failure-to-pay penalty accrued under IRC Section 6651(a)(2), the interest accrued under IRC Section 6601, and a total amount due by a stated date. Section 6303 requires the IRS to send this notice within 60 days of assessing the tax, which is why a CP14 often follows so soon after a return is processed.

The CP14 is an information-and-demand notice, not a collection-enforcement notice. It does not authorize a levy, it does not place a lien, and it does not start the clock on any enforced collection by itself. What it does is establish, in writing, that the IRS has demanded payment — a procedural step the IRS must take before the rest of the collection process can move forward. Treating it as a routine first bill, rather than ignoring it or panicking over it, is the correct posture.

Why Did I Get a CP14 Notice?

You received a CP14 because the IRS records show tax assessed for a year and a remaining balance that has not been paid in full. The most common reasons are a return filed showing a balance due that was not paid with the return, a return where the payment was short of the total, estimated taxes that came in under what the return required, or an IRS adjustment that increased the tax after processing. In each case the system generates a CP14 to demand the unpaid amount.

Because the failure-to-pay penalty and interest are calculated from the original due date of the return, the total on a CP14 is usually larger than the bare tax figure a taxpayer remembers. That is expected. The penalty under Section 6651(a)(2) runs at 0.5% of the unpaid tax for each month or part of a month it remains unpaid, and interest under Section 6601 compounds daily. The gap between “what I owed” and “what the notice says” is almost always those two accruals, not an error — though it is always worth confirming the figures, which the section below on a wrong notice covers.

How Long Do I Have to Respond to a CP14?

A CP14 generally gives you 21 calendar days from the notice date to pay the balance in full before additional failure-to-pay penalty is charged on the notice amount, and that window shortens to 10 business days when the balance shown is $100,000 or more. The shorter period for larger balances comes from IRC Section 6601(e)(3). Paying within the stated window is the cleanest resolution and stops further accrual on the amount paid.

One point that surprises people: the 21-day window is the deadline to avoid additional charges on the notice balance, but penalties and interest from the original due date do not pause while you decide what to do. The table below shows how the accruals on a CP14 balance work.

| Charge | Authority | How it accrues |

|---|---|---|

| Failure-to-pay penalty | IRC 6651(a)(2) | 0.5% of unpaid tax per month or part-month, up to a 25% cap |

| Interest on the underpayment | IRC 6601 | Federal short-term rate plus 3%, compounded daily, until paid |

| Standard payment deadline | CP14 notice / IRC 6303 | 21 calendar days from the notice date |

| Deadline if balance is $100,000 or more | IRC 6601(e)(3) | 10 business days from the notice date |

Because the charges keep running, waiting rarely helps. As a rough illustration of the mechanism: on a $20,000 unpaid balance, the failure-to-pay penalty alone adds about $100 each month it stays unpaid, separate from daily interest — and that continues until the balance is paid or the penalty reaches its 25% cap. You can estimate the running total for your own figures with our IRS penalty and interest calculator.

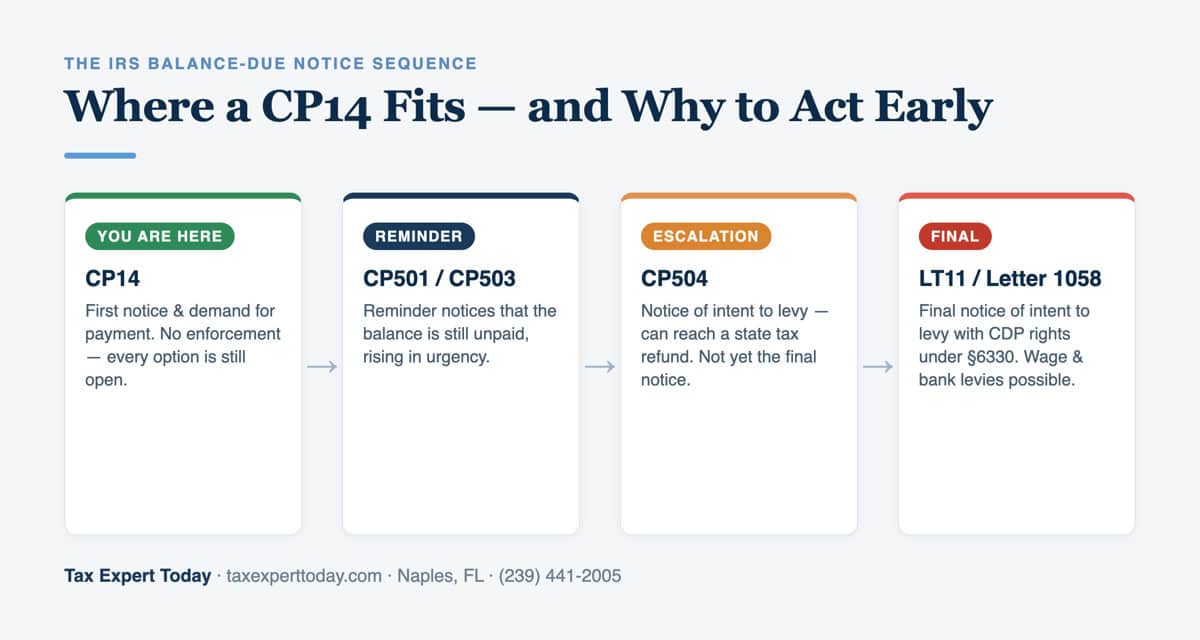

Where Does a CP14 Fit in the IRS Notice Sequence?

The CP14 is the top of the IRS collection-notice funnel; if a balance stays unpaid and unaddressed, the IRS follows it with a predictable series of escalating notices. Knowing the order tells you how much time and how many decision points remain. The CP14 itself is the lowest-pressure stage, which is exactly why it is the best moment to act.

- CP14 — the first notice and demand for payment. No enforcement; the balance is simply due.

- CP501 / CP503 — reminder notices that the balance remains unpaid, with increasing urgency in tone.

- CP504 — a notice of intent to levy that can reach a state tax refund. It is a serious escalation but is still not the final pre-levy notice.

- LT11 / Letter 1058 — the final notice of intent to levy, which carries the right to a Collection Due Process hearing under IRC Section 6330. This is the stage where wage and bank levies become possible.

The practical takeaway is that responding at the CP14 stage keeps every option open and the cost low. Each later notice narrows choices and raises the stakes, and the levy notices carry strict deadlines for preserving appeal rights. Addressing a CP14 now is far simpler than untangling a levy later.

What If I Can’t Pay the CP14 Balance?

If you cannot pay a CP14 balance in full, the IRS offers several structured alternatives, and applying for one is far better than letting the notice sequence escalate. The right option depends on how much you owe and your ability to pay over time. The main paths are below.

- Short-term payment (up to 180 days)

- If you can clear the balance within about six months, a short-term payment plan avoids a setup fee. Penalty and interest continue to accrue until the balance is gone, but no formal agreement is required.

- Installment agreement (monthly payment plan)

- A monthly payment plan under IRC Section 6159 lets you pay over time. Many taxpayers who owe under the IRS threshold can set one up online. Once an agreement is in place on a timely-filed return, the failure-to-pay penalty rate drops from 0.5% to 0.25% per month.

- Offer in compromise

- An offer in compromise under IRC Section 7122 can settle a liability for less than the full amount when paying in full is not feasible based on income, expenses, and assets. It is fact-dependent and not available to everyone — our offer in compromise guide explains who qualifies.

- Currently not collectible status

- If paying anything would prevent you from meeting basic living expenses, the IRS can place the account in currently not collectible status, pausing active collection. Interest and penalties continue to accrue while the account is paused.

Whatever the path, the failure-to-pay penalty and interest discussed above keep running until the balance is satisfied, so the value of acting early is real. For relief from the penalties themselves — as opposed to a way to pay the tax — see our guide on how to get IRS penalties removed, which covers First-Time Abatement and reasonable cause for the failure-to-pay penalty under IRC Section 6651.

What If the CP14 Notice Is Wrong?

If you believe a CP14 is incorrect, do not pay it on autopilot and do not ignore it — contact the IRS to dispute the balance before the payment deadline. A CP14 can be wrong when a payment you made was not credited, was applied to a different year, or crossed in the mail with the notice; when an estimated payment is missing; or when an IRS adjustment misread an entry on the return. The notice includes a contact number and a response deadline, and the IRS can place a short hold while it researches a disputed item.

When you dispute a CP14, do it in writing where possible and keep proof: copies of cancelled checks or electronic payment confirmations, the return as filed, and any prior IRS correspondence. If the balance is correct but the penalty is the problem, that is a separate request — abatement of the failure-to-pay penalty under First-Time Abatement or reasonable cause — rather than a dispute of the tax. Mixing the two slows things down, so it helps to identify which one actually applies before you call. Where the figures are right and the tax is genuinely owed, the productive move is to stop the accruals by paying or arranging one of the alternatives above.

IRS CP14 Notice Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to CP14 notices and the balance-due notices that follow — confirming whether the amount is correct, arranging installment agreements or other collection alternatives, and requesting penalty relief where the facts support it. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 9am to 5pm ET.

Frequently Asked Questions

What does an IRS CP14 notice mean?

A CP14 notice means the IRS has assessed tax for a year and shows an unpaid balance. It is the formal notice and demand for payment required by IRC Section 6303 and lists the tax, the failure-to-pay penalty, the interest, and a total due by a stated date. It is the first notice in the IRS collection sequence and is not a levy or an enforcement action. It does mean a balance is owed and that penalties and interest are accruing until it is paid.

How long do I have to pay a CP14 notice?

A CP14 generally gives 21 calendar days from the notice date to pay the balance in full before additional failure-to-pay penalty is charged on the notice amount. If the balance shown is $100,000 or more, the window is 10 business days under IRC Section 6601(e)(3). Penalties and interest that accrued from the original due date of the return do not pause during this window, so paying or arranging an alternative promptly limits the cost.

What happens if I ignore a CP14 notice?

If you ignore a CP14, the balance stays unpaid and the IRS sends a series of escalating notices — reminder notices, then a CP504 notice of intent to levy, then an LT11 or Letter 1058 final notice that carries Collection Due Process rights and allows wage and bank levies. The failure-to-pay penalty and interest continue to accrue the entire time. Responding at the CP14 stage keeps every option open and costs far less than addressing a levy later.

Can I set up a payment plan after a CP14?

Yes. A CP14 is a normal entry point for an IRS payment plan. A short-term plan of up to about 180 days avoids a setup fee, and a longer monthly installment agreement under IRC Section 6159 lets you pay over time, with many taxpayers eligible to apply online. Once an installment agreement is in place on a timely-filed return, the failure-to-pay penalty rate is reduced from 0.5% to 0.25% per month, though interest continues to accrue.

Where can I get help with a CP14 notice in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with CP14 notices, confirming the balance, arranging installment agreements or other collection alternatives, and requesting penalty relief where the facts support it. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a CP14 Notice

A CP14 is manageable, and many taxpayers who can pay simply pay it. Professional help earns its keep when the balance is one you cannot pay in full, when the figures look wrong, when several years are involved, or when you want to weigh an installment agreement against an offer in compromise on the actual numbers. The judgment calls are confirming the assessment is correct, choosing the collection alternative that fits your finances, and timing a penalty-relief request so it does not get tangled with a balance dispute. Acting at the CP14 stage, before the notice sequence escalates toward a levy, is what keeps the options wide and the cost contained. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review a CP14 notice, confirm the balance, and choose the response that fits your facts. The payment window is short and the accruals are daily, so the review is worth starting right away. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 8, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005