By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: An IRS CP504 notice is a notice of intent to levy, issued under IRC Section 6331(d), that warns the IRS intends to seize your state income tax refund and apply it to an unpaid balance. Despite its urgent tone, the CP504 is not the final notice before the IRS can levy wages and bank accounts — that requires a later notice (the LT11 or Letter 1058) carrying Collection Due Process rights. The CP504 is a serious escalation that should be resolved promptly, but you still have several ways to respond.

Published: June 2026

The CP504 sits in the middle of the IRS collection sequence — after the first CP14 notice and the reminder notices, but before the final notice of intent to levy. It is the notice where the language turns from a bill into a warning, and it is often the point at which taxpayers first take a balance seriously. This 2026 guide explains what the CP504 actually authorizes under Internal Revenue Code Section 6331, why it is not the final pre-levy notice, what the IRS can and cannot reach at this stage, and how to respond before the case escalates.

What Is an IRS CP504 Notice?

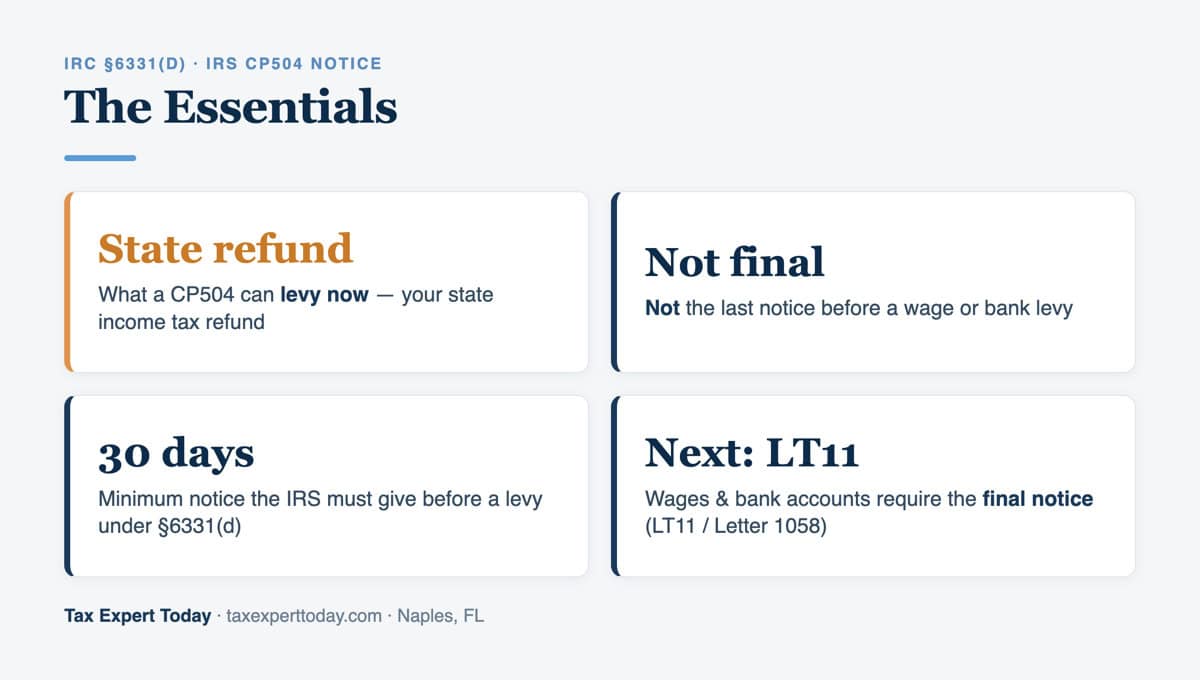

An IRS CP504 notice is a notice of intent to levy that the IRS sends when a balance has gone unpaid through the earlier notices, warning that the IRS intends to seize the taxpayer’s state income tax refund and apply it to the debt. It is issued under the §6331(d) requirement that the IRS give notice at least 30 days before a levy. The notice states the amount due, the tax period, and the IRS’s intent to levy, and it generally indicates the IRS may also file a Notice of Federal Tax Lien.

The CP504 follows the CP14 and the CP501 and CP503 reminder notices in the standard sequence. Its arrival means the account has moved into a more serious collection posture, and that automated enforcement is approaching. The notice is real and should not be ignored — but as the next section explains, what it can actually reach right away is narrower than its tone suggests.

Is a CP504 the Final Notice of Intent to Levy?

No. A CP504 is a notice of intent to levy, but it is not the final notice the IRS must send before levying wages, bank accounts, and most other property. That final step is a separate notice — the LT11 or Letter 1058 — which carries the right to a Collection Due Process hearing under IRC Section 6330. Because the CP504 does not include that hearing notice, it does not by itself authorize a levy on wages or bank accounts.

This distinction matters for two reasons. First, it tells you roughly how much time and how many steps remain before enforced collection against your paycheck or accounts. Second, it tells you the CP504 is the better, lower-pressure moment to resolve the balance — before the final notice starts the 30-day Collection Due Process clock. Treating the CP504 as the last word, or conversely dismissing it because it is not the final notice, are both mistakes.

What Can the IRS Levy After a CP504?

After a CP504, the IRS can levy the taxpayer’s state income tax refund, but it must still issue the final notice of intent to levy before reaching wages, bank accounts, or other property. The table below separates what the CP504 stage allows from what requires the later notice.

| Action | Allowed after a CP504? | What is required |

|---|---|---|

| Levy a state income tax refund | Yes | The CP504 itself |

| File a Notice of Federal Tax Lien | Possible | Separate lien procedures |

| Levy wages or a bank account | Not yet | Final notice (LT11 / Letter 1058) + 30-day CDP window |

| Seize other property | Not yet | Final notice (LT11 / Letter 1058) + 30-day CDP window |

In other words, the most disruptive levies — a wage garnishment or a frozen bank account — cannot happen on the strength of a CP504 alone. They follow the final notice. That is precisely why resolving the balance at the CP504 stage is valuable: it keeps the case from reaching the notice that opens the door to those actions.

How Do I Respond to a CP504 Notice?

You respond to a CP504 by paying the balance, arranging a collection alternative, or disputing the amount before the IRS escalates to the final notice. The available paths are the same structured options the IRS offers throughout collection, and choosing one promptly is what stops the sequence from advancing.

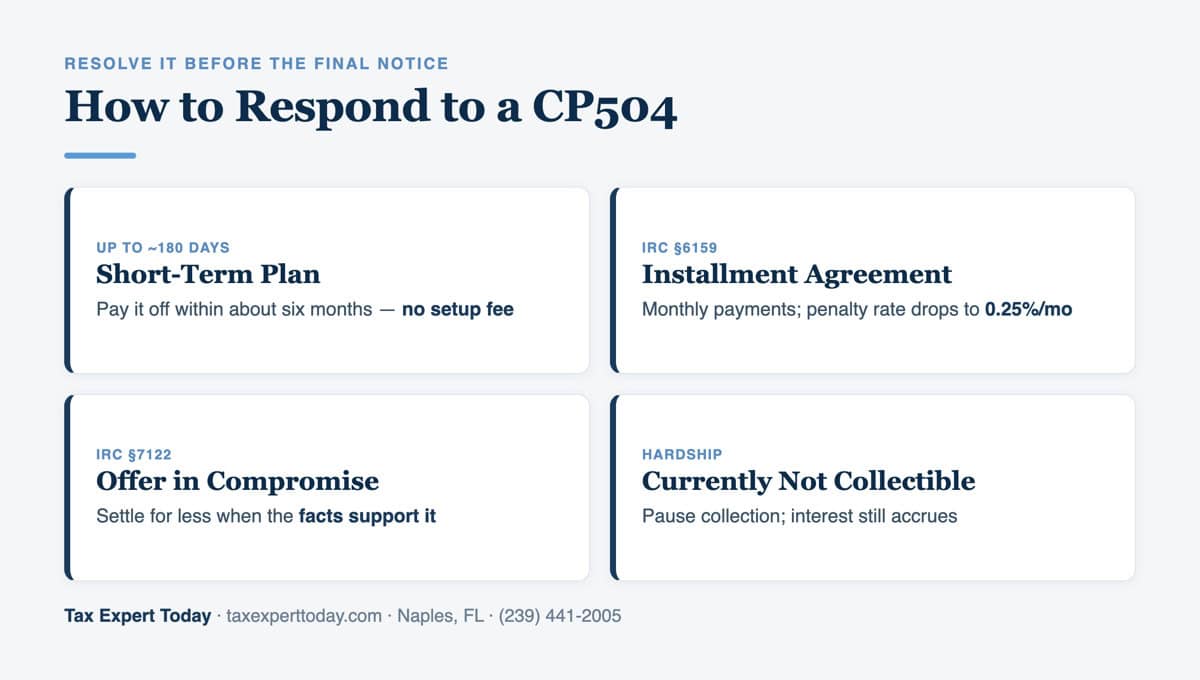

- Pay or arrange a short-term plan

- Paying in full stops further accrual. If you can clear the balance within about 180 days, a short-term payment plan avoids a setup fee.

- Installment agreement

- A monthly payment plan under IRC Section 6159 resolves the balance over time. Once an agreement is in place on a timely-filed return, the failure-to-pay penalty rate drops from 0.5% to 0.25% per month.

- Offer in compromise

- A settlement for less than the full balance under IRC Section 7122 where income, expenses, and assets support it — our offer in compromise guide covers who qualifies.

- Currently not collectible status

- A pause on active collection where paying anything would prevent meeting basic living expenses. Interest and penalties continue to accrue.

- Dispute the balance

- If the amount looks wrong — a missing payment or an IRS adjustment error — contact the IRS using the number on the notice before the deadline and keep proof of payments.

Penalties and interest continue to run on the unpaid balance throughout, so acting at the CP504 stage limits the cost as well as the risk. For relief from the penalties themselves, see our guide on how to get IRS penalties removed.

CP504 vs LT11 / Letter 1058: What Is the Difference?

The CP504 is an intermediate notice of intent to levy that can reach a state tax refund, while the LT11 / Letter 1058 is the final notice that authorizes a levy on wages and bank accounts and carries Collection Due Process rights. Confusing the two is the most common and most costly mistake at this stage, because the deadlines and the available defenses are different.

If you have received the final notice rather than a CP504, the 30-day window to request a Collection Due Process hearing is running, and protecting it is urgent — our guide on the IRS Letter 1058 / LT11 and CDP hearing walks through Form 12153 and that deadline. If you have a CP504, you are a step earlier, with more options and less time pressure — which makes it the better moment to resolve the balance.

IRS CP504 Notice Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to CP504 notices and the rest of the IRS collection sequence — confirming the balance, arranging installment agreements or other alternatives, and resolving the account before it reaches the final notice of intent to levy. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 9am to 5pm ET.

Frequently Asked Questions

What does an IRS CP504 notice mean?

A CP504 notice means a balance has gone unpaid through the earlier IRS notices and the IRS intends to levy your state income tax refund to collect it. It is issued under IRC Section 6331(d) as a notice of intent to levy and may also indicate the IRS could file a Notice of Federal Tax Lien. It is a serious escalation, but it is not the final notice required before the IRS can levy wages or bank accounts.

Can the IRS take my paycheck or bank account after a CP504?

Not on the strength of a CP504 alone. A CP504 allows the IRS to levy a state income tax refund, but to levy wages, a bank account, or other property the IRS must first send the final notice of intent to levy (the LT11 or Letter 1058), which carries a 30-day Collection Due Process hearing right under IRC Section 6330. The CP504 is the stage before that final notice.

How do I stop a CP504 levy?

Resolve the balance before the IRS escalates: pay in full, set up an installment agreement under IRC Section 6159, apply for an offer in compromise under IRC Section 7122 if the facts support it, request currently not collectible status if paying would prevent meeting basic expenses, or dispute the amount if it is wrong. Acting at the CP504 stage keeps the case from reaching the final notice and the levies that follow it.

How long do I have to respond to a CP504?

A CP504 generally gives you until the date stated on the notice, and the IRS must allow at least 30 days before levying. Because penalties and interest keep accruing and the next step is the final notice of intent to levy, responding promptly is important even though the most disruptive levies cannot occur until that later notice is sent.

Where can I get help with a CP504 notice in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with CP504 notices, confirming the balance, arranging installment agreements or other collection alternatives, and resolving the account before it reaches the final notice of intent to levy. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a CP504 Notice

A CP504 is a warning with room to act, and that room is the opportunity. The judgment calls are confirming the balance is correct, choosing the collection alternative that fits your finances, and resolving the account before the final notice of intent to levy starts the Collection Due Process clock. Waiting until that final notice arrives narrows the options and raises the stakes, so the CP504 stage is the efficient time to engage. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review a CP504 notice, confirm the balance, and choose the response that fits your facts. Resolving it now keeps the case out of the final-notice stage, so the review is worth starting right away. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 15, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005