By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

This IRS underpayment penalty calculator estimates the Form 2210 penalty you may owe for paying your 2026 estimated taxes too slowly. If you earn income that is not subject to withholding, self-employment income, business profits, investment gains, or distributions, the IRS expects you to pay tax on it throughout the year through estimated payments. Pay too little, too late, and you owe an underpayment of estimated tax penalty under Internal Revenue Code §6654, reported on IRS Form 2210. Use the underpayment penalty calculator below to estimate what you may owe, then read on for how the penalty works and how to avoid it.

Quick Answer: The IRS underpayment penalty applies when you do not pay at least 90% of your current year tax or 100% of your prior year tax (110% if your prior year AGI exceeded $150,000), whichever is smaller, through withholding and timely estimated payments. The penalty is interest, charged quarter by quarter at the federal short-term rate plus three percentage points under IRC §6621, 6% for the quarter beginning April 1, 2026.

Published: June 2, 2026

Primary sources

Estimate your 2026 federal estimated tax underpayment penalty, results update as you type

Estimate only. This tool uses the Form 2210 regular method and assumes any quarterly shortfall stays unpaid through the April 15, 2027 filing deadline, withholding is spread evenly across the four periods, and a single interest rate applies. It does not apply the annualized income installment method, special farmer/fisherman rules, or rate changes between quarters. Your actual penalty is determined by the IRS. Confirm the current rate on the IRS quarterly interest rates page and see the disclaimer below.

How to use this underpayment penalty calculator

Enter your projected 2026 total tax, your 2026 withholding, any quarterly estimated payments, and your 2025 tax. The underpayment penalty calculator applies the Form 2210 safe harbors and the current 6% interest rate, then estimates your penalty as you type. It is a planning estimate; the sections below explain how the figure is built.

What is the IRS underpayment of estimated tax penalty?

The underpayment penalty is not a flat fine, it is interest the IRS charges when you pay your income tax too slowly during the year. Under IRC §6654, the U.S. tax system is “pay as you go”: you must pay tax as you earn income, either through payroll withholding or quarterly estimated payments. When your timely payments fall short of the required amount, the IRS applies an interest charge to the shortfall for each period it remained unpaid.

The rate is set quarterly under IRC §6621 as the federal short-term rate plus three percentage points. For the quarter beginning April 1, 2026 the individual underpayment rate is 6% (down from 7% in the first quarter of 2026). Because the penalty is computed period by period, two taxpayers who owe the same total at year end can face very different penalties depending on when they fell behind.

How the One Big Beautiful Bill Act (OBBBA) affects 2026 estimated taxes

The One Big Beautiful Bill Act did not change the §6654 safe harbors, the 90% / 100% / 110% tests and the $150,000 AGI threshold still apply for 2026.

What it did change is the math behind your total tax: OBBBA made the current tax brackets permanent and, for 2026, raised the standard deduction (to $16,100 for single filers and $32,200 for married couples filing jointly), added a $6,000 deduction for taxpayers 65 and older, lifted the SALT cap to $40,000, and created new deductions for qualified tips and overtime. These provisions can lower your tax, but they can also reduce paycheck withholding, which quietly raises your underpayment risk if your estimated payments do not keep pace. If your 2026 income or withholding shifted, re-check your safe harbor with the calculator above.

Who has to pay estimated taxes (and who owes the penalty)?

You generally must make estimated payments, and risk the penalty if you do not, when you expect to owe at least $1,000 in tax after subtracting withholding and refundable credits. This most often affects self-employed individuals, business owners and partners, S-corporation shareholders, retirees taking distributions, investors with capital gains or dividends, landlords, and gig workers. Per the IRS estimated taxes guidance, W-2 employees can often avoid the issue by increasing payroll withholding instead.

There is an important exception: if you had no tax liability for the prior year, you were a U.S. citizen or resident for the whole year, and that year covered 12 months, you generally owe no underpayment penalty this year regardless of what you owe now.

How is the underpayment penalty calculated?

The penalty is calculated on Form 2210 in four steps. First, the IRS determines your required annual payment, the smaller of 90% of your current year tax or 100% of your prior year tax (110% if your prior year AGI was over $150,000). Second, that amount is divided into four required installments due April 15, June 15, September 15, and January 15.

Third, your withholding and estimated payments are credited against each installment, with overpayments carried forward. Fourth, any shortfall in a period is charged interest at the §6621 rate from that installment’s due date until the date paid (or the April 15 filing deadline).

Withholding gets favorable treatment: it is treated as paid in equal amounts on each due date, no matter when it was actually withheld. That is why bumping up your year end withholding can retroactively cover earlier quarters, an option estimated payments do not offer. The calculator above applies this same regular method logic.

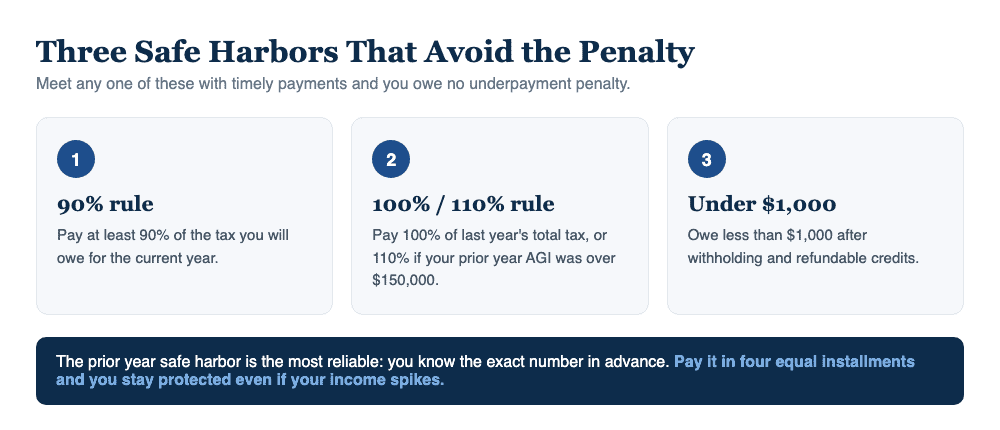

What are the safe harbors that protect you from the penalty?

You avoid the penalty entirely if your timely payments meet any one of these safe harbors: you pay at least 90% of your current year tax; or you pay 100% of last year’s tax (110% if your prior year AGI exceeded $150,000); or your total balance due after withholding is under $1,000. The prior year safe harbor is the most reliable because you know the exact number in advance, pay it in four equal installments and you are protected even if your income spikes.

- 90% rule: pay 90% of what you will owe this year.

- 100% / 110% rule: pay 100% of last year’s total tax (110% if 2025 AGI > $150,000).

- $1,000 rule: owe less than $1,000 after withholding and credits.

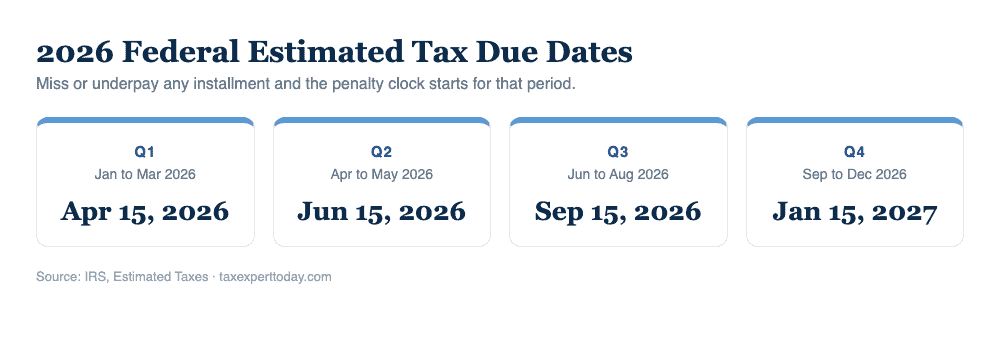

2026 estimated tax due dates

Federal estimated tax payments for the 2026 tax year are due in four installments. Missing or underpaying any one of them can start the penalty clock for that period, even if you catch up later.

- Q1 (Jan to Mar 2026): due April 15, 2026

- Q2 (Apr to May 2026): due June 15, 2026

- Q3 (Jun to Aug 2026): due September 15, 2026

- Q4 (Sep to Dec 2026): due January 15, 2027

How do I avoid the underpayment penalty?

The cleanest way to avoid the penalty is to lock in the prior year safe harbor: divide last year’s total tax (times 110% if your AGI was over $150,000) by four and pay that amount each quarter on time. If your income is uneven, a big Q4 capital gain, for example, the annualized income installment method on Form 2210 Schedule AI can reduce the penalty by matching required payments to when you actually earned the income. W-2 earners with side income can often skip estimates entirely by raising withholding on a paycheck or a retirement distribution. To turn your safe harbor number into four dated payment amounts, run it through our quarterly estimated tax calculator.

Can the underpayment penalty be waived?

Yes, in specific situations. Under IRC §6654(e), the IRS can waive the penalty if the underpayment was caused by a casualty, disaster, or other unusual circumstance where charging it would be inequitable, or if you retired after age 62 or became disabled during the tax year and the underpayment was due to reasonable cause rather than willful neglect. You request the waiver in Part II of Form 2210 with a statement explaining the circumstances. Waivers are fact-specific, and a well-documented request matters.

Federal vs. state estimated tax penalties

This calculator covers the federal penalty. States with an income tax run their own parallel systems, California uses FTB Form 5805 and Georgia uses Form 500 UET, each with its own rate and rules. If you live or do business in California or Georgia, you may owe a state penalty in addition to the federal one. Florida and Texas have no personal income tax, so there is no state estimated tax penalty for individuals in those states. We help clients in California, Georgia, and nationwide manage both layers.

Note on a related but different penalty

The underpayment penalty discussed here is for paying estimated tax too slowly during the year. It is different from the failure-to-file and failure-to-pay penalties (plus interest) that apply when you file or pay your final balance late. If you’ve already filed and simply owe a balance with late penalties accruing, use our IRS penalty and interest calculator instead, which covers IRC §6651 and §6601.

Frequently asked questions

How much is the IRS underpayment penalty?

There is no flat amount. The penalty is interest charged on each period’s shortfall at the federal short-term rate plus three percentage points (set quarterly under IRC §6621; 6% for the quarter beginning April 1, 2026). Because it accrues by period, the size depends on how much you underpaid and how early in the year you fell behind.

What happens if I do not pay estimated taxes?

If you owe $1,000 or more after withholding and do not meet a safe harbor, the IRS adds an underpayment penalty to your tax bill, calculated on Form 2210. You still owe the underlying tax as well. Paying late on the final balance can also trigger separate failure-to-pay penalties and interest.

Is the underpayment penalty deductible?

For individuals, no. The IRC §6654 estimated tax penalty is a personal, nondeductible charge. Businesses should consult a tax professional, as treatment can differ by entity type and the nature of the underpayment.

Can I just pay the penalty with my return?

Often yes. If you do not compute Form 2210 yourself, the IRS will usually calculate the penalty and send a bill, or you can let your software figure it. However, computing it, and checking the annualized income method or a waiver, can reduce or eliminate the amount, so it is worth reviewing before you assume the default figure is final.

Does increasing withholding really help after the fact?

Yes. Unlike estimated payments, federal withholding is treated as paid evenly across all four periods regardless of when it was actually withheld. Increasing withholding late in the year, through a paycheck or a retirement account distribution, can retroactively cover earlier quarters and shrink or erase the penalty.

Where can I get help with estimated tax penalties in Naples, FL?

Tax Expert Today LLC is based at 11983 Tamiami Trail N, Naples, FL 34110, and serves clients across Naples, Southwest Florida, and all 50 states. Our team of Enrolled Agents, CPAs, and tax attorneys helps with estimated tax planning, Form 2210 penalty review, and IRS resolution. Call (239) 441-2005 to discuss your situation.

Get help with estimated taxes and IRS penalties

Estimated taxes trip up even sophisticated earners, especially in years with uneven income, a business sale, or a large gain. Tax Expert Today helps individuals and business owners set safe harbor payment plans, apply the annualized income method, and, when a penalty has already hit, pursue waivers and resolution. You can also re-run the underpayment penalty calculator above any time your income or withholding changes.

Call (239) 441-2005 or schedule a consultation to review your estimated taxes and Form 2210 exposure. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Disclaimer: This calculator and article are provided for general educational purposes only and produce estimates, not a determination of tax owed. They do not constitute tax, legal, or financial advice, and using them does not create a client relationship. Penalty rules under IRC §6654 are fact-specific, interest rates change quarterly, and your actual liability is determined by the IRS based on your complete return. Consult a qualified tax professional about your situation. See our full disclaimer.

Self-employed? Estimate your Social Security and Medicare bill first with our free self-employment tax calculator.

Published June 2, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005