By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Self-employment tax for 2026 is 15.3 percent of 92.35 percent of net self-employment profit: 12.4 percent for Social Security on the first $184,500 of combined wages and net earnings, plus 2.9 percent for Medicare on every dollar of net earnings. Higher earners add a 0.9 percent Additional Medicare Tax, and one-half of the base tax is deductible. The calculator below runs your exact numbers.

A reliable self employment tax calculator answers the question every freelancer, contractor, and small business owner asks at some point: how much of my profit goes to Social Security and Medicare? The answer is more involved than multiplying by 15.3 percent. The tax applies to 92.35 percent of net profit, the Social Security portion stops at an annual wage base, W-2 wages from a day job change the math, and high earners pick up an extra 0.9 percent Medicare layer. This 2026 guide includes the calculator, the exact formula behind it, and the coordination rules most online tools skip.

All figures reflect tax year 2026, including the $184,500 Social Security wage base. Last updated: July 11, 2026.

Self-Employment Tax Calculator (2026)

Estimate your 2026 self-employment tax, including the Social Security wage base, the Additional Medicare Tax, and your deduction for one-half of the tax.

Estimate only. The total shown combines Schedule SE tax plus any Additional Medicare Tax attributable to your self-employment income. It does not include federal or state income tax, and it assumes the W-2 wages entered are your Social Security and Medicare wages for the full year. Your exact liability depends on your complete return.

Ask a tax expert what you actually owe → Call (239) 441-2005How Much Is Self-Employment Tax in 2026?

Self-employment tax for 2026 is 15.3 percent of 92.35 percent of your net self-employment profit: 12.4 percent for Social Security on the first $184,500 of combined wages and net earnings, plus 2.9 percent for Medicare with no ceiling. A 0.9 percent Additional Medicare Tax applies above $200,000 for single filers or $250,000 for joint filers, and one-half of the base tax is deductible.

What Is Self-Employment Tax?

Self-employment tax is the Social Security and Medicare tax paid by people who work for themselves, computed on Schedule SE under IRC Section 1401. It replaces the FICA tax split between employer and employee on a W-2, which is why the self-employed pay both halves: 12.4 percent for Social Security plus 2.9 percent for Medicare.

The tax applies to net earnings from a sole proprietorship, a single-member LLC, independent contractor or gig income reported on a 1099, and a general partner’s share of partnership income. It is separate from, and in addition to, federal income tax. An employee earning $80,000 sees 7.65 percent come out of each paycheck while the employer quietly pays the other 7.65 percent. A freelancer with the same $80,000 of profit writes the check for both sides. The deduction for one-half of the tax, described below, is the code’s way of putting the self-employed back on roughly equal footing with the employer side of that arrangement.

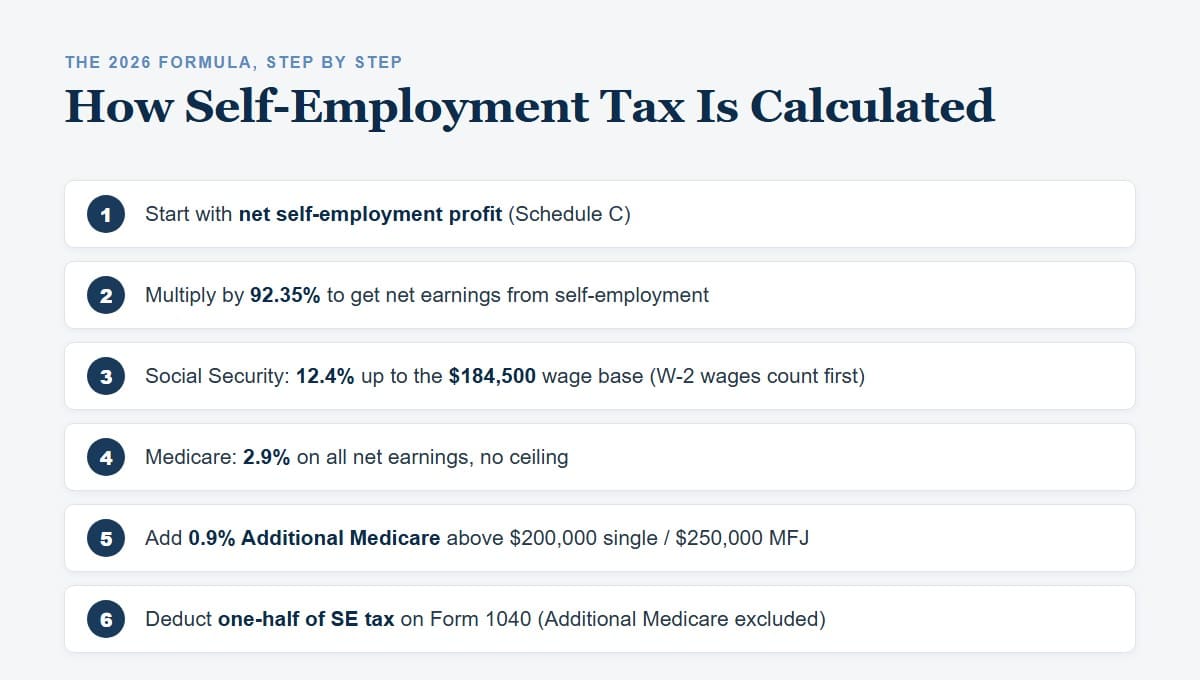

How Is Self-Employment Tax Calculated in 2026?

Multiply net self-employment profit by 92.35 percent to get net earnings, then apply 12.4 percent Social Security tax to net earnings up to the $184,500 wage base and 2.9 percent Medicare tax to every dollar of net earnings. One-half of the result is deductible as an adjustment to income on Schedule 1.

The 92.35 percent factor exists because employees do not pay FICA on the employer’s share of FICA. Per IRS Publication 334, you multiply self-employment earnings by 92.35 percent (0.9235) before applying the rates, which mirrors that employer-side exclusion. If net earnings after the 92.35 percent step are under $400, no self-employment tax is due at all.

Here is the full 2026 computation for a single filer with $100,000 of net Schedule C profit and no W-2 wages:

| Step | Computation | Amount |

|---|---|---|

| Net earnings | $100,000 × 92.35% | $92,350.00 |

| Social Security portion | $92,350 × 12.4% (under the $184,500 base) | $11,451.40 |

| Medicare portion | $92,350 × 2.9% | $2,678.15 |

| Additional Medicare Tax | Under the $200,000 threshold | $0.00 |

| Deduction for one-half of SE tax | $14,129.55 ÷ 2 | $7,064.78 |

| Total self-employment tax | Effective rate 14.13% of profit | $14,129.55 |

Two practical notes on that table. First, the deduction for one-half of self-employment tax reduces adjusted gross income, not the self-employment tax itself; the IRS describes it as deducting the employer-equivalent portion. Second, the Additional Medicare Tax is never deductible, and it is computed on Form 8959 rather than Schedule SE.

How Do W-2 Wages Affect Self-Employment Tax?

W-2 wages count against the $184,500 Social Security wage base first. Only the remaining room in the base is exposed to the 12.4 percent portion of self-employment tax, so a side business on top of a high salary may owe little or no Social Security portion. The 2.9 percent Medicare portion still applies to all net earnings.

The same coordination applies to the Additional Medicare Tax, in the order set out in IRS Topic 560: wages soak up the threshold first, then self-employment income is measured against whatever threshold remains. A single filer with $150,000 of wages has only $50,000 of threshold left, so self-employment net earnings above $50,000 pick up the extra 0.9 percent even though neither income stream crosses $200,000 on its own. The calculator above runs both coordination rules automatically, which is exactly where most generic tools and back-of-envelope estimates go wrong.

What Income Is Not Subject to Self-Employment Tax?

Capital gains, dividends, interest, and other investment income are outside self-employment tax, and so is most rental real estate income unless you are a dealer or provide substantial services such as those of a hotel. S corporation pass-through income and distributions are not self-employment income, and a limited partner’s distributive share is generally excluded under IRC Section 1402(a)(13). Wages already taxed through payroll withholding never run through Schedule SE.

The lines are factual, not elective. An active LLC member who works the business full time cannot simply claim limited partner treatment, and the IRS has litigated that boundary repeatedly. Likewise, calling a short-term rental passive does not survive scrutiny when guest services make it look like a hospitality business. When a material amount of income sits near one of these lines, the classification deserves professional review before the return is filed.

Do I Have to Make Quarterly Estimated Payments on Self-Employment Tax?

Generally yes. Self-employment tax has no withholding, so it is paid through quarterly estimated payments under IRC Section 6654, due in April, June, September, and January. If total tax due at filing is $1,000 or more and safe harbor payments were missed, the IRS charges an underpayment penalty computed at its quarterly interest rate. To split your projected tax into four dated installments, use our quarterly estimated tax calculator.

Self-employment tax is the reason so many first-year freelancers get blindsided in April: income tax may be modest at lower profit levels, but the 15.3 percent layer starts from the first $400 of net earnings. Run your safe harbor math with our IRS underpayment penalty calculator, and if a prior-year balance is already accruing, our IRS penalty and interest calculator shows what waiting costs.

When Are the 2026 Estimated Payment Deadlines?

For the 2026 tax year the four estimated payment deadlines fall in April, June, and September of 2026 and January of 2027. The safe harbor rules under the IRS estimated tax rules protect you from the underpayment penalty when you pay at least 90 percent of the current year tax, or 100 percent of the prior year tax, which rises to 110 percent when prior year adjusted gross income exceeded $150,000.

| Installment | Income period covered | Due date |

|---|---|---|

| First | January through March 2026 | April 15, 2026 |

| Second | April through May 2026 | June 15, 2026 |

| Third | June through August 2026 | September 15, 2026 |

| Fourth | September through December 2026 | January 15, 2027 |

The installments are not true calendar quarters, which is why the June payment surprises so many first-year filers only two months after the April one. Income that arrives unevenly can be annualized on Form 2210 so the payments track when the money actually came in, a technique that matters for seasonal businesses and for anyone whose fourth quarter dwarfs the first.

How Can I Reduce Self-Employment Tax?

The main levers are maximizing legitimate business deductions to lower net profit, and for profitable businesses, evaluating an S corporation election. An S corporation pays FICA only on a reasonable salary, not on the full profit, which can meaningfully reduce the combined Social Security and Medicare cost in the right circumstances.

The S corporation route is powerful but not automatic. The IRS requires reasonable compensation for the owner’s work, payroll adds real administrative cost, and a lower salary can reduce future Social Security benefits and retirement plan contribution room. Whether the election makes sense depends on profit level, state, and long-term goals, which is a modeling exercise rather than a rule of thumb. Our Naples tax planning team runs that analysis as part of a broader tax planning engagement, alongside retirement plan design, the qualified business income deduction, and health insurance deductions for the self-employed.

Does the QBI Deduction Reduce Self-Employment Tax?

No. The qualified business income deduction of up to 20 percent reduces income tax only; self-employment tax is computed on Schedule SE before that deduction is applied. A freelancer can wipe out a large share of income tax through the QBI deduction and still owe the full 15.3 percent layer on the same profit.

The two provisions do interact in one direction: the deduction for one-half of self-employment tax reduces qualified business income, which slightly trims the QBI deduction itself. The calculator above isolates the self-employment side so that number is right before the income tax layers are stacked on top of it.

Self-Employment Tax Help in Naples and Southwest Florida

Tax Expert Today works with self-employed professionals, contractors, and small business owners across Naples, Bonita Springs, Estero, Fort Myers, and Marco Island, and with clients in all 50 states. Southwest Florida runs on independent businesses: realtors, charter captains, medical and dental practices, consultants, and seasonal residents who bring a Schedule C with them from up north.

Visit us at 11983 Tamiami Trail N, Naples, FL 34110, call (239) 441-2005, Monday through Friday, 10am to 5pm Eastern.

Does Florida charge its own self-employment tax?

No. Florida has no state income tax and no state-level self-employment tax, so Naples freelancers and business owners pay only the federal 15.3 percent structure. That is one reason relocating a business to Southwest Florida can lower the total tax picture, though the federal self-employment tax follows you to any state.

When to Engage a Professional

A calculator handles the arithmetic. It cannot tell you whether your worker classification is defensible, whether an S corporation election would survive a reasonable compensation review, how a mid-year move or a mix of K-1 and W-2 income changes the answer, or how to catch up cleanly after a year of missed estimates. Those calls depend on your complete facts, and getting them wrong tends to cost more than getting advice early.

Tax Expert Today can review your self-employment income, run the entity and estimated payment analysis, and prepare the filings. Call (239) 441-2005 or schedule a consultation here. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Frequently Asked Questions

What is the self-employment tax rate for 2026?

The 2026 self-employment tax rate is 15.3 percent, made up of 12.4 percent for Social Security and 2.9 percent for Medicare, applied to 92.35 percent of net self-employment profit. The Social Security portion stops at $184,500 of combined wages and net earnings; the Medicare portion has no cap.

Do I pay self-employment tax if I also have a W-2 job?

Yes, on your self-employment profit, but your W-2 wages use up the $184,500 Social Security wage base first. If wages already exceed the base, you owe only the 2.9 percent Medicare portion, plus the 0.9 percent Additional Medicare Tax on income above your filing status threshold.

Is any part of self-employment tax deductible?

Yes. You can deduct one-half of your self-employment tax, the employer-equivalent portion, as an adjustment to income on Schedule 1. The deduction reduces your income tax but not the self-employment tax itself, and it does not require itemizing. The 0.9 percent Additional Medicare Tax is not deductible.

Who has to file Schedule SE?

Anyone with net earnings from self-employment of $400 or more for the year must file Schedule SE and pay self-employment tax, even if no income tax is otherwise due. That includes sole proprietors, single-member LLC owners, independent contractors, gig workers, and general partners reporting a share of partnership income.

Texas business owners can also review how the entity itself is taxed in our guide to Texas LLC taxes, which covers franchise tax, pass-through treatment, and the S corporation election.

Published July 11, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005