By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: An IRS bank levy release is the IRS lifting the freeze it placed on your bank account so the money is unfrozen or returned. Under IRC Section 6332(c), your bank must hold the levied funds for 21 days before sending them to the IRS, which gives you a window to act. You can request a release under IRC Section 6343 by paying the balance, entering an installment agreement, proving economic hardship, or showing the levy was improper.

Published: June 2026

Few collection actions feel as alarming as logging in to find your bank account frozen by the IRS. A bank levy seizes the funds on deposit to satisfy an unpaid tax balance, and the money is not gone the instant the freeze appears — federal law gives you a short, fixed window to respond before the bank forwards anything to the IRS. This 2026 guide explains what an IRS bank levy is, how the 21-day holding period under IRC Section 6332(c) works, how to request a release under Section 6343, whether you can recover money the IRS has already taken, and how to keep the next levy from happening.

What Is an IRS Bank Levy?

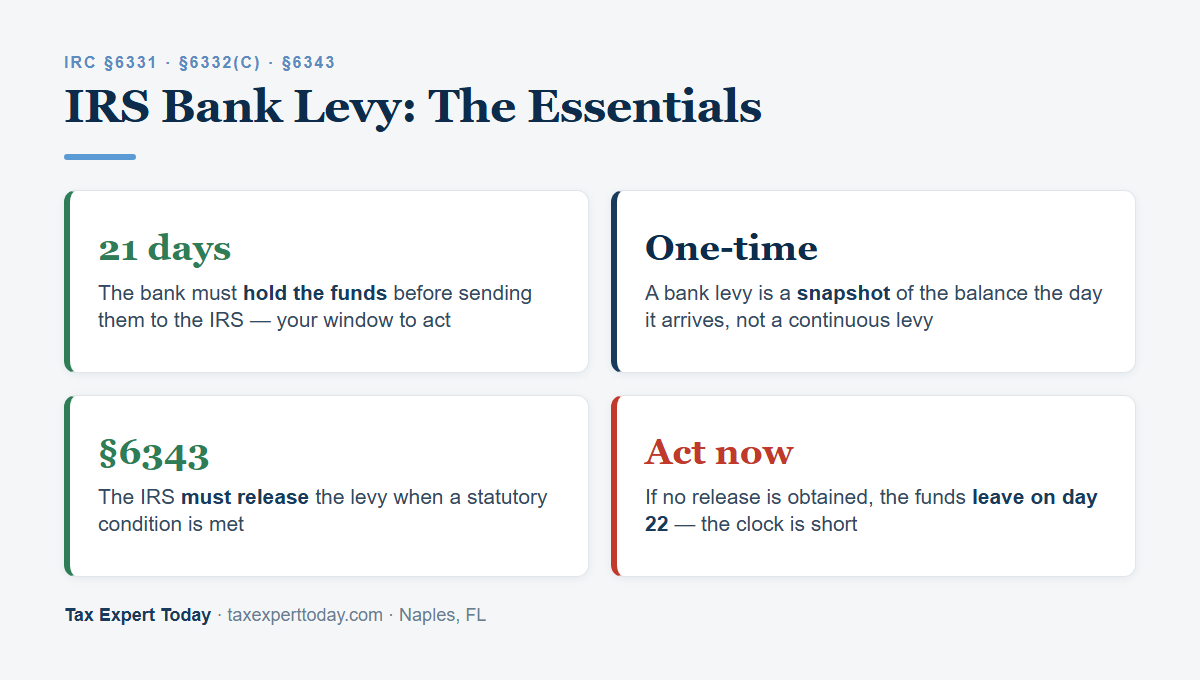

An IRS bank levy is a legal seizure of the money in your bank account to satisfy an unpaid tax debt, authorized under IRC Section 6331. When the IRS sends a levy notice to your bank, the bank freezes the account balance up to the amount you owe as of the day the levy arrives, then holds those funds before remitting them to the IRS.

A bank levy is a one-time snapshot, which is an important distinction. It reaches only the funds in the account on the day the levy is received; deposits you make afterward are not captured unless the IRS issues another levy. That makes it different from a continuous wage levy, which attaches to each paycheck until it is released — the mechanics of that situation are covered in our guide to the IRS wage garnishment. A bank levy almost never arrives without warning: it generally follows the collection notice sequence and the final notice of intent to levy, explained in our guide to IRS Letter 1058 / LT11 and your Collection Due Process rights.

How Long Before the Bank Sends My Money to the IRS?

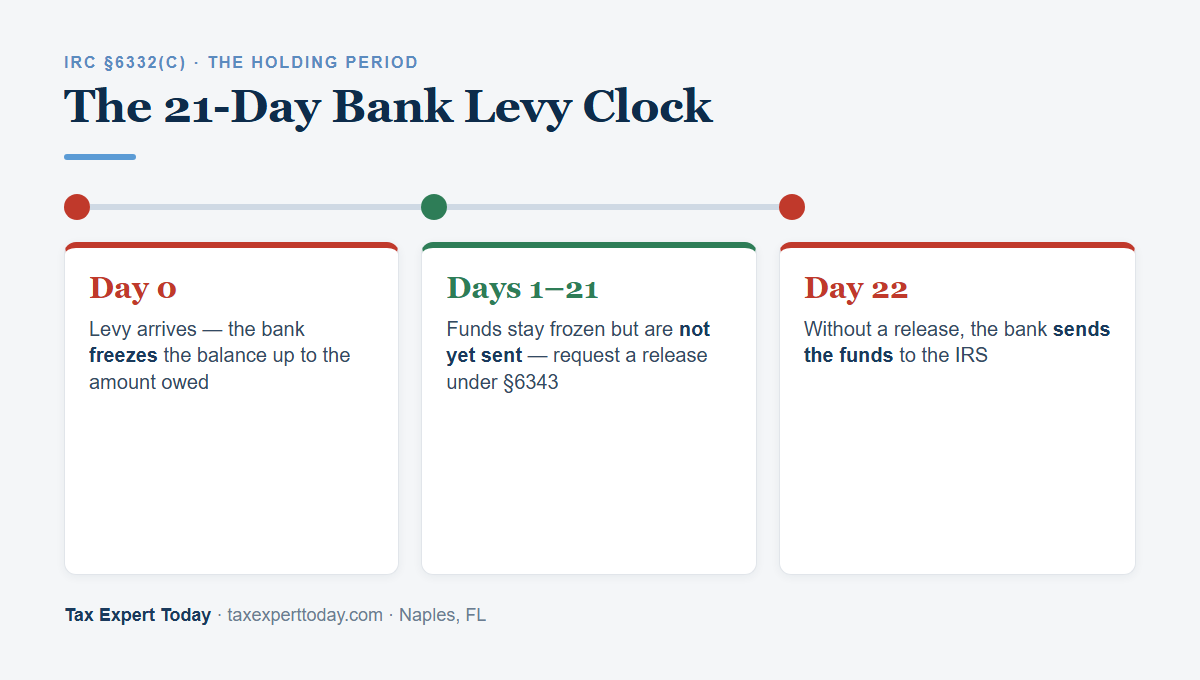

The bank must wait 21 calendar days after receiving the levy before sending the frozen funds to the IRS, under IRC Section 6332(c). Congress built in this holding period specifically so that taxpayers have time to correct a mistake, prove a hardship, or arrange a release before the money leaves the account. The 21-day clock starts the day the bank processes the levy, not the day you discover it.

| Stage | What happens | What you can do |

|---|---|---|

| Day 0 — levy received | The bank freezes the balance up to the amount owed; you cannot withdraw the frozen funds | Confirm the levy amount and contact the IRS revenue officer or the number on the notice |

| Days 1–21 — holding period | The funds stay frozen at the bank but are not yet sent to the IRS | Request a release under §6343 — pay, arrange a plan, or document hardship |

| Day 22 — remittance | If no release is obtained, the bank sends the frozen funds to the IRS | Pursue return of property under §6343(d) if the levy was wrongful or caused hardship |

The practical lesson is that the 21 days are the most valuable part of the process, and they pass quickly. Because the bank acts on the date the levy arrives, the window may already be partly spent by the time the freeze shows up in your account, so the response should begin immediately rather than waiting for a letter in the mail.

How Do I Request an IRS Bank Levy Release?

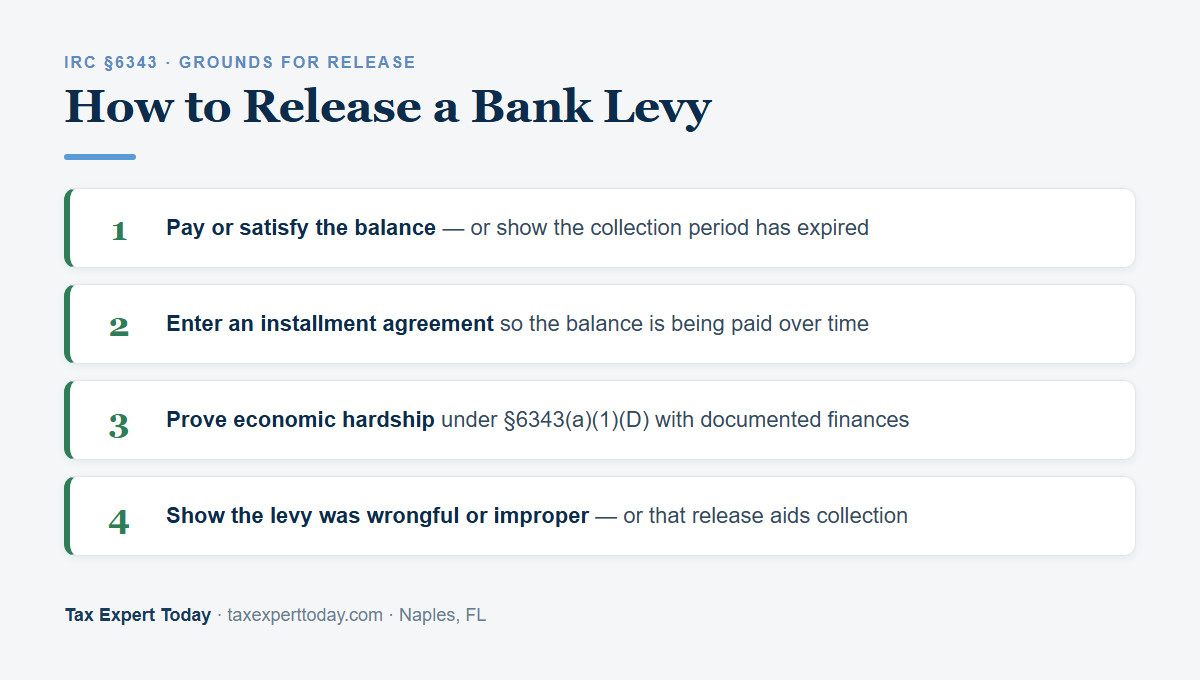

You request an IRS bank levy release under IRC Section 6343 by resolving the underlying issue: paying the balance in full, entering an installment agreement, demonstrating that the levy creates an economic hardship, or showing the levy was issued in error. When one of the statutory conditions in Section 6343(a) is met, the IRS is required to release the levy.

- Pay the balance or show it is satisfied

- If the liability is paid, or the collection period has expired, the IRS must release the levy. This also applies when the levy was issued for an amount that was already resolved.

- Enter an installment agreement

- Setting up a payment plan generally leads the IRS to release an active levy, because the balance is being addressed through agreed monthly payments. Our guide to IRS installment agreement options walks through the plan types and how to apply.

- Demonstrate economic hardship

- Under Section 6343(a)(1)(D), the IRS must release a levy that creates an economic hardship — meaning it prevents you from meeting basic, reasonable living expenses. This requires documenting your income, expenses, and assets to the IRS.

- Show the levy facilitates collection less than a release would

- If releasing the levy would actually help you pay the debt — for example, by letting a business keep operating — that is a recognized ground for release under Section 6343.

- Resolve through an offer in compromise

- A pending or accepted offer in compromise can support release of a levy while the IRS evaluates the offer, depending on the facts.

Speed matters here. Once the IRS agrees to release the levy, it can transmit the release to your bank, but that has to happen within the 21-day window to free the still-frozen funds. Knowing which ground actually applies to your situation — and assembling the financial documentation the IRS will require — is where preparation makes the difference between a release that lands in time and one that does not.

Can I Recover Money the IRS Already Took?

In some cases, yes. If the 21-day period has passed and the bank has already sent the funds to the IRS, recovery is harder but not always impossible. Under IRC Section 6343(d), the IRS has authority to return levied property, and a person whose property was wrongfully levied may pursue a separate claim under Section 6343(b).

Two situations are worth separating. A wrongful levy arises when the IRS levies property that did not belong to the taxpayer or in which a third party had a superior interest — for instance, funds in a joint or fiduciary account that belonged to someone else. The affected party can file a wrongful-levy claim, generally subject to a statutory deadline. Return of property under Section 6343(d) is broader but discretionary: the IRS may return the proceeds of a levy if it was premature, did not follow IRS procedures, or if return would facilitate collection or be in the best interests of the taxpayer and the government, and the request must be made within the time limits set by statute. Because both paths are fact-specific and time-limited, they should be evaluated quickly rather than assumed to be available later.

How Can I Prevent the Next Bank Levy?

The most reliable way to prevent a bank levy is to engage with the IRS before it reaches the levy stage. A levy generally cannot be issued until the IRS sends a final notice of intent to levy and notice of your right to a hearing under IRC Section 6330, which gives you 30 days to request a Collection Due Process hearing.

That 30-day window is the single most powerful tool for stopping enforced collection, because a timely hearing request generally suspends levy action while your case is reviewed and lets you propose alternatives such as a payment plan or currently not collectible status. The steps are explained in our guide to the LT11 final notice and CDP rights. If you have already missed that window, setting up an installment agreement or establishing that you cannot currently pay are the usual ways to take a levy off the table going forward.

IRS Bank Levy Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to bank levies — confirming the levy amount, identifying the release ground that fits the facts, preparing the financial documentation the IRS requires, and requesting the release within the 21-day window. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 9am to 5pm ET.

Frequently Asked Questions

How much can the IRS take from my bank account?

A bank levy reaches the funds on deposit up to the amount you owe as of the day the levy arrives at the bank. It is a one-time snapshot, so it captures the balance present that day, not money you deposit afterward. If the frozen balance does not cover the full liability, the IRS can issue a new levy later to reach additional deposits, which is why resolving the underlying balance matters more than any single levy.

Is a bank levy the same as a wage garnishment?

No. A bank levy is a one-time seizure of the funds in your account on the day it is received, while a wage garnishment is a continuous levy that attaches to each paycheck until the balance is paid or the levy is released. They are issued under the same levy authority but work differently. If your wages are being levied rather than your bank account, our guide on how to stop an IRS wage garnishment explains the exempt-amount rules and release options.

How long does it take to get a bank levy released?

It depends on how quickly the underlying issue can be resolved and the documentation provided. Once the IRS agrees to a release, it can send the release to your bank promptly, but that has to occur within the 21-day holding period under IRC Section 6332(c) to free the frozen funds. Acting on the first day the freeze appears, rather than waiting, gives the best chance of a release that reaches the bank in time.

Can the IRS levy my bank account without notice?

In most cases, no. The IRS generally must send a final notice of intent to levy and notice of your Collection Due Process rights under IRC Section 6330 at least 30 days before levying. There are limited exceptions, such as a jeopardy levy when collection is at risk, a levy on a state tax refund, or a disqualified employment tax levy, but the ordinary bank levy follows the notice sequence and the 30-day CDP window.

Where can I get help with an IRS bank levy in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with IRS bank levies, identifying the release ground that fits the situation, preparing the required financial documentation, and requesting release within the 21-day period. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a Bank Levy

A bank levy runs on a 21-day clock, and the right response depends on facts the IRS will want documented: which release ground applies, whether the levy was wrongful, and what financial information supports a hardship claim. Those judgment calls — made under time pressure, with frozen funds — are where professional representation helps most, because a release request that is incomplete or aimed at the wrong ground can miss the window entirely. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review the levy, identify the release ground that fits your facts, and request the release before the holding period ends. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 25, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005