By Dr. Pellumb Kabashi, DBA, MBA, EA, CFE, CES

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: An IRS CP2000 notice is a proposed change to your tax return generated when income reported to the IRS by third parties, such as employers and banks, does not match the income on your filed return. It is produced by the IRS Automated Underreporter program and is not a formal audit. The notice shows the proposed additional tax, and often an accuracy-related penalty under IRC Section 6662 and interest, and it asks you to agree or disagree by a stated deadline, usually 30 days. Responding on time is what keeps the matter from becoming a formal notice of deficiency.

Published: July 9, 2026

Few pieces of IRS mail cause more confusion than the CP2000. It arrives looking like a bill, it proposes extra tax and penalties, and it references income you may not remember. Yet it is one of the most routine notices the IRS sends, and it is often resolved with a single well-documented response. This 2026 guide explains what an IRS CP2000 notice is, why it is not the same as an audit, how to respond whether you agree or disagree, and what happens if the notice is ignored. It builds on our guide to the CP14 notice, which is where a confirmed balance begins its collection life.

What Is an IRS CP2000 Notice?

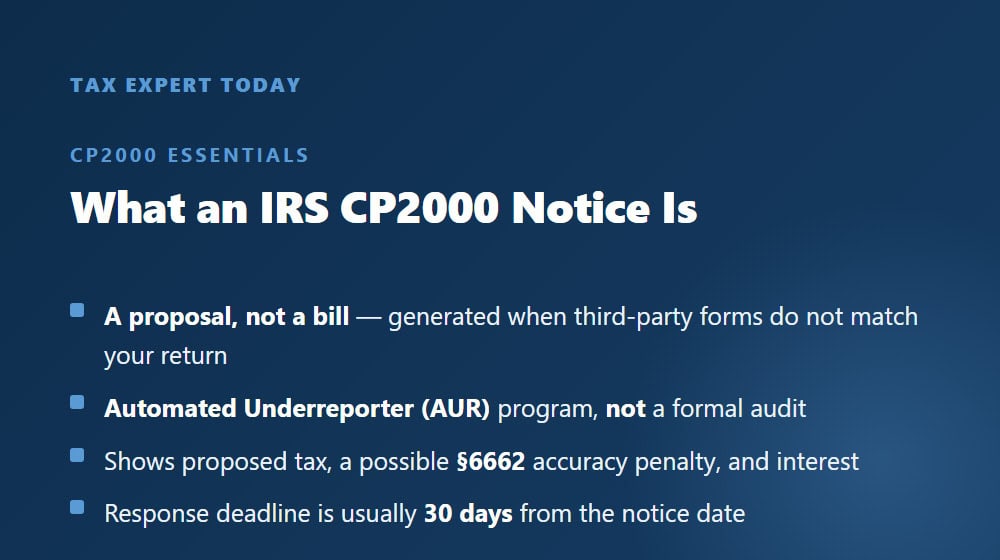

An IRS CP2000 notice is a proposed adjustment to your return that the IRS sends when the income and payment information reported to it by third parties does not match what you reported. It is generated by the Automated Underreporter (AUR) program, which compares the amounts on forms such as W-2, 1099-NEC, 1099-INT, 1099-DIV, 1099-B, and 1099-K against your filed return, as described in IRS Tax Topic 652. When the computer finds a discrepancy, it proposes the tax that would result if the third-party figures are correct.

The notice is a proposal, not a final assessment. It lays out the specific items in question, the proposed change to your tax, any accuracy-related penalty under IRC Section 6662, and interest, and it gives you a response deadline that is generally 30 days from the date on the notice. Because it is only a proposal, you retain the right to agree, to disagree in whole or in part, and to submit documentation, all of which the IRS explains on its Understanding Your CP2000 Series Notice page.

Is a CP2000 an Audit?

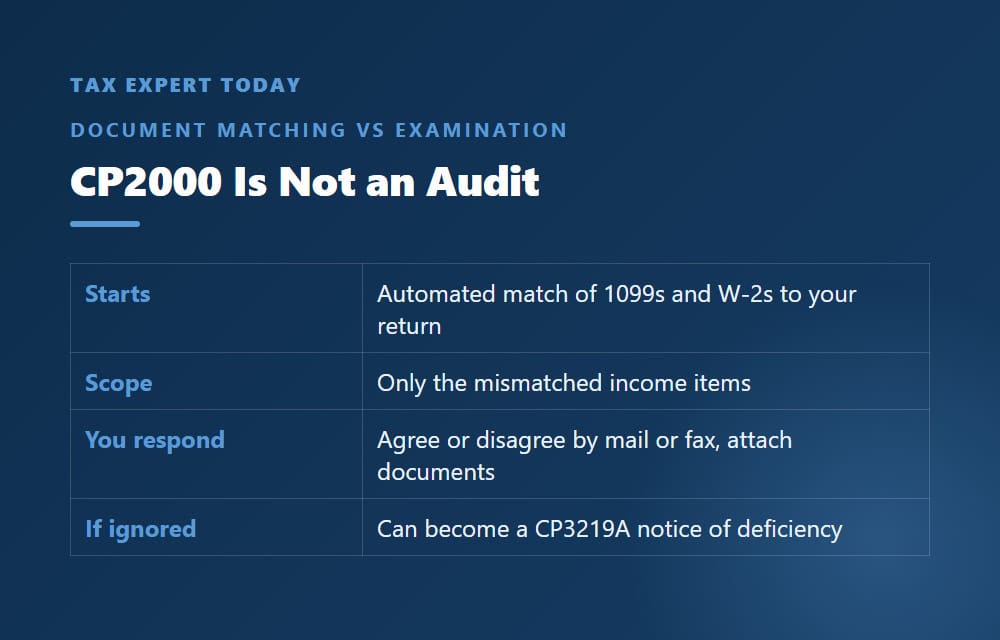

No. A CP2000 is a document-matching notice, not an audit. An audit, or examination, is a formal review in which the IRS asks you to substantiate items on your return and can look broadly at your books and records. A CP2000 is narrower and automated: it flags only the specific income items where third-party reporting and your return disagree, and it proposes a fix based on those items alone.

The distinction matters because it changes how you respond. An audit involves examination procedures and an examiner; a CP2000 is answered by mail or fax to the AUR unit, usually with a copy of the notice, a short explanation, and supporting documents. That said, an unresolved CP2000 does not simply disappear. If it is not answered, it can progress into the formal deficiency process under IRC Section 6213, which carries its own deadlines and appeal rights.

| Feature | CP2000 (document matching) | Audit (examination) |

|---|---|---|

| How it starts | Automated match of third-party forms to your return | Selection for formal review of return items |

| Scope | Only the mismatched income items | Can extend to books, records, and multiple issues |

| How you respond | Return the response form, agree or disagree, attach documents | Work with an examiner under examination procedures |

| If unresolved | Can become a CP3219A notice of deficiency | Closes with an examination report and appeal rights |

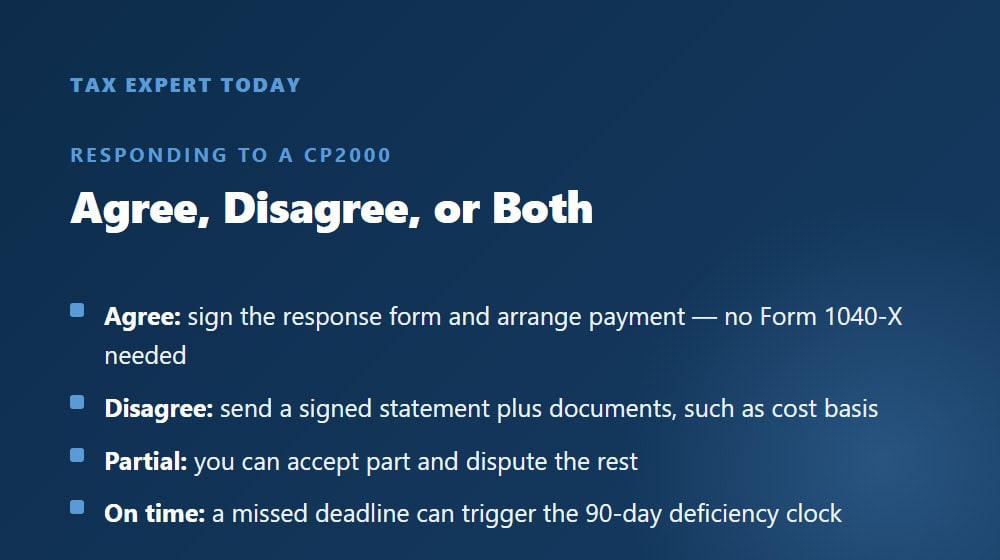

How Do I Respond If I Agree?

If you agree with the CP2000, you sign and return the response form that comes with the notice, indicating agreement, and you arrange to pay or set up a payment plan for the additional tax, penalty, and interest. Signing the agreement authorizes the IRS to assess the proposed amount, so you generally do not need to file an amended return for the items the CP2000 already covers. In fact, filing a Form 1040-X for those same items can duplicate the adjustment and slow processing.

If you cannot pay the full balance, you can still agree with the adjustment and address payment separately. Once the tax is assessed, the options are the same as for any balance due: an installment agreement to pay over time, or, in qualifying hardship cases, other collection alternatives. Agreeing to the tax and arranging payment are two separate steps, and it is usually better to respond on time even if payment will take longer to arrange.

How Do I Respond If I Disagree?

If you disagree with all or part of a CP2000, you check the disagree box on the response form and send a signed statement explaining why, together with documents that support your position, before the deadline on the notice. The most common reasons a CP2000 is wrong include income that was actually reported under a different line or entity, a cost basis the IRS did not have for a securities sale, income that belongs to someone else because of a duplicate or incorrect information return, or amounts that were already reported but offset by deductions the AUR match did not see.

Documentation is what wins these responses. For a securities sale flagged on a 1099-B, that means showing your basis so only the actual gain is taxed rather than the full proceeds. For a mismatched 1099, it may mean a corrected form from the issuer or records showing where the income appeared on your return. You can agree with part of the notice and dispute the rest; the response form allows a partial agreement. If a change to your return is genuinely warranted for items the CP2000 did not raise, that is the situation where a Form 1040-X may be appropriate, filed alongside the CP2000 response rather than in place of it.

What Happens If I Ignore a CP2000?

If you do not respond to a CP2000 by the deadline, the IRS generally issues a Notice CP3219A, a statutory notice of deficiency, which is the formal step that follows an unresolved proposal. As the IRS explains on its Understanding Your CP3219A Notice page, this notice gives you 90 days to petition the United States Tax Court if you still disagree, a right created by IRC Section 6213. This 90-day window is often called the ticket to Tax Court, and it cannot be extended.

If you let the 90 days pass without either resolving the issue or petitioning the Tax Court, the IRS assesses the tax, and the balance moves into normal collection. From there it follows the notice sequence that leads to a CP14 balance-due notice and, if still unpaid, enforced collection. Ignoring the original CP2000 does not make the proposed tax go away; it removes the easier, documentation-based chances to correct or reduce it.

Can the Accuracy Penalty Be Removed?

A CP2000 frequently includes a 20 percent accuracy-related penalty under IRC Section 6662, which applies to a substantial understatement of income tax or to negligence. This penalty can sometimes be reduced or removed, but it is handled separately from the tax itself, and eligibility depends on the facts. The two main paths are showing that the underlying adjustment is wrong, which removes the penalty base along with the tax, or establishing reasonable cause.

Reasonable cause means showing that you acted in good faith and that the omission had a reasonable explanation, such as reliance on a corrected or missing information return, and it is discussed in our guide to reasonable cause for IRS penalties. Separately, the accuracy penalty is not eligible for first-time penalty abatement, which applies to failure-to-file and failure-to-pay penalties rather than the Section 6662 penalty; our overview of how to get IRS penalties removed explains which relief applies to which penalty. Because the accuracy penalty is fact-specific, the CP2000 response is the natural place to raise it, since resolving the income issue and the penalty together is usually more efficient than addressing them in separate letters. For the mechanics of that penalty, our detailed page on the accuracy-related penalty walks through how it is calculated.

IRS CP2000 Notice Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida read a CP2000 notice, confirm whether the proposed change is correct, and prepare a documented response before the deadline. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and it handles the two pieces that most often decide a CP2000, which are proving the correct income figure, including cost basis on securities sales, and addressing any accuracy-related penalty. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

What is an IRS CP2000 notice?

An IRS CP2000 notice is a proposed change to your tax return that the IRS sends when income reported to it by third parties does not match the income on your return. It is generated by the Automated Underreporter program, not by an auditor, and it shows the proposed additional tax, any accuracy-related penalty under IRC Section 6662, and interest. It asks you to agree or disagree by a deadline that is usually 30 days from the date on the notice.

Is a CP2000 the same as an audit?

No. A CP2000 is an automated document-matching notice, while an audit is a formal examination of your return. The CP2000 looks only at the specific income items where third-party forms and your return disagree, and it is answered by mail or fax to the Automated Underreporter unit. An audit is broader and involves an examiner. An unresolved CP2000 can, however, progress into the formal deficiency process.

Do I need to file an amended return to respond to a CP2000?

Usually not for the items the CP2000 already covers. If you agree, signing the response form authorizes the IRS to assess the proposed amount, and filing a Form 1040-X for the same items can duplicate the adjustment. A Form 1040-X may be appropriate only when a separate change to your return is warranted for items the CP2000 did not raise, and then it is filed alongside the response, not instead of it.

What happens if I ignore a CP2000 notice?

If you do not respond by the deadline, the IRS generally issues a CP3219A statutory notice of deficiency, which gives you 90 days to petition the United States Tax Court under IRC Section 6213. If that window passes without resolution or a Tax Court petition, the IRS assesses the tax and the balance moves into normal collection, eventually following the CP14 and later collection notices. The proposed tax does not go away simply because the CP2000 was ignored.

Where can I get help with a CP2000 notice in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with CP2000 notices, including confirming the proposed change, documenting the correct income and cost basis, and addressing any accuracy-related penalty. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a CP2000 Notice

A CP2000 rewards a timely, documented response, and the judgment calls are where a professional adds the most value: deciding whether the proposed change is actually correct, assembling the right proof of income and cost basis, allocating a partial agreement, and addressing the accuracy-related penalty in the same response rather than in a second round. Missing the deadline is what turns an easy correction into a notice of deficiency with a hard 90-day clock. Tax Expert Today LLC represents individuals and businesses in IRS notice and collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review a CP2000 notice and prepare a documented response before the deadline. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 9, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005