By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

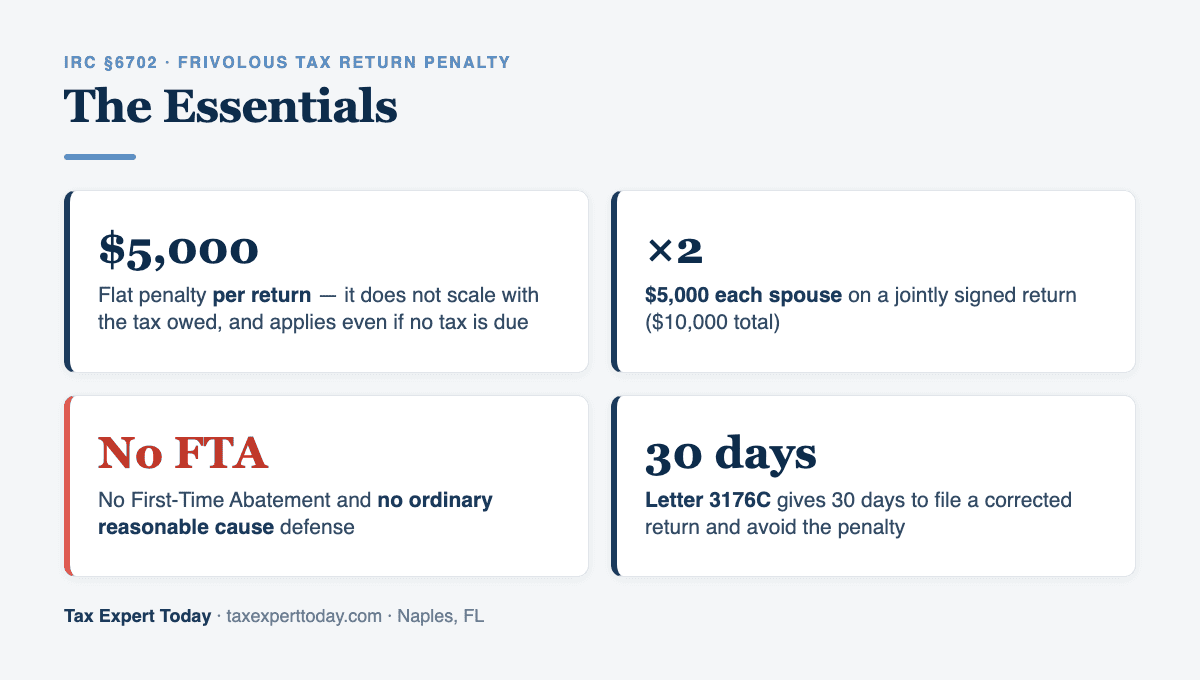

Quick Answer: The frivolous tax return penalty under IRC Section 6702 is a flat $5,000 charge the IRS assesses when a return or other submission takes a position the IRS has identified as frivolous, or is filed to delay or impede tax administration. It applies per return, so a married couple filing jointly can each be charged $5,000. It is separate from, and stacks on top of, the failure to file, failure to pay, and accuracy-related penalties. The IRS usually first sends Letter 3176C, which gives 30 days to file a corrected return and avoid the penalty.

Published: June 3, 2026

The frivolous return penalty is one of the harshest civil penalties in the Internal Revenue Code, and one of the few where First-Time Abatement and ordinary reasonable cause do not apply. It is aimed at tax-protester arguments and at filings designed to clog the system, not at honest mistakes or good-faith disputes. This 2026 guide explains what triggers the penalty under Internal Revenue Code Section 6702, which positions the IRS has formally labeled frivolous, what the Letter 3176C warning means, and the narrow paths to correct or challenge an assessment.

What Is the IRS Frivolous Tax Return Penalty?

The frivolous tax return penalty is a $5,000 civil penalty the IRS imposes under IRC Section 6702 when a taxpayer files a return or submission that either fails to contain enough information to judge whether the self-assessment is correct, or that is substantially incorrect on its face — and that conduct is based on a position the IRS has identified as frivolous or reflects a desire to delay or impede the administration of federal tax law. The two elements must both be present: a defective filing and a frivolous basis or obstructive intent.

This penalty is not for being wrong. A taxpayer who takes an aggressive but good-faith position on a genuine legal question is exposed to the accuracy-related penalty under IRC Section 6662, not Section 6702. The frivolous penalty targets a defined category of arguments — the kind the IRS lists in Notice 2010-33 and rebuts in its publication The Truth About Frivolous Tax Arguments. The penalty was raised from $500 to $5,000 by the Tax Relief and Health Care Act of 2006, which is when Congress signaled it would treat these filings as a serious compliance problem rather than a nuisance.

How Much Is the Frivolous Return Penalty?

The penalty is a flat $5,000 per frivolous return or submission, with no sliding scale and no cap that reduces it over time. Unlike the failure to pay penalty, which is a percentage that builds month by month, the frivolous penalty is assessed in full the moment the IRS determines the filing qualifies. The table below shows how the $5,000 charge applies across the situations covered by IRC Section 6702 and related sanction statutes.

| Trigger | Authority | Penalty |

|---|---|---|

| Frivolous income tax return | IRC 6702(a) | $5,000 per return |

| Specified frivolous submission (e.g., a CDP hearing request, installment agreement, or offer in compromise filed on a frivolous basis) | IRC 6702(b) | $5,000 per submission |

| Joint return signed by both spouses | IRC 6702(a) | $5,000 each ($10,000 total) |

| Frivolous or delay position in U.S. Tax Court | IRC 6673 | Up to $25,000 |

The frivolous penalty is in addition to any other penalty. A protester-style return filed late and unpaid can draw the failure to file penalty, the failure to pay penalty, the accuracy-related penalty, and the $5,000 frivolous penalty at the same time, plus daily interest under IRC Section 6601. The frivolous penalty also does not require that any tax actually be owed. A “zero return” reporting no income, filed to make a point rather than to report real figures, can trigger the full $5,000 even if the filer would have owed nothing on a correct return.

What Counts as a Frivolous Position?

A position is frivolous when the IRS has identified it as such in published guidance, currently Notice 2010-33, or when the filing has no purpose other than to delay or obstruct. The IRS does not decide this case by case from scratch — it works from a standing list of arguments that courts have rejected for decades. The most common ones I see surface in flagged returns are below.

- “Wages are not income”

- The claim that compensation for labor is an even exchange and therefore not taxable income. Courts have rejected this consistently; wages are gross income under IRC Section 61.

- “Filing is voluntary”

- The argument that the word “voluntary” in IRS materials means filing and paying are optional. It refers to the self-assessment system, not to whether the obligation exists.

- Constitutional and Sixteenth Amendment arguments

- Claims that the income tax violates the Constitution, that the Sixteenth Amendment was never properly ratified, or that filing violates the Fifth Amendment. All are listed as frivolous.

- “Only federal employees or federal income is taxable”

- The claim that only government workers, or only income from federal sources, is subject to tax. There is no such limitation in the Code.

- Zero returns and altered-form schemes

- Returns reporting all zeros despite real income, returns with a disclaimer striking the penalty-of-perjury statement, and Form 1099-OID “redemption” schemes that claim fictitious withholding. These are flagged both as frivolous positions and as filings that obstruct administration.

The full catalog of arguments, each paired with the statutes and court decisions that defeat it, is in the IRS document The Truth About Frivolous Tax Arguments. If a position appears there, treating it as a basis for a filing exposes the taxpayer to the $5,000 penalty regardless of how sincerely it is held.

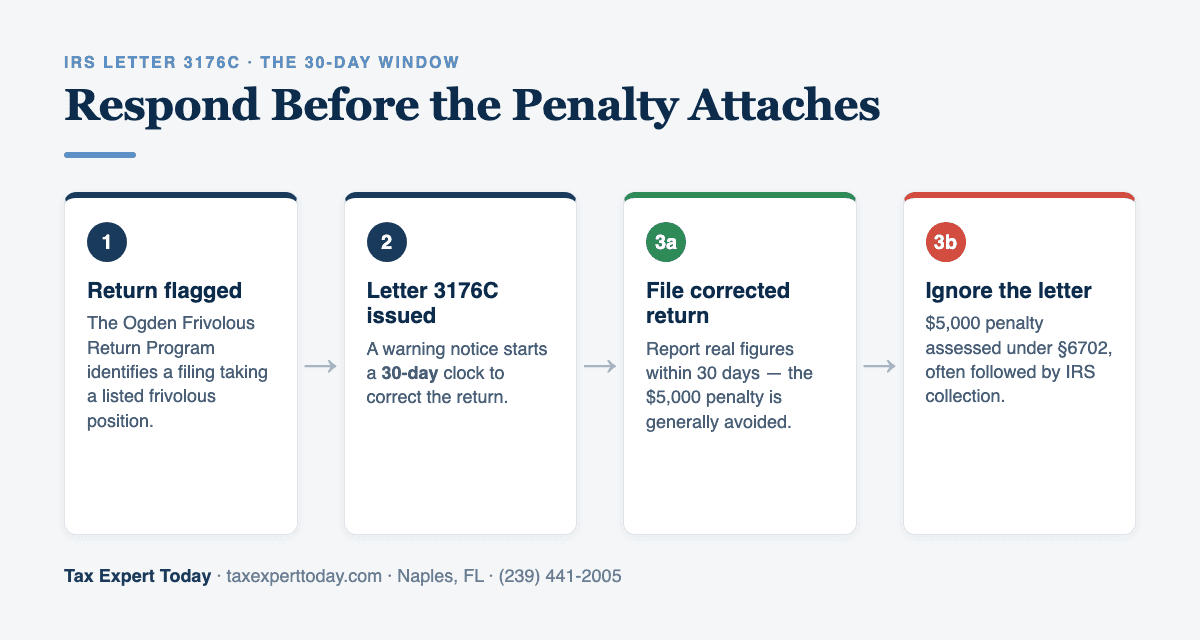

What Is IRS Letter 3176C and the 30-Day Warning?

Letter 3176C is the notice the IRS sends when it believes a filed return takes a frivolous position, and it gives the taxpayer 30 days to file a corrected, accurate return before the $5,000 penalty is assessed. The letter is issued by the IRS Frivolous Return Program unit in Ogden, Utah, which screens suspect filings. The 30-day correction window is the single most important feature of the process: a taxpayer who responds with a proper return reporting real figures generally avoids the penalty entirely.

The mistake I see most often is a taxpayer ignoring Letter 3176C, either because they do not understand it or because they got advice telling them to stand firm. Letting the 30 days lapse converts a warning into a $5,000 assessment, and the same letter often precedes the IRS preparing a substitute return and beginning collection. When a return was flagged because of a genuine error — a missing schedule, a misread entry, or a defective e-file rather than a protester argument — the correction response is also where that gets resolved before the penalty attaches.

How Do You Remove or Challenge a Frivolous Return Penalty?

Removing a frivolous penalty is harder than removing most penalties, because First-Time Abatement and the ordinary reasonable cause defense do not apply to IRC Section 6702. There is no clean-compliance-history waiver and no “serious illness” excuse here, because the penalty turns on the position taken rather than on a missed deadline. Three realistic paths exist, in order of preference.

- Correct the return within the Letter 3176C window. Filing an accurate return within the 30 days stated in the letter is the cleanest resolution and usually prevents the penalty from being assessed at all. This is the path that matters most, and it is time-sensitive.

- Request reduction under IRC Section 6702(d). The IRS has discretionary authority to reduce the penalty when doing so would promote compliance with and administration of the tax laws. A taxpayer who has since filed correctly and come into full compliance can ask the IRS to exercise this authority, in writing, with Form 843.

- Use the IRC Section 6703 pay-and-claim procedure. To contest the penalty in court, the taxpayer pays 15% of the penalty within 30 days of notice and demand and files a claim for refund under IRC Section 6703. If the claim is denied or six months pass, the taxpayer has 30 days to file suit in U.S. district court. A useful feature of Section 6703: the burden of proof that a submission is frivolous rests on the IRS, not the taxpayer.

One caution that applies throughout: arguing the merits of a frivolous position to the IRS or the courts does not remove the penalty — it risks adding the up-to-$25,000 Tax Court penalty under IRC Section 6673. The productive response is to abandon the position, file correctly, and then seek reduction or refund on procedural grounds. For penalties that do qualify for the standard waivers, the sequencing is different and is covered in our guide on how to get IRS penalties removed and our reasonable cause IRS penalty guide.

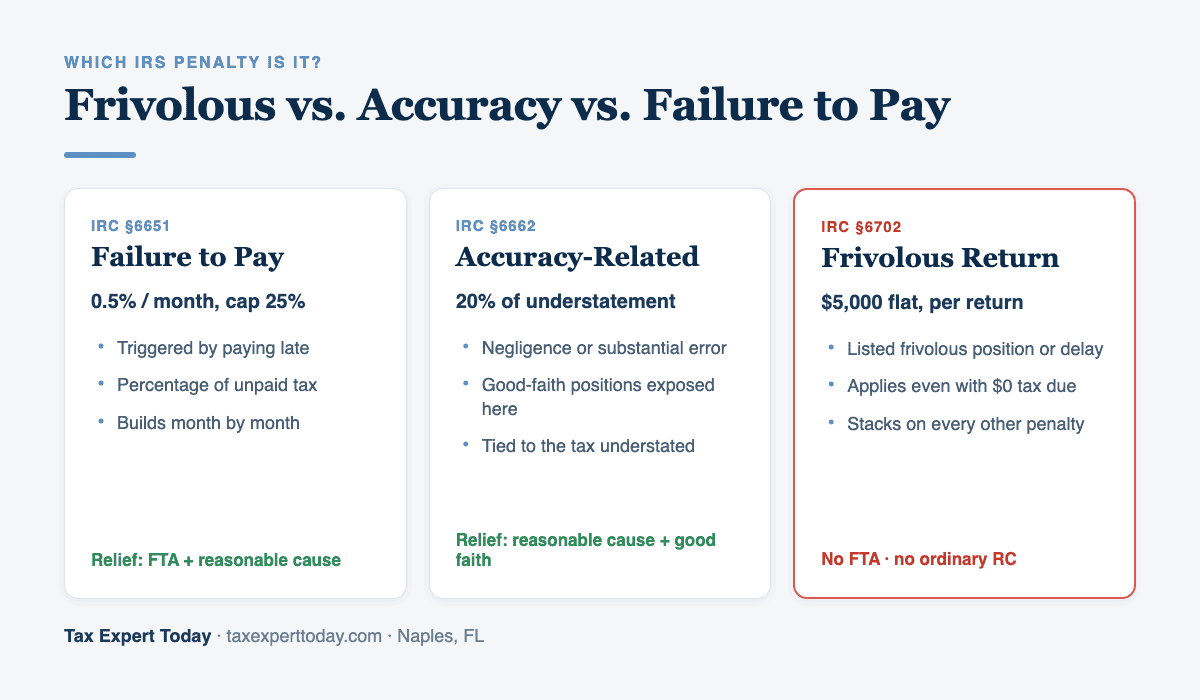

How Is the Frivolous Penalty Different From the Failure-to-File and Accuracy Penalties?

The frivolous penalty punishes the type of position taken, while the failure-to-file and accuracy penalties punish lateness or understatement regardless of motive. That distinction controls which relief is available. A taxpayer who simply filed or paid late is dealing with the percentage-based penalties under IRC Section 6651, both of which qualify for First-Time Abatement and reasonable cause. A taxpayer who understated tax through negligence or a substantial valuation error faces the 20% accuracy-related penalty under IRC Section 6662, which has a reasonable cause and good-faith defense. The frivolous penalty under Section 6702 sits apart: flat dollar amount, no FTA, no ordinary reasonable cause, and a basis tied to a published list of disallowed arguments. Knowing which penalty is actually in play is the first step, because applying the wrong relief request wastes the limited time the taxpayer has to respond.

Frivolous Return Penalty Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and businesses in Naples and across Southwest Florida respond to frivolous return notices, correct flagged or erroneously assessed returns, and get back into full compliance with the IRS. The firm does not promote or defend frivolous tax positions; the work is bringing a taxpayer’s filings into compliance and challenging a penalty on procedural grounds where the facts support it. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

How much is the frivolous tax return penalty?

The frivolous tax return penalty is a flat $5,000 per return or submission under IRC Section 6702. It does not increase or decrease with the amount of tax involved, and it can be assessed even when no tax is owed. On a jointly filed return signed by both spouses, the IRS can assess $5,000 against each spouse. The penalty is in addition to any failure to file, failure to pay, or accuracy-related penalty that also applies.

Can the frivolous return penalty be removed with First-Time Abatement?

No. First-Time Abatement applies only to the failure to file, failure to pay, and failure to deposit penalties, not to the frivolous return penalty under IRC Section 6702. Ordinary reasonable cause also does not apply, because the penalty turns on the position taken rather than on a missed deadline. The available paths are correcting the return within the Letter 3176C window, requesting a discretionary reduction under Section 6702(d), or paying 15% and filing a refund claim under Section 6703.

What should I do if I receive IRS Letter 3176C?

File a corrected, accurate return within the 30 days the letter allows. Letter 3176C is a warning that the IRS views a filed return as frivolous, and responding with a proper return reporting real income and figures generally prevents the $5,000 penalty from being assessed. Ignoring the letter lets the penalty attach and often precedes IRS collection action. If the return was flagged because of an honest error rather than a frivolous position, the correction response is where that is resolved.

Is the frivolous penalty the same as the accuracy-related penalty?

No. The accuracy-related penalty under IRC Section 6662 is 20% of an understatement caused by negligence or a substantial error, and it has a reasonable cause and good-faith defense. The frivolous penalty under IRC Section 6702 is a flat $5,000 tied to positions the IRS has formally identified as frivolous, with no ordinary reasonable cause defense. A good-faith but incorrect tax position is an accuracy-penalty issue, not a frivolous-penalty issue.

Where can I get help with a frivolous return penalty in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with frivolous return notices, correcting flagged returns, and returning to IRS compliance. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a Frivolous Return Penalty

The frivolous penalty rewards fast, correct action and punishes delay, which makes the response window the moment that matters. The judgment calls are whether the filing was actually frivolous or simply flagged in error, how to draft a corrected return that closes the issue, and whether the Section 6703 pay-and-claim route is worth pursuing given the facts. Standing on the original position is the one move that reliably makes things worse, because it invites the additional Tax Court penalty under IRC Section 6673. Tax Expert Today LLC represents individuals and businesses in IRS penalty and collection matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review a Letter 3176C or a frivolous penalty assessment and the response options that fit your facts. The 30-day correction window closes quickly, so the review is worth starting right away. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 3, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005