By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: The accuracy-related penalty under IRC Section 6662 adds 20 percent of the underpayment of tax that results from negligence, disregard of rules, or a substantial understatement of income tax. The rate rises to 40 percent for gross valuation misstatements and undisclosed foreign financial asset understatements. The penalty does not apply where the taxpayer shows reasonable cause and good faith under IRC Section 6664(c), or where the return position was adequately disclosed on Form 8275.

Published: May 28, 2026

An accuracy-related penalty notice often arrives after an audit or an automated adjustment such as a CP2000 notice, layered on top of the additional tax the IRS says is due. The penalty is not automatic, and it is not always correct. This 2026 guide explains the statutory framework under Internal Revenue Code Section 6662, the conduct that triggers the penalty, the rate that applies, and the defenses that remove it when the facts support relief.

What Is an Accuracy-Related Penalty?

An accuracy-related penalty is a civil penalty the IRS adds to an underpayment of tax when the underpayment results from specified taxpayer conduct on a filed return. The penalty is imposed under IRC Section 6662 and falls on the portion of the underpayment attributable to that conduct, not on the entire balance due. Because the penalty applies only where a return was filed, it is distinct from the failure-to-file and failure-to-pay penalties that attach to late filing and late payment.

Section 6662 consolidates several penalty grounds into one regime. The two grounds most individuals and small businesses encounter are negligence or disregard of rules and regulations under IRC Section 6662(b)(1), and substantial understatement of income tax under IRC Section 6662(b)(2). Valuation misstatement grounds apply in narrower circumstances involving property values and transfer pricing.

How Much Is the Accuracy-Related Penalty?

The standard accuracy-related penalty is 20 percent of the underpayment attributable to the prohibited conduct. The rate doubles to 40 percent for two categories. The chart below summarizes the rate structure as set by IRC Section 6662.

| Ground for penalty | Rate |

|---|---|

| Negligence or disregard of rules and regulations | 20% |

| Substantial understatement of income tax | 20% |

| Substantial valuation misstatement | 20% |

| Gross valuation misstatement | 40% |

| Undisclosed foreign financial asset understatement | 40% |

The penalty is calculated on tax, not on the income that was understated. On an underpayment of $20,000 attributable to negligence, the 20 percent penalty alone reaches $4,000, before any interest that accrues on both the tax and the penalty. Interest runs from the original due date of the return, so the longer an assessment sits unresolved, the larger the combined balance grows.

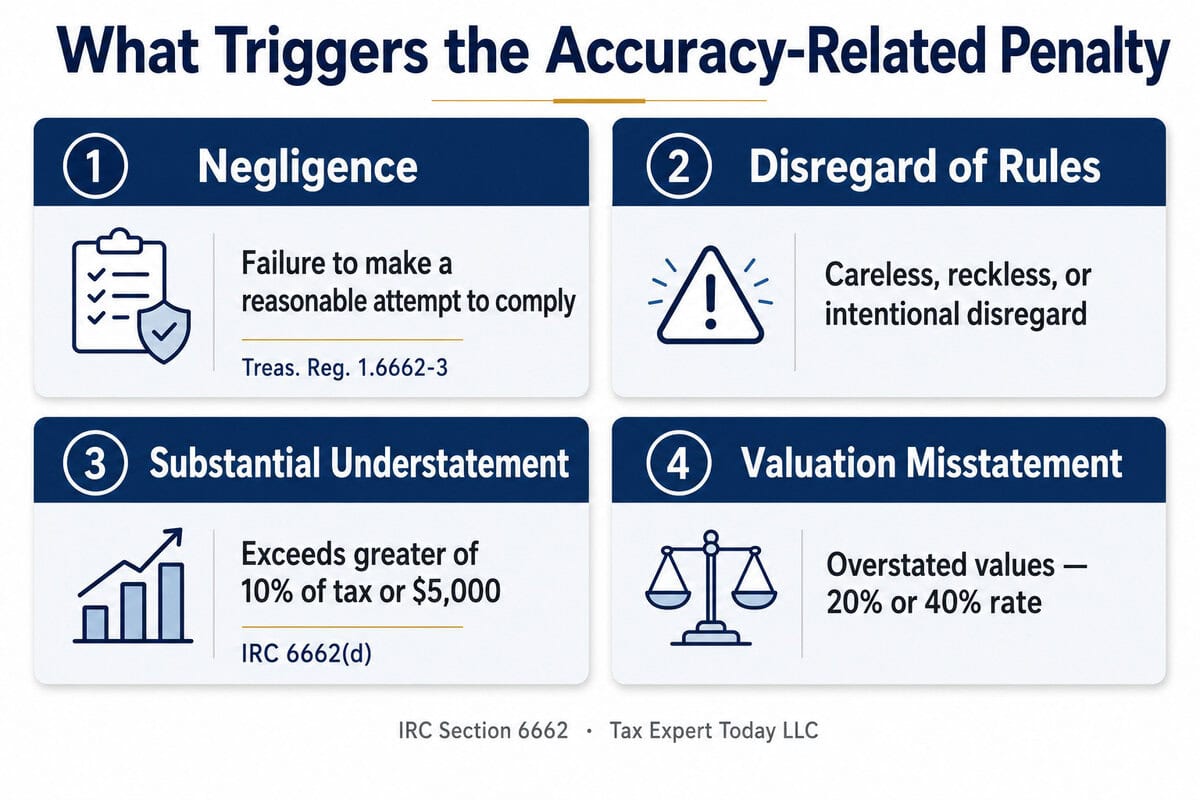

What Triggers an Accuracy-Related Penalty?

The IRS asserts the penalty when an examiner concludes the underpayment falls within one of the Section 6662 grounds. Each ground has a defined meaning in the regulations.

- Negligence

- Under Treasury Regulation 1.6662-3(b), negligence means any failure to make a reasonable attempt to comply with the tax laws, including the failure to keep adequate books and records or to substantiate items properly. A return position with a reasonable basis is not negligent.

- Disregard of rules or regulations

- Disregard covers any careless, reckless, or intentional disregard of the Internal Revenue Code, Treasury regulations, and published IRS rulings or notices. A position contrary to a rule that is adequately disclosed and has a reasonable basis is generally protected.

- Substantial understatement of income tax

- For an individual, an understatement is substantial when it exceeds the greater of 10 percent of the tax required to be shown on the return or $5,000, under IRC Section 6662(d). For most C corporations, the threshold is the lesser of 10 percent of the correct tax (or $10,000 if greater) or $10 million.

- Valuation misstatements

- A substantial valuation misstatement carries the 20 percent rate; a gross valuation misstatement carries 40 percent. These grounds reach overstated charitable deduction values, depreciation bases, and transfer pricing positions.

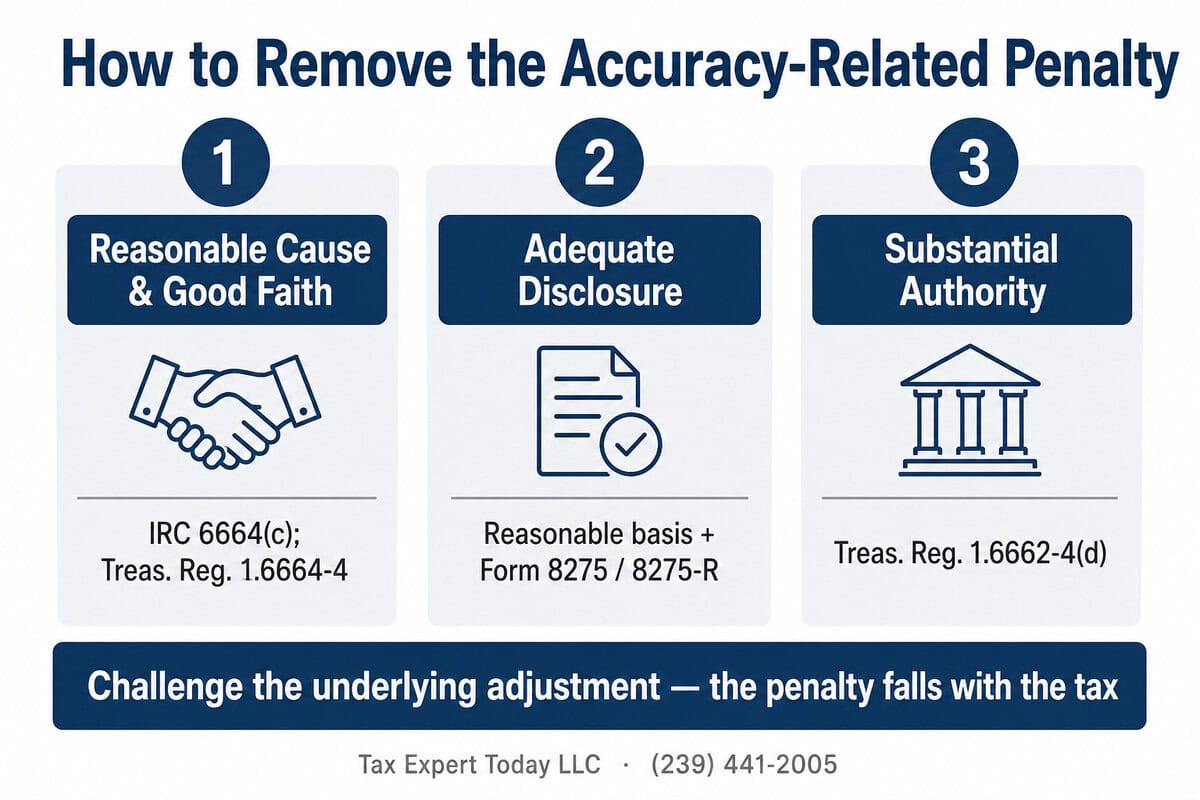

How Do You Remove an Accuracy-Related Penalty?

The accuracy-related penalty can be challenged, and in qualifying cases it is removed in full. When I review one of these notices, the first question is which Section 6662 ground the examiner actually asserted, because that determines which of the three defenses below applies.

- Reasonable cause and good faith. Under IRC Section 6664(c) and Treasury Regulation 1.6664-4, no accuracy-related penalty applies to any portion of an underpayment for which the taxpayer shows reasonable cause and that the taxpayer acted in good faith. The most important factor is the extent of the taxpayer’s effort to assess the correct tax liability. Honest reliance on the advice of a qualified tax professional who was given complete and accurate information can establish this defense, subject to the limits in the regulation.

- Adequate disclosure. The penalty for disregard of rules and for substantial understatement of non-tax-shelter items does not apply when the position has a reasonable basis and was adequately disclosed. Disclosure is made on Form 8275, or on Form 8275-R when the position is contrary to a regulation, as provided in Treasury Regulation 1.6662-3(c) and 1.6662-4(f).

- Substantial authority. For substantial understatement, the understatement is reduced by any portion supported by substantial authority under Treasury Regulation 1.6662-4(d). Substantial authority is an objective standard measured against statutes, regulations, cases, and published guidance.

A fourth path is often the most direct: challenge the underlying adjustment itself. When the additional tax is reduced or eliminated through audit reconsideration or appeal, the penalty calculated on that tax falls with it. The procedures that govern that challenge parallel the broader strategy described in our How to Get IRS Penalties Removed guide, and the documentation standards mirror those covered in our Reasonable Cause IRS Penalty guide.

Can the Accuracy-Related Penalty Stack With Other Penalties?

The accuracy-related penalty and the civil fraud penalty under IRC Section 6663 do not both apply to the same portion of an underpayment. Where the IRS asserts the 75 percent fraud penalty, the 20 percent accuracy penalty does not also attach to that portion. The accuracy-related penalty can, however, sit alongside failure-to-file and failure-to-pay penalties, which arise from late filing and late payment rather than from the content of the return. A complete review of an IRS notice identifies which penalties have been stacked and whether each is correctly applied.

Frequently Asked Questions

Can an accuracy-related penalty be removed?

Yes, in qualifying cases. The penalty does not apply to any portion of an underpayment for which the taxpayer establishes reasonable cause and good faith under IRC Section 6664(c). It also does not apply to positions that were adequately disclosed on Form 8275 and had a reasonable basis, or that were supported by substantial authority. Removing the underlying tax adjustment through appeal also removes the penalty calculated on it. Outcomes depend on the specific facts and documentation.

How much is the accuracy-related penalty?

The penalty is 20 percent of the underpayment attributable to negligence, disregard of rules, or a substantial understatement of income tax. It rises to 40 percent for gross valuation misstatements and for undisclosed foreign financial asset understatements, under IRC Section 6662.

What is a substantial understatement of income tax?

For an individual, an understatement of income tax is substantial when it exceeds the greater of 10 percent of the tax required to be shown on the return or $5,000, under IRC Section 6662(d). Different thresholds apply to corporations.

Does relying on a tax preparer protect me from the penalty?

Reliance on a qualified professional can support a reasonable cause defense when the taxpayer provided complete and accurate information and the reliance was reasonable and in good faith. Treasury Regulation 1.6664-4 governs the analysis, and reliance does not automatically defeat the penalty in every case.

How do I respond to an accuracy-related penalty notice?

Review the notice to confirm which Section 6662 ground the IRS asserted and how the penalty was calculated. Pull the account transcript, gather the records that support the return position, and respond within the deadline stated on the notice. Where the assessment followed an audit, the penalty can be contested through the same appeal that addresses the underlying tax.

When to Engage a Professional for an Accuracy-Related Penalty

The accuracy-related penalty turns on standards that are factual and document driven: whether a position had a reasonable basis, whether disclosure was adequate, and whether the taxpayer’s effort to determine the correct tax meets the reasonable cause standard. The mistake I see most often is treating the penalty as a fixed number. Because it is calculated on the underlying tax, reducing or eliminating that adjustment reduces the penalty with it. Each of these standards is contestable, and each requires matching the facts of the return to the controlling regulation. Tax Expert Today LLC represents individuals and businesses in penalty and audit matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review your notice and the available defenses. Interest accrues on both the tax and the penalty until the matter is resolved, so a timely response protects your position.

Published May 28, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005