By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Moving to Florida before selling a business can remove the state income tax on the gain, because Florida imposes no personal income tax and gain on the sale of stock or an ownership interest is generally sourced to the state where the seller is domiciled when the sale occurs. The savings are real only when the domicile change is genuine and complete before the deal becomes legally binding, and only for the part of the gain that is not tied to real property or operations still located in the old state. Timing, documentation, and the structure of the sale decide the result.

Published: July 2026

A business sale is often the largest single taxable event of an owner’s life, and the state where you are domiciled in the year of that sale can change the tax bill substantially. Florida collects no personal income tax, so owners in high-tax states such as New York, California, New Jersey, and Illinois frequently ask whether relocating first will keep the state out of the gain. The answer is that moving to Florida before selling a business can work, but it is not automatic. The outcome depends on when your domicile actually changes, what the buyer is buying, and where the underlying assets sit. This guide explains how the sourcing rules work, when the move must be complete, and how the installment method and the qualified small business stock rules interact with a Florida relocation. If California is the state you are leaving, our guide to the California exit tax covers the departure from the California side, including which gains remain taxable there after you move.

Should You Consider Moving to Florida Before Selling a Business?

Yes, considering a move to Florida before selling a business is worthwhile whenever the gain is large and the ownership interest is stock or an entity interest rather than in-state real property. Because Florida has no personal income tax and gain on intangible property generally follows the seller’s domicile, a completed and well documented move can remove the former state’s tax on that portion of the gain. The planning has to happen before the sale is committed, not after.

The strategy is strongest for the sale of C corporation stock, S corporation stock, or a limited liability company or partnership interest, because these are intangible assets. It is weakest, and sometimes ineffective, when the business owns real estate or operates through assets physically located in the old state, since states tax nonresidents on income sourced to property within their borders. Understanding which category your sale falls into is the first planning question.

The same sourcing logic applies at death rather than at sale. Real property and tangible property left behind generally stay inside the former state’s estate tax base even after Florida becomes your domicile. Our guide on Florida estate planning for new residents explains what your old state can still reach, and how the New York cliff works.

How Does Florida Residency Affect Tax on a Business Sale?

Florida residency affects the sale by changing which state may tax the gain on intangible property. When you sell corporate stock or an ownership interest, that gain is intangible income, and long standing sourcing principles assign intangible income to the state where the owner is domiciled at the time of the sale. A Florida domicile therefore places the gain in a state with no income tax, provided the gain is not independently sourced to the old state by a look-through or real property rule.

This is the same domicile concept that governs a state residency audit, and the two questions are decided on the same evidence. Your former state examines where your life is genuinely centered before it accepts that a sale belongs to Florida. For the full picture of how states test a move and what auditors weigh, see our guide on the Florida residency audit and the underlying steps in how to establish Florida residency.

If you plan to keep splitting the year between Florida and the old state rather than cutting ties completely, review our guide on dual state residency and the snowbird tax trap so a retained home and day count do not create a second residency.

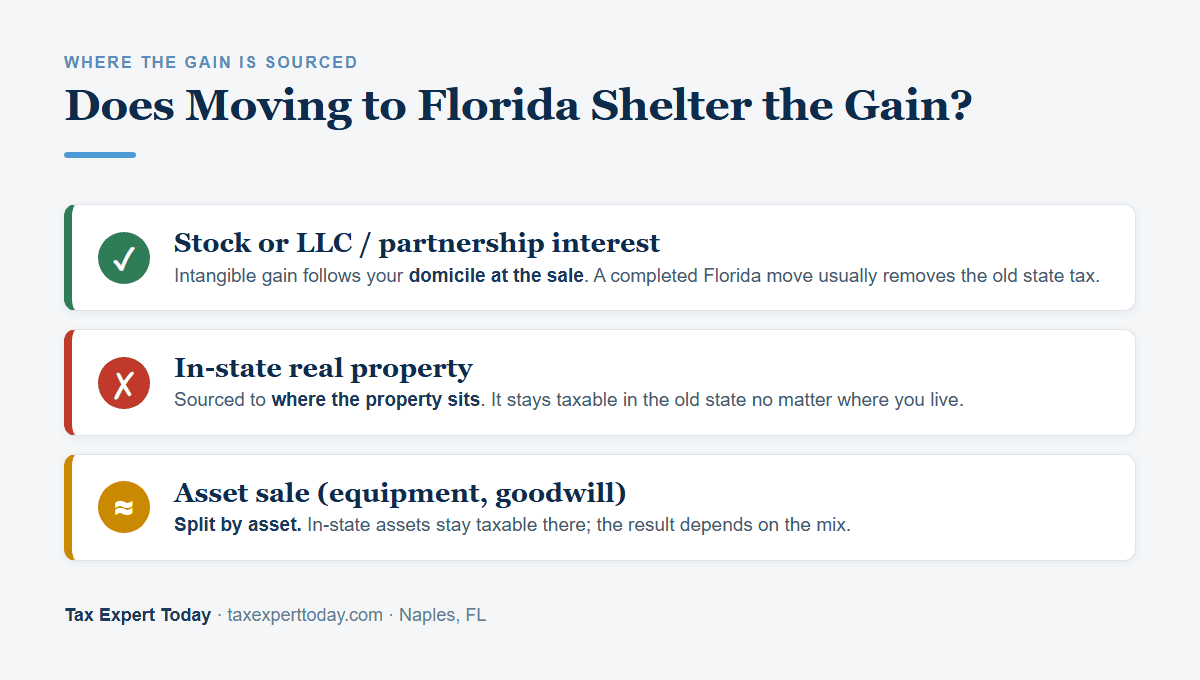

Which Sale Gains Can Your Old State Still Tax After You Move?

Your old state can still tax gain that is sourced to that state regardless of where you live, which primarily means gain on real property located there and gain tied to a business that operates there. Moving your domicile changes the treatment of intangible gain, but it does not convert in-state source income into Florida income. The distinction between an intangible interest and in-state assets is the core of the analysis.

The same sourcing logic reaches equity compensation. Restricted stock units and options earned while working in the old state stay partly taxable there after a move, allocated by workdays, as explained in our guide on Florida domicile for executives and RSU timing.

| What you sell | How it is generally sourced | Does moving to Florida help? |

|---|---|---|

| Corporate stock or an LLC or partnership interest (intangible) | To the seller’s state of domicile at the time of sale | Usually yes, if the move is complete and genuine |

| In-state real property, or an entity holding it | To the state where the real property is located | No, that gain stays taxable in the old state |

| Business assets in an asset sale (equipment, inventory, goodwill) | By asset, often to where the assets and operations are located | Partly, and it depends on the asset mix and state rules |

Two traps deserve special attention. First, several states apply a look-through rule to the sale of a partnership or limited liability company interest, treating part of the gain as in-state source income to the extent the entity owns property or does business in that state. Second, an asset sale splits the price across many assets under the federal allocation rules, and the in-state real estate and tangible property inside that allocation remain taxable where they sit. A stock sale of an entity that does not own in-state real property is the cleanest case for a Florida move.

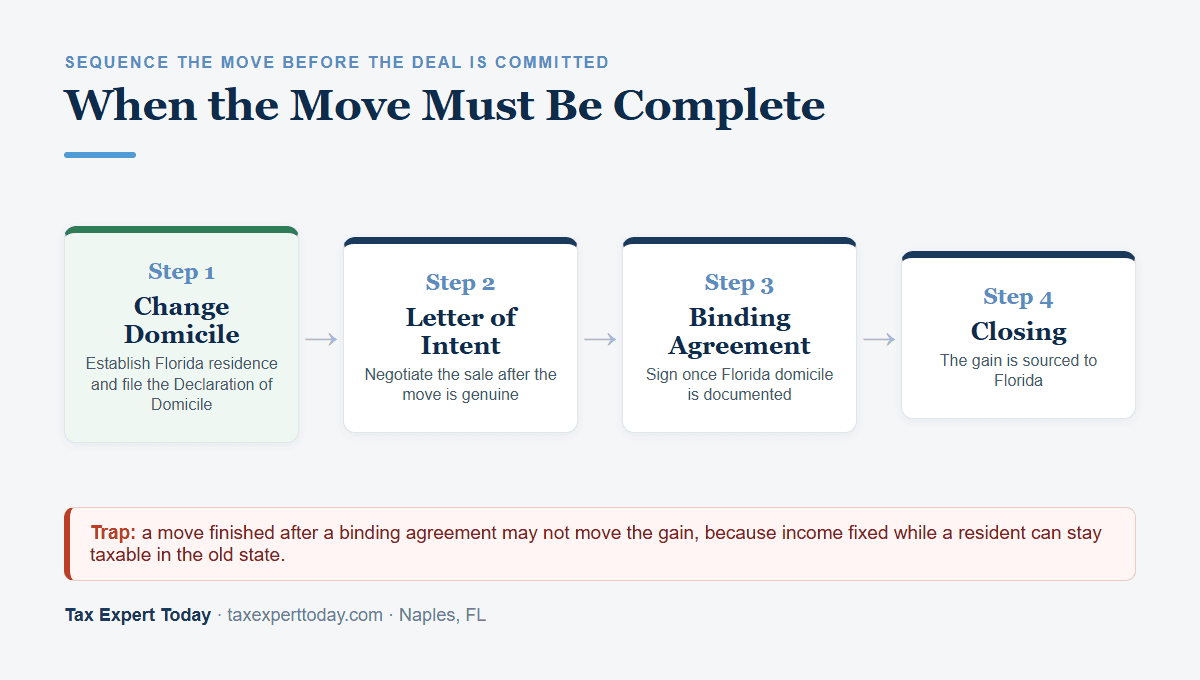

When Must the Move to Florida Be Complete to Count?

The move should be complete, meaning your domicile has genuinely changed to Florida, before the sale becomes legally binding, not merely before the closing date. States and the federal courts apply the assignment of income doctrine, which treats income as taxable to the person who owned the right to it when that right became fixed. If you sign a binding purchase agreement while still a resident of the old state, a later move may not move the gain.

Some states reinforce this with an accrual rule. Under New York Tax Law §639, a taxpayer who changes from resident to nonresident must accrue and report income items that accrued while a New York resident, which can pull a sale back into New York if the deal was fixed before the move. The practical rule is to change domicile before signing a binding letter of intent or purchase agreement, and to keep the negotiation, the move, and the signing in a clear and defensible order. A move finished after the deal is signed is the weakest position.

How Do Installment Sales and QSBS Change the Timing?

The installment method and the qualified small business stock rules can lower the overall tax and interact with the timing of a Florida move, but neither is a substitute for a genuine change of domicile. Each has federal mechanics that apply everywhere, plus state consequences that a Florida residence can improve.

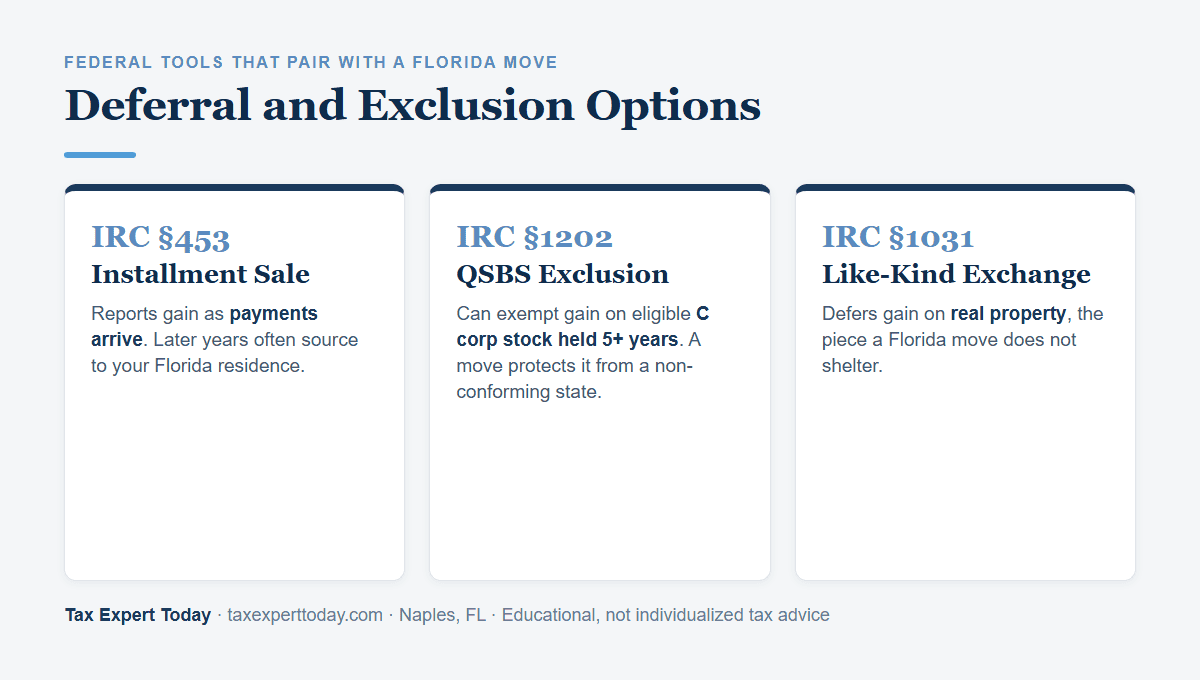

- Installment sale under IRC §453

- An installment sale reports the gain as payments arrive across future years rather than all at once. Gain on intangibles is generally sourced to your state of residence in the year each payment is received, so a Florida resident receiving later payments often keeps those years out of the old state. Some states apply accrual or claw-back rules to former residents, so the deferral is helpful but not assured, and the structure needs state-specific review.

- Qualified small business stock under IRC §1202

- The section 1202 exclusion can exempt a large share of gain on eligible C corporation stock held more than five years for federal purposes. States differ on whether they follow it, and some high-tax states do not conform and tax the gain in full. A Florida domicile removes the state layer entirely on the intangible gain, so it protects the benefit regardless of whether the old state would have honored the federal exclusion.

- Like-kind exchange under IRC §1031

- If the business owns real estate, a like-kind exchange can defer gain on that real property, which is now the only property type that qualifies. This matters because in-state real property is the category a Florida move does not shelter, so deferral is often the better tool for that piece.

Selling the old-state home usually rounds out the plan. The IRC §121 exclusion can exempt a substantial part of the gain on a primary residence you owned and used as your main home, and selling that home also strengthens the domicile record for Florida.

What Steps Protect a Pre-Sale Move to Florida?

Owners relocating a company to a no-income-tax state should also understand the Texas franchise tax that applies to most entities doing business there.

You protect a pre-sale move by completing the domicile change early, documenting it in real time, and sequencing the sale so the binding agreement follows the move. The same evidence that defends a residency audit also supports the position that a sale belongs to Florida.

- Establish Florida domicile before any binding letter of intent or purchase agreement, and file a Declaration of Domicile with your Florida county clerk.

- Complete the practical domicile steps, including a Florida driver license, voter and vehicle registration, homestead on the Naples home, and moving banking and advisors to Florida, as detailed in how to establish Florida residency.

- Keep a contemporaneous day log and limit days in the former state, and model the count with our Florida 183-day rule calculator so you do not trip the statutory residency test.

- Confirm what the buyer is acquiring, and separate any in-state real property so its treatment is planned rather than assumed.

- Review whether an installment sale, a section 1202 position, or a like-kind exchange fits the facts, and coordinate each with the residency timeline.

- Update your estate plan and trusts to Florida law, which supports both the domicile record and the longer term plan covered in our estate and trust planning service.

Moving to Florida Before a Business Sale: Help in Naples and Southwest Florida

Tax Expert Today LLC helps business owners in Naples and across Southwest Florida plan a move to Florida around a business sale or other large income event. In the high-income years leading up to a sale, some owners also use a cash balance plan to move a large, deductible amount into retirement savings. That work includes testing whether the gain is intangible or in-state source income, sequencing the domicile change ahead of a binding agreement, evaluating an installment or section 1202 structure, and building the residency file that supports the position if the former state asks questions. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, serving clients nationwide. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET. You can review the firm’s Naples tax planning and Florida tax services for related help.

Frequently Asked Questions

Do I owe state tax on my business sale if I move to Florida first?

It depends on what you sell and when your domicile actually changes. Gain on corporate stock or an ownership interest is generally sourced to your state of domicile at the time of sale, so a completed move to Florida can remove the old state’s tax on that intangible gain. Gain tied to in-state real property or in-state operations remains taxable in that state regardless of your move.

How soon before the sale do I need to establish Florida residency?

Your domicile should genuinely change before the sale becomes legally binding, not just before the closing. Because the assignment of income doctrine and rules such as New York Tax Law section 639 can tax income that became fixed while you were still a resident, a move completed after a binding purchase agreement is signed is difficult to defend. Establishing domicile before signing a binding letter of intent is the stronger position.

Does an installment sale keep my old state from taxing the gain?

Often, but not always. Under IRC section 453, an installment sale reports intangible gain as payments are received, and those years are generally sourced to where you reside when the payment arrives, which can favor a Florida resident. Some states apply accrual or claw-back rules to former residents, so the installment method needs a state-specific review rather than a blanket assumption.

Can my old state tax the sale of real estate my business owns?

Yes. Gain on real property is sourced to the state where the property is located, so a move to Florida does not shelter it. If the business owns real estate in the old state, that portion of the gain stays taxable there, and a like-kind exchange under IRC section 1031 is often the better tool for deferring it.

Where can I get help planning a Florida move before selling my business in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps business owners in Naples and across Southwest Florida time a move to Florida around a sale, source the gain correctly, and document the residency change. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and advises clients in residency and tax matters nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional Before a Business Sale

If you are planning to sell a business and considering a move to Florida, the planning is worth doing before the deal is committed rather than after the closing. The judgment calls are whether the gain is intangible or in-state source income, how to sequence the domicile change relative to a binding agreement, whether an installment or section 1202 structure fits, and how to document the move so it holds up if the former state reviews it. Those are the points where preparation changes the outcome, and where representation matters if a residency audit opens. Tax Expert Today LLC advises business owners on Florida relocation and represents taxpayers in residency and tax matters nationwide.

Call (239) 441-2005 or schedule a consultation to plan the timing of your move, source the gain correctly, and build a residency file that supports the sale. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 1, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005