By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: The dual state residency trap catches snowbirds who move to Florida but keep a home and a heavy day count in a high-tax state such as New York. Even with a genuine Florida domicile, the former state can still tax you as a statutory resident on all of your income when you keep a permanent home there and spend more than 183 days in the state during the year. Avoiding the trap means cutting both the days and the ties, not simply filing Florida paperwork.

Published: July 2026

Many snowbirds assume that buying a Florida home, getting a Florida driver license, and spending the winter in Naples is enough to leave a high-tax state behind. It often is not. A state such as New York or California can continue to tax a person who has genuinely changed domicile to Florida, because state residency is defined in more than one way and each state applies its own rules. When two states each treat you as a resident in the same year, you face dual state residency, and both states claim the right to tax your income. This guide explains how the trap forms, what the statutory residency and 183-day rules actually require, which states pursue it hardest, and how a Florida move should be structured so the former state cannot pull you back in.

What Is Dual State Residency?

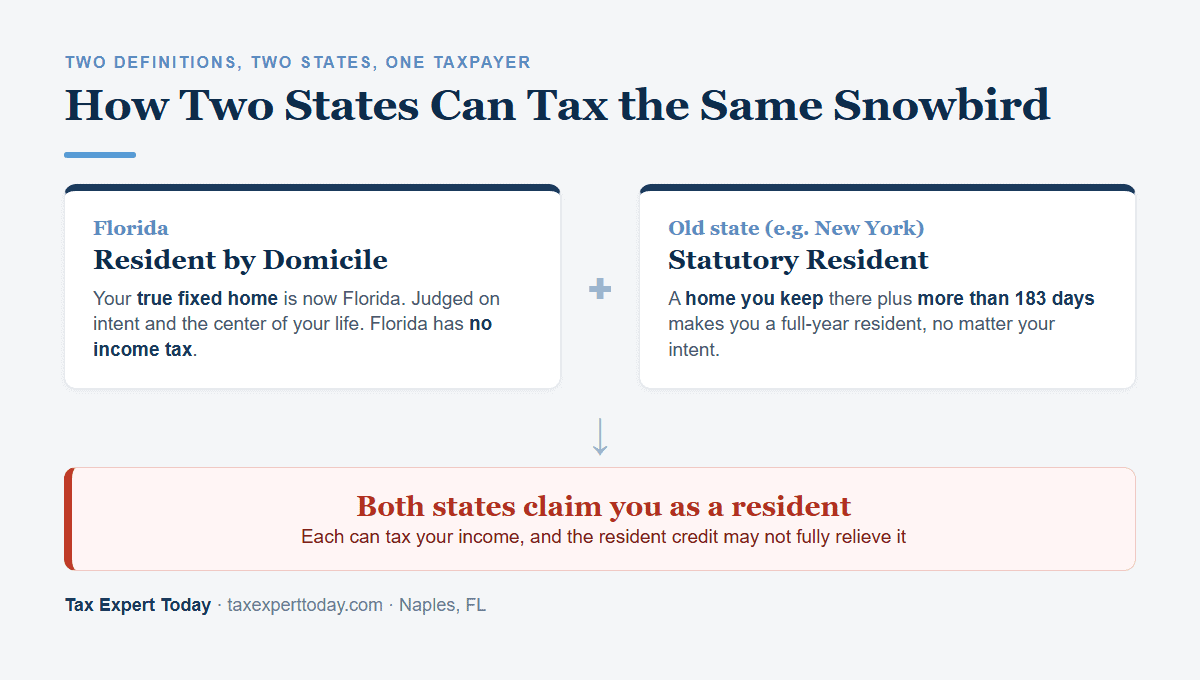

Dual state residency means two states each treat you as a resident for income tax purposes in the same year, so both claim the right to tax your income, including intangible income such as interest, dividends, and capital gains. It usually happens when one state considers you domiciled there while another counts you as a statutory resident based on a home you keep and the number of days you spend inside its borders.

The result can be a genuine double tax. States generally give a resident credit for tax paid to another state on income sourced there, but that credit often does not fully cover income taxed by both states purely on a residence basis, which is exactly the kind of income a snowbird tends to have. That gap is why dual residency is a trap rather than a simple paperwork problem.

How Can Two States Tax the Same Snowbird?

Two states can tax the same snowbird because states define residency in two different ways. A state taxes you as a resident if you are domiciled there, meaning it is your true fixed home, or if you are a statutory resident, meaning you keep a permanent place of abode there and spend more than 183 days in the state during the year. A move to Florida changes your domicile, but on its own it does nothing about the statutory residency test in the state you left.

This is the same domicile concept that governs a state residency audit, and it turns on where your life is genuinely centered. The former state examines that evidence before it accepts that you have left. For the underlying steps and the way auditors weigh a move, see our guides on how to establish Florida residency and the Florida residency audit.

What Is the Statutory Residency 183-Day Test?

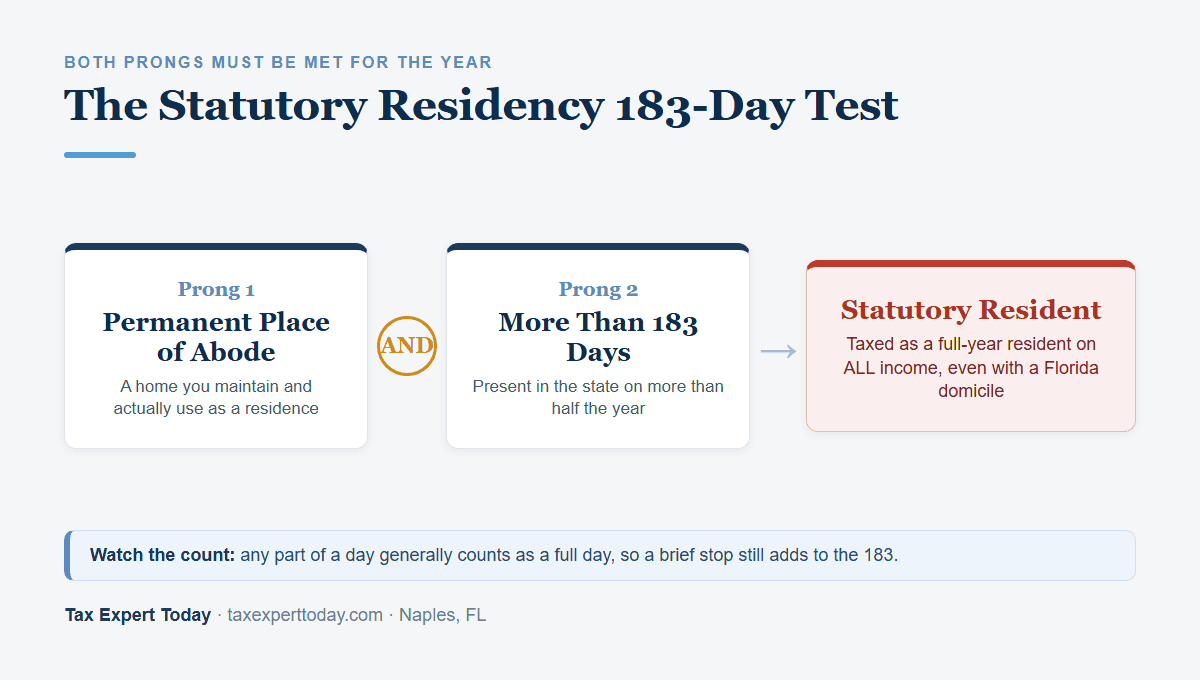

The statutory residency test makes you a full-year resident of a state, regardless of your domicile, when two conditions are both met for the year: you maintain a permanent place of abode in the state, and you are present there for more than 183 days. In New York, any part of a day generally counts as a full day, with narrow exceptions for travel through the state and for days spent receiving inpatient medical care.

Both prongs must be present, and the courts read them carefully. In Gaied v. New York State Tax Appeals Tribunal, New York’s highest court held that a dwelling is a permanent place of abode only if the taxpayer actually uses it as a residence, not merely because the taxpayer owns or pays for it. The statute itself appears in New York Tax Law §605(b), and the state explains the mechanics in its official income tax definitions.

| Prong of the statutory residency test | What it means | How the day or use is measured |

|---|---|---|

| Permanent place of abode | A dwelling you maintain and actually use as a residence, held for substantially all of the year | Ownership alone is not enough; the home must be usable and used, as Gaied requires |

| More than 183 days in the state | Physical presence in the state on more than half the year | Any part of a day generally counts as a full day, so a brief stop can add to the total |

The day count is the piece snowbirds control most directly, and it is also the piece auditors examine most closely, using cell phone records, toll and travel data, and credit card activity. A contemporaneous day log is the single most useful record you can keep, and our Florida 183-day rule calculator helps you model the count before the year is over.

Domicile vs. Statutory Residency: What Is the Difference?

Domicile is your one true permanent home, the place you intend to return to, and you keep it until you clearly establish a new one. Statutory residency ignores intent and looks only at a physical home plus a day count. You can change your domicile to Florida and still be a statutory resident of the state you left, which is the heart of the dual-residency trap.

- Domicile

- Your fixed and permanent home, judged on intent and the center of your life, including where your family, primary home, business ties, and community connections sit. You have exactly one domicile, and it does not change until a new one is established.

- Statutory residency

- A residency status based purely on mechanics, triggered when you keep a permanent place of abode in the state and spend more than 183 days there. Intent does not matter, and it can apply even to a person who is clearly domiciled elsewhere.

- Why both matter to a snowbird

- A clean Florida move wins the domicile question, but the former state can still reach you through statutory residency if you keep the old home and the days. Escaping the tax means clearing both tests, not just one.

Which States Pursue Snowbirds Most Aggressively?

New York and California pursue departing residents most aggressively, and both run active residency audit programs. New York applies the permanent place of abode plus 183-day statutory residency test and examines day counts closely. California uses a facts and circumstances closest connections test rather than a fixed day count, so a vacation home and strong California ties can make you a resident even without 183 days of presence.

| State | How it can claim you | What tends to trigger a look |

|---|---|---|

| New York | Domicile or statutory residency, under Tax Law §605(b) | Keeping a New York home plus a large income year or a sale of a business |

| California | Closest connections test; presumption of residency after nine months in the state | A retained California home, family, or business ties after a claimed move |

| New Jersey, Illinois, and similar high-tax states | Domicile or a statutory residency test modeled on the 183-day rule | A maintained residence and a day count that stays above the threshold |

The California Franchise Tax Board explains that residency there turns on the closest connections to a state, which is a softer and in some ways harder line to clear than a day count. The common thread across every aggressive state is that a retained home plus continued presence keeps the door open. Our guide to the California exit tax explains what does and does not follow a departing Californian.

Executives carry an added layer, because restricted stock units, options, and deferred pay earned in the old state can stay taxable there even after a clean move. Our guide on Florida domicile for executives and RSU timing explains how that equity is sourced.

How Do You Avoid the Dual-Residency Trap When Moving to Florida?

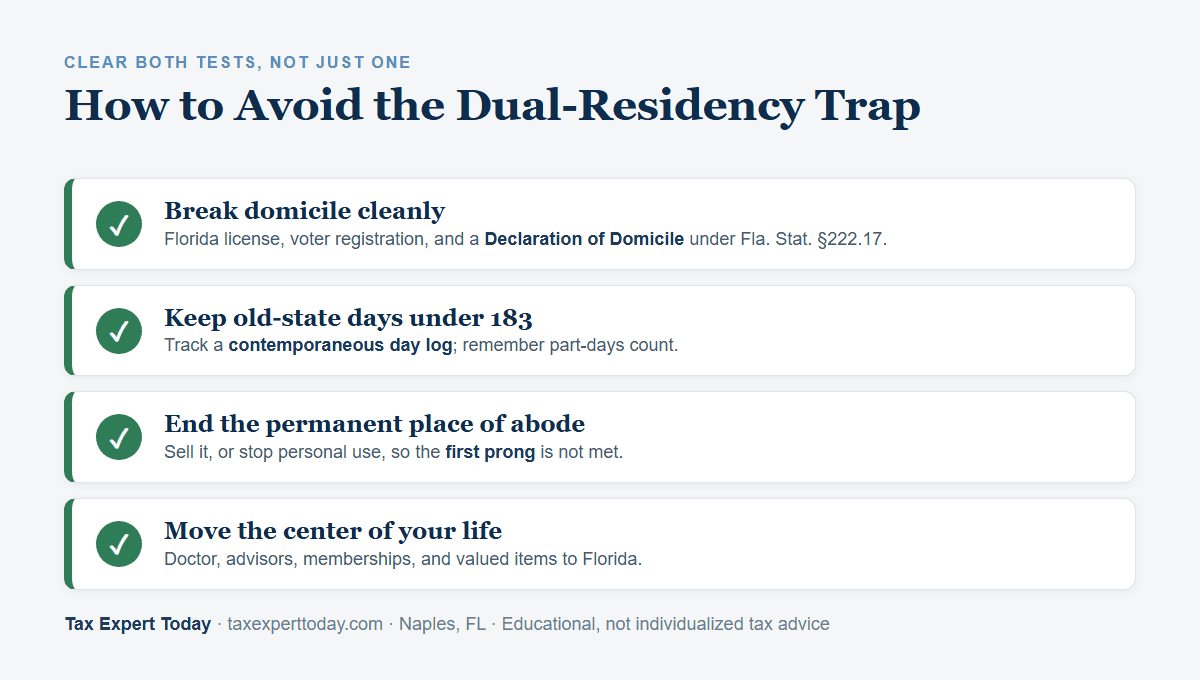

You avoid the trap by breaking domicile cleanly and cutting the day count in the old state, not just by filing Florida paperwork. That means reducing time in the former state below the statutory threshold, giving up or limiting the permanent home there, moving the center of your life to Florida, and keeping contemporaneous records that prove both the domicile change and the day count.

- Establish Florida domicile in a documented way, including a Florida driver license, voter registration, and a Declaration of Domicile, following the full checklist in how to establish Florida residency.

- Keep your presence in the former state under the 183-day line, and keep a contemporaneous day log, modeling the count with our Florida 183-day rule calculator.

- Reduce the permanent place of abode in the old state by selling it, converting it to a rental you do not use, or otherwise ending your personal use, since a home you keep and use is the first prong of statutory residency.

- Move the center of your life to Florida, including your primary physician, financial advisors, place of worship, club memberships, and the items you value most, so the domicile record is consistent.

- Time any large income event, such as a business sale or a stock sale, around the move, as explained in moving to Florida before selling a business.

- Update your estate plan and trusts to Florida law, which both supports the domicile record and advances the longer term plan covered in our estate and trust planning service.

Does Florida Have a Residency Day-Count Rule?

No. Florida imposes no personal income tax, so it has no resident or statutory-resident income tax test and no 183-day counting rule of its own. What Florida offers instead is documentation that helps prove domicile, including the Declaration of Domicile under Florida Statutes §222.17 and the permanent residency factors used for homestead under Florida Statutes §196.015. The day count that matters is the one kept by the state you left, so the planning always points back to the former state’s rules.

Snowbird and Dual-Residency Help in Naples and Southwest Florida

Tax Expert Today LLC helps snowbirds and part-year residents in Naples and across Southwest Florida structure a Florida move so the former state cannot pull them back in. That work includes testing both the domicile and statutory residency questions, building a day-count log that survives review, reducing ties and abode in the old state, and coordinating the timing of a large income event with the move. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, serving clients nationwide. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET. You can review the firm’s Naples tax planning and Florida tax services for related help.

Frequently Asked Questions

Can two states really tax the same income?

Yes. When two states each treat you as a resident, both can tax your income on a residence basis, including intangible income such as interest, dividends, and capital gains. A resident credit usually offsets tax paid to another state on income sourced there, but it often does not fully relieve income that both states tax purely because they each claim you as a resident, which is why dual residency can produce a real double tax.

How many days can I spend in New York without becoming a resident?

If you keep a permanent place of abode in New York, spending more than 183 days there generally makes you a statutory resident for the entire year, even if you are domiciled in Florida. Any part of a day usually counts as a full day, so brief visits add up. Staying at or below 183 days and keeping a contemporaneous log are essential when you retain a New York home.

Do I still owe New York tax if I move to Florida in the middle of the year?

In the year of the move you generally file as a part-year resident of New York, taxed as a resident for the portion of the year before your domicile changed. The statutory residency test can still apply for the full year if you kept a permanent place of abode and exceeded the day threshold, so a mid-year move needs careful day counting and documentation rather than an assumption.

Does California use the 183-day rule?

No. California does not rely on a fixed 183-day count. It applies a facts and circumstances closest connections test and presumes residency for anyone present in the state more than nine months in a year. A retained California home and strong California ties can make you a resident even without 183 days of presence, so a California exit turns on cutting ties rather than counting days.

Where can I get help with a dual-residency or snowbird tax question in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps snowbirds and part-year residents in Naples and across Southwest Florida clear both the domicile and statutory residency tests, document the day count, and reduce ties to the former state. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and advises clients in residency and tax matters nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional on a Dual-Residency Question

If you split the year between Florida and a high-tax state, the planning is worth doing before the year closes rather than after a notice arrives. The judgment calls are whether you have cleared both the domicile and statutory residency tests, how to keep the day count defensible, whether to reduce or give up the home in the old state, and how to time a large income event around the move. Those are the points where preparation changes the outcome, and where representation matters if a residency audit opens. Tax Expert Today LLC advises snowbirds and part-year residents on Florida relocation and represents taxpayers in residency and tax matters nationwide.

Call (239) 441-2005 or schedule a consultation to test both residency questions, build a day-count record, and structure your move so only one state can tax you. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 6, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005