By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: There is no California exit tax. The wealth tax bills that would have taxed former residents for up to ten years after departure, AB 2088 in 2020 and AB 259 in 2024, both died without becoming law. What actually follows you out of California is narrower and much older: residency based taxation until you genuinely change domicile, plus California source income that remains taxable no matter where you later live.

Published: July 2026

What Is the California Exit Tax?

The California exit tax is a tax that does not exist. No provision of California law imposes a charge for the act of leaving the state, and no statute taxes a former resident on wealth accumulated while living there. The phrase entered circulation through proposed legislation that was never enacted, and it has outlived the bills that created it by several years.

The confusion is understandable, because two separate ideas get compressed into one phrase. The first idea is a true exit tax, meaning a levy triggered by departure itself. California has never had one. The second idea is that California continues to tax certain income after you leave. That one is real, but it is not an exit tax. It is ordinary source based taxation, and it operates the same way for a person who has never set foot in California as it does for someone who moved away last year.

Did California Ever Pass an Exit Tax?

No. Two wealth tax bills proposed something resembling an exit tax, and both failed. Neither reached the governor. Neither was ever enacted in any form. Because the proposals were widely covered while they were pending, and far less widely covered when they died, the rumor has substantially outlasted the legislation.

AB 2088, introduced in February 2020, proposed an annual tax of 0.4 percent on worldwide net worth above $30 million. Its notable feature was a tail provision: a person who had been subject to the tax would continue to owe a declining fraction of it for ten years after leaving, reduced by one tenth each year. That tail is the specific origin of the ten year exit tax story. The bill died in committee in November 2020 without a floor vote.

AB 259, introduced in 2023 alongside proposed constitutional amendment ACA 3, revived the concept at a $50 million threshold. It failed on February 1, 2024. A wealth tax of the type both bills contemplated would require a constitutional amendment, because the California Constitution caps the rate on personal property, which is why ACA 3 accompanied AB 259 in the first place.

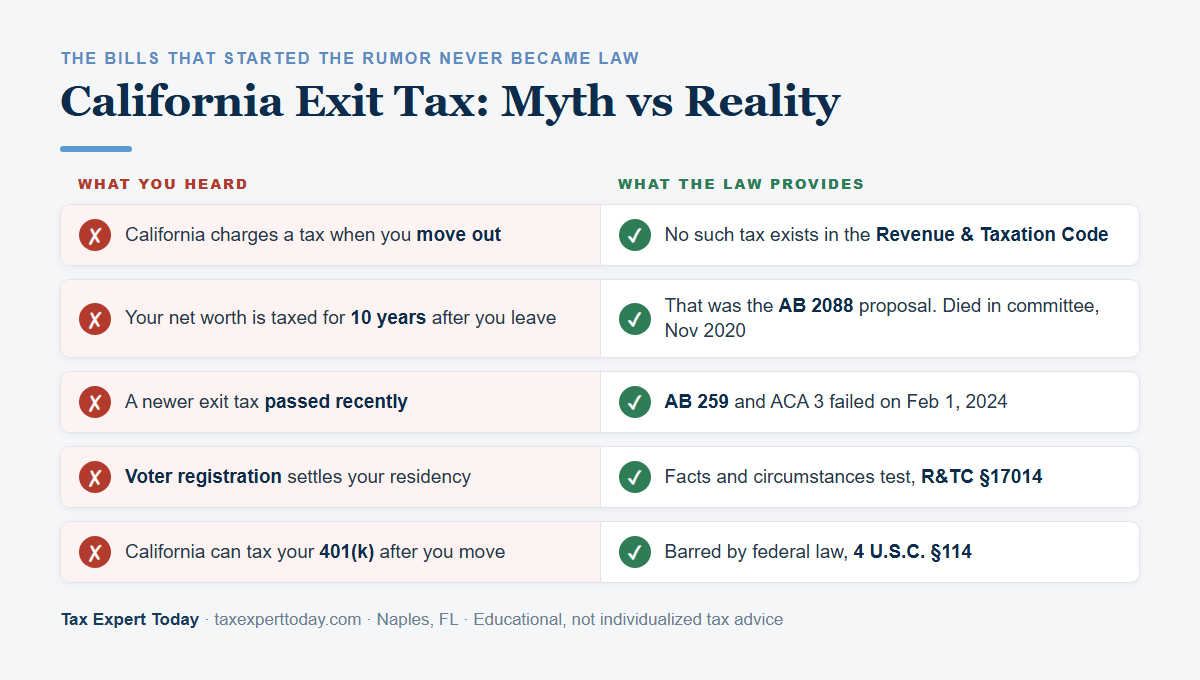

| What you may have heard | What the law actually provides |

|---|---|

| California charges a tax when you move out | No such tax exists in the Revenue and Taxation Code |

| California taxes your net worth for ten years after you leave | That was the AB 2088 proposal. It died in committee in November 2020 |

| A newer version of the exit tax passed recently | AB 259 and ACA 3 failed on February 1, 2024 |

| Changing your voter registration settles residency | Residency is a facts and circumstances test under R&TC §17014. No single document controls |

| Moving before a sale always removes California tax | Only if the sale occurs after residency actually changes. Timing governs, not intent |

| California can tax your 401(k) after you move | 4 U.S.C. §114 prohibits states from taxing qualified retirement income of nonresidents |

What Actually Follows You Out of California?

Two things follow a departing Californian, and neither is an exit tax. The first is residency itself, which persists until you genuinely abandon California domicile and establish a new one. The second is California source income, which stays taxable in California regardless of where you live when you receive it. Understanding which category a given dollar falls into is the whole exercise.

California taxes residents on all income from every source, and taxes nonresidents only on income sourced to California. That single sentence explains most outcomes. The planning question is therefore never how do I avoid the California exit tax, because there is no such thing. The question is when did residency actually change, and which of my income items carry a California source regardless.

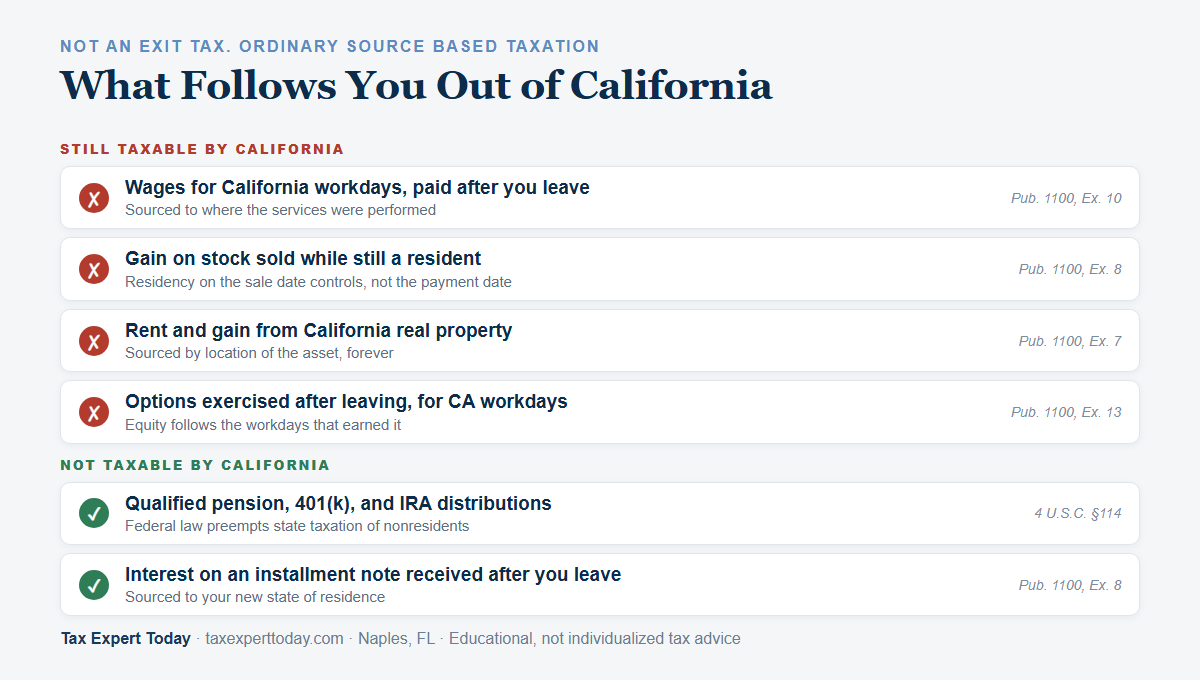

| Income item | Taxable by California after you move? | Authority |

|---|---|---|

| Wages for services performed in California, paid after you leave | Yes, sourced to where services were performed | FTB Pub. 1100, Example 10 |

| Gain on stock sold while still a California resident, paid in installments after you leave | Yes, residency at the time of sale controls | FTB Pub. 1100, Example 8 |

| Gain on stock sold after residency changed | Generally no, sourced to your new state | R&TC §17952 |

| Rent or gain from California real property | Yes, always, regardless of residency | FTB Pub. 1100, Example 7 |

| Nonstatutory stock options for California workdays, exercised after you leave | Yes, compensation follows the workdays | FTB Pub. 1100, Example 13 |

| Qualified pension, 401(k), and IRA distributions | No, federal law preempts state taxation | 4 U.S.C. §114 |

| Interest on an installment note received after you leave | No, sourced to your state of residence | FTB Pub. 1100, Examples 6 to 8 |

How Does California Decide Whether You Are Still a Resident?

California applies a facts and circumstances test, not a checklist. Under R&TC §17014, a resident is every individual in the state for other than a temporary or transitory purpose, and every individual domiciled in the state who is outside it for a temporary or transitory purpose. Domicile and residence are separate concepts in California, and they do not always align.

FTB Publication 1031 defines domicile as the place where you voluntarily establish yourself and your family, with the present intention of making it your true, fixed, permanent home, and the place to which you intend to return whenever you are absent. Changing domicile requires all three of the following: abandonment of the prior domicile, physically moving to and residing in the new locality, and intent to remain there permanently or indefinitely as demonstrated by your actions. You may hold only one domicile at a time, and you keep the old one until you acquire a new one.

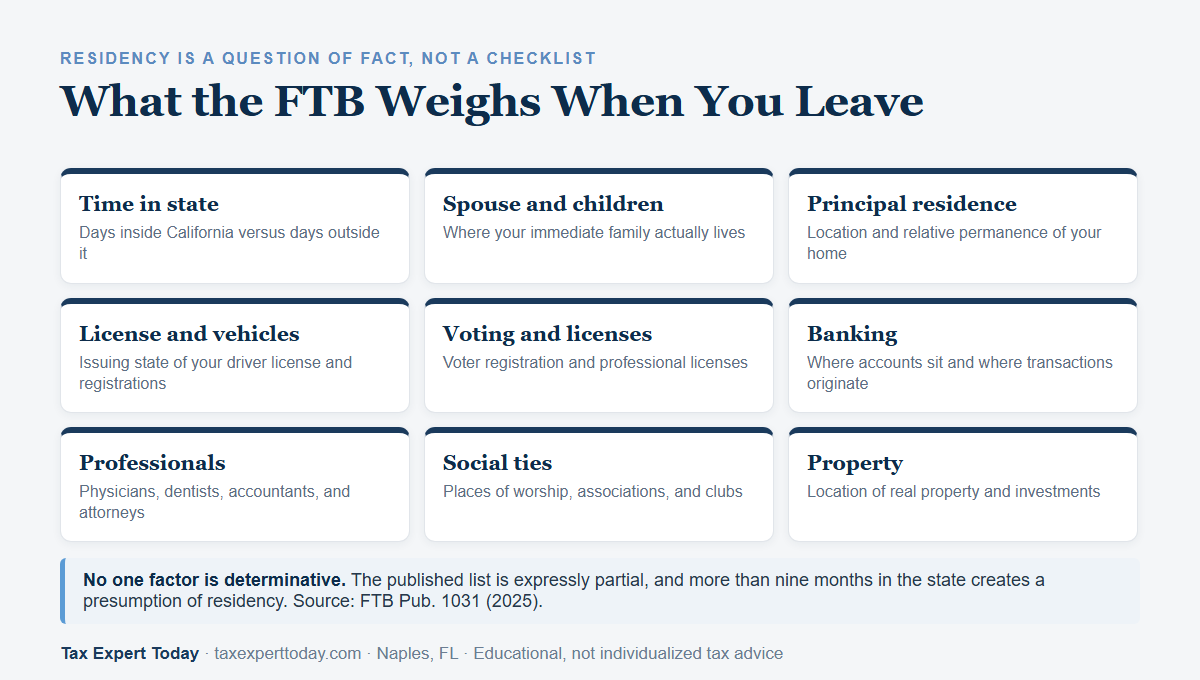

Publication 1031 lists the connections the FTB weighs. No single factor is determinative, and the published list is expressly partial:

- Time spent in California versus time spent outside it

- Location of your spouse or registered domestic partner and your children

- Location of your principal residence

- State that issued your driver license, and where your vehicles are registered

- State where you maintain professional licenses and where you are registered to vote

- Location of your banks, and the origination point of your financial transactions

- Location of your physicians, dentists, accountants, and attorneys

- Location of social ties, including places of worship, professional associations, and clubs

- Location of your real property and investments

- Permanence of any work assignments in California

Two specific rules deserve attention. First, Publication 1031 states that you are presumed to be a California resident for any taxable year in which you spend more than nine months in the state. Second, a safe harbor exists for individuals leaving California under an employment related contract for an uninterrupted period of at least 546 consecutive days. That safe harbor does not apply if intangible income exceeds $200,000 in any taxable year the contract is in effect, or if the principal purpose of the absence is avoiding personal income tax. Return visits totaling 45 days or fewer per year are treated as temporary. The safe harbor is narrow, and it does not cover a retiree or a business owner who simply relocates.

If you are moving to Florida specifically, the mechanics of building the other side of the record are covered in our guides on how to establish Florida residency and the dual state residency trap. Florida permits a formal Declaration of Domicile under Fla. Stat. §222.17, which is useful evidence, though it is one factor among many rather than a switch that ends California residency.

What Happens to a Business Sale or an Installment Note?

Timing controls. If you sell while you are still a California resident, California taxes the gain, and it does not matter that the money arrives after you have moved. If residency has genuinely changed before the sale occurs, gain on intangible property is generally sourced to your new state under R&TC §17952, which provides that a nonresident is not taxed on income from stocks, bonds, or notes unless that property has acquired a business situs in California.

FTB Publication 1100 addresses the California to Florida fact pattern directly. In its Example 8, a California resident sells stock in an installment sale in September, becomes a Florida resident on February 1 of the following year, and receives installment proceeds on May 1. The determination is that the capital gain remains taxable by California, because the taxpayer was a California resident when the stock was sold. Only the interest component escapes, because interest is sourced to the recipient state of residence at the time of receipt.

The mirror image also holds. Under Example 6, a former resident who sold real property located outside California while still a resident is not taxed by California on installment proceeds received afterward. Under Example 7, real property located inside California remains California taxable on the gain no matter where the seller has moved, because California sources real property income by location.

The practical consequence for owners contemplating both a move and a sale is that the sequence, and the defensibility of the residency change on the date of sale, carry the entire result. This is the California side of the analysis. The Florida side, including the timing considerations before a transaction, is covered in our guide on moving to Florida before selling a business.

Do RSUs and Stock Options Still Get Taxed by California?

Yes, to the extent the equity compensates California workdays. California taxes wage income from employee stock options on a source basis, and Publication 1100 states this applies whether you were always a nonresident or were formerly a California resident. Equity compensation is treated as payment for the services that earned it, so the location where you performed those services governs.

Publication 1100 Example 13 is instructive. A taxpayer is granted nonstatutory stock options while a California resident, performs all services in California until leaving the company and moving to Texas, and exercises the options a month after the move. The resulting income is taxable by California, because it is compensation for services having a California source. Moving first does not change where the work was performed.

Restricted stock units follow comparable workday allocation logic, and the FTB addresses equity compensation in detail in FTB Publication 1004. Executives holding unvested equity when they relocate frequently find that a meaningful share of a future vest remains California taxable for years afterward. The Florida side of this planning question is discussed in our guide on Florida domicile for executives.

Can California Tax Your Retirement Income After You Move?

No, and this is where federal law provides a genuine shield rather than a planning technique. 4 U.S.C. §114 prohibits any state from imposing income tax on the retirement income of an individual who is not a resident or domiciliary of that state. Publication 1100 reflects this, stating plainly that California does not tax the IRA distributions or the qualified pension, profit sharing, and stock bonus plans of a nonresident.

The protection covers qualified plans, individual retirement accounts, and certain nonqualified deferred compensation paid in substantially equal periodic payments over life expectancy or over a period of at least ten years. It does not convert California source wages into exempt income, and it does not protect deferred compensation structured outside those parameters. A departing executive with a nonqualified plan should confirm the payout schedule against the statute before assuming the shield applies.

What If You Keep California Real Estate?

California real property remains California taxable indefinitely. Rental income is California source while you own it, and gain on sale is California source when you sell it, regardless of how many years you have lived elsewhere. Residency planning does nothing for real estate, because California sources this income by the location of the asset rather than the location of the owner.

Sales of California real property are also subject to withholding. Form 593 provides for withholding at 3 1/3 percent (.0333) of the total sales price, or at an alternative withholding calculation elected by the seller. Withholding is a prepayment rather than a final tax, so the actual liability is settled on the return, but sellers who do not plan for it are often surprised by the amount held back at closing.

How Much Is Actually at Stake?

The arithmetic explains why the corridor exists. California imposes a top marginal rate of 12.3 percent under R&TC §17041, plus an additional 1 percent Mental Health Services Tax on taxable income above $1 million, for a combined 13.3 percent. Wage earners face more, because State Disability Insurance is withheld at 1.3 percent for 2026 and, since January 1, 2024, applies to all wages with no cap. Florida imposes no personal income tax at all.

Consider a hypothetical: a business owner with $3 million of taxable gain on the sale of company stock. Sold as a California resident, the gain carries roughly $399,000 of California tax at 13.3 percent. Sold after a defensible change of residency to Florida, and assuming the stock has not acquired a California business situs under R&TC §17952, the California tax on that intangible gain is zero. The same transaction, separated by the residency date, produces materially different results. That gap is why sequencing and documentation matter far more than the rumored California exit tax ever did, and it is also why the FTB scrutinizes departures in high value years. Outcomes depend entirely on individual facts.

California Exit Tax Help in Naples & Southwest Florida

Tax Expert Today LLC advises individuals and business owners on state residency and tax matters nationwide, including California departures and Florida arrivals. Our team includes tax advisors, enrolled agents, CPAs, and attorneys, which matters on a corridor question because the California side and the Florida side of a move are analyzed under different bodies of law and often in the same tax year. We work with clients relocating from California to Florida on residency documentation, transaction sequencing, part-year return preparation, and Franchise Tax Board correspondence.

Our office is located at 11983 Tamiami Trail N, Naples, FL 34110. You may reach us at (239) 441-2005, Monday through Friday, 10am to 5pm ET. We serve clients in all 50 states, with a concentration in Florida, California, Texas, and Georgia. Related reading includes our California tax services page, our Naples tax planning overview, and our Florida residency audit guide.

Frequently Asked Questions

Does California have an exit tax in 2026?

No. California has no exit tax and has never enacted one. AB 2088 in 2020 and AB 259 in 2024 proposed wealth taxes with provisions that would have reached former residents, and both died in committee. What persists after a move is residency based taxation until domicile genuinely changes, and California source income, which remains taxable regardless of where you live.

How long does California have to audit my residency after I leave?

California generally has four years from the filing date to assess additional tax on a filed return, and there is no statute of limitations on unfiled returns. Departure years are commonly examined because they combine a residency change with a high income event. Contemporaneous records of your whereabouts and connections carry more weight than reconstructions prepared later.

Can California tax my income if I move to Florida mid-year?

Yes, for the California portion. In the year of a move you generally file Form 540NR as a part-year resident, reporting all income earned while a California resident plus any California source income earned after the move. California computes the tax using an effective rate based on total income, so income earned after departure can still influence the rate applied to the California portion.

Will a Florida Declaration of Domicile end my California residency?

Not by itself. A Declaration of Domicile under Fla. Stat. §222.17 is useful evidence of intent, but California applies a facts and circumstances test in which no single document is determinative. The FTB weighs where your home, family, licenses, physicians, bank relationships, and social ties are actually located, and it compares your conduct against your stated intent.

Where can I get help with a California to Florida move in Naples, FL?

Tax Expert Today LLC, at 11983 Tamiami Trail N, Naples, FL 34110, advises clients on California departures and Florida residency. Our team of tax advisors, enrolled agents, CPAs, and attorneys handles residency documentation, transaction timing, part-year returns, and Franchise Tax Board correspondence. Call (239) 441-2005, Monday through Friday, 10am to 5pm ET. We serve clients in all 50 states.

When to Engage a Professional

Residency changes are decided on facts, and the facts are built long before anyone asks to see them. Professional guidance is generally worthwhile where a move coincides with a liquidity event, where equity compensation vests across the departure date, where California real property or a California operating business remains behind, or where the departure year involves income substantial enough that the Franchise Tax Board is likely to examine it.

Whether any particular strategy applies depends on your specific facts, and the analysis frequently spans two states in the same tax year. If you are planning a California departure, or if you have already moved and want the record reviewed before it is tested, our team advises on residency and tax matters nationwide. Call (239) 441-2005 or visit our California tax services page. Engagements are scoped and quoted after a consultation.

This article is educational and does not constitute tax advice for any particular taxpayer. California residency outcomes depend on individual facts and circumstances, and applicable law may change.

Published July 15, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005