By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Establishing Florida domicile for executives removes Florida income tax on future pay, but it does not erase the former state’s tax on equity compensation already earned there. States source restricted stock units and stock options by the share of workdays performed inside the state during the vesting period, so a California or New York executive who moves to Florida still owes the old state tax on the portion tied to in-state work. Nonqualified deferred compensation can escape the former state only when it is paid over at least ten years or over life expectancy.

Published: July 2026

Executives who move to Florida for its lack of a personal income tax often carry a portfolio of restricted stock units, stock options, and deferred compensation earned while working in a high-tax state such as California or New York. Changing domicile to Florida stops the old state from taxing pay for work performed after the move, but it does nothing to the compensation the executive already earned there. State tax law sources equity and deferred pay to where the underlying services were performed, not to where the executive lives when the income is finally received. This guide explains how restricted stock units and options are sourced after a move, how the federal Source Tax law protects certain deferred compensation, and how the timing of a Florida move interacts with a multi-year vesting schedule.

Does Moving to Florida Eliminate State Tax on My RSUs and Stock Options?

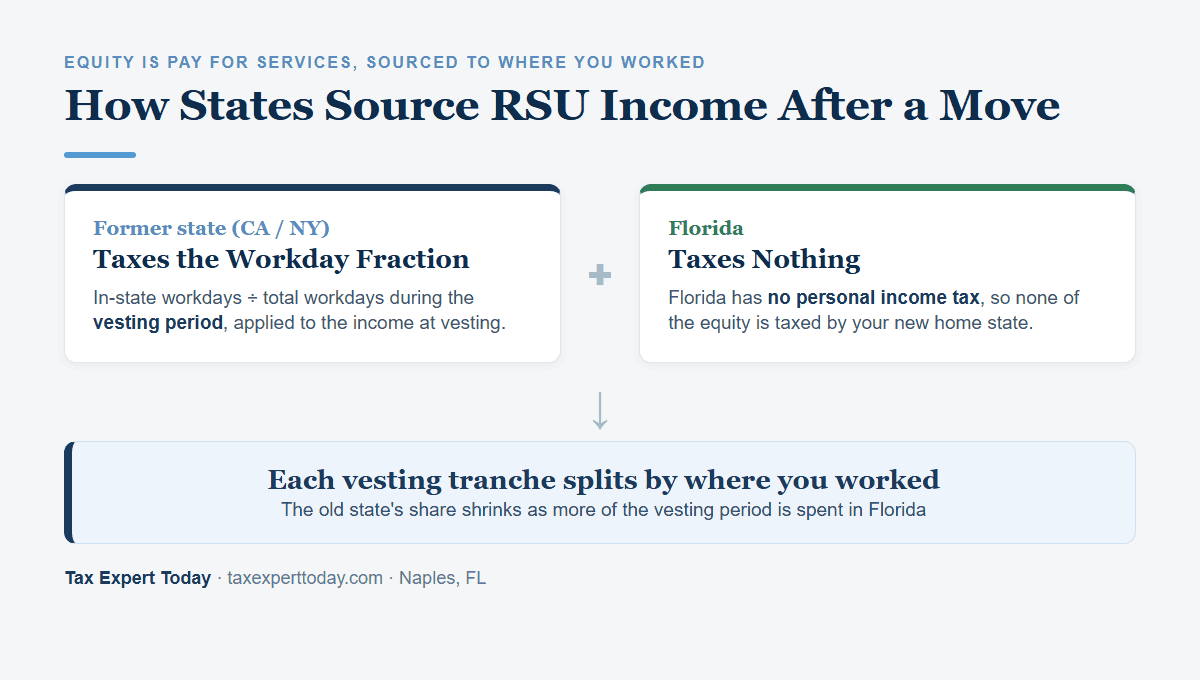

No. Moving to Florida ends the former state’s tax on compensation for work you perform after you become a Florida resident, but the state you left can still tax the part of your restricted stock units and stock options that you earned while working there. Equity compensation is pay for services, and states source it to the location of the work during the vesting period, so a portion tied to in-state workdays remains taxable in the old state even though Florida itself imposes no income tax.

This is why a clean domicile change, while essential, is only half of the planning. The other half is understanding how each tranche of equity is sourced, because a grant that vests over four years can straddle the move and split between two states. For the domicile mechanics themselves, see our guide on how to establish Florida residency.

How Do States Source RSU and Stock-Option Income After You Move?

States source restricted stock unit and stock option income using a workday allocation fraction: the number of workdays performed in the state during the allocation period, divided by total workdays in that period, multiplied by the income recognized at vesting or exercise. For restricted stock units, the allocation period generally runs from the grant date to the vesting date. For nonstatutory stock options, it generally runs from grant to the date the option becomes exercisable or is exercised.

California explains this method in FTB Publication 1004, which allocates option and unit income to California based on California workdays over the vesting period, even for a taxpayer who has since become a nonresident. New York applies a parallel rule in TSB-M-07(7)I, sourcing a nonresident’s equity income by a New York workday fraction. The federal timing of the income itself is set by IRC §83, which treats the shares as compensation when they vest. For a fuller treatment of the California side of a departure, see our guide to the California exit tax.

| Equity type | When it is taxed federally | How the former state sources it |

|---|---|---|

| Restricted stock units | As ordinary income at vesting under IRC §83 | Workday fraction from grant to vest |

| Nonstatutory stock options | On the spread at exercise | Workday fraction from grant to vest or exercise |

| Nonqualified deferred compensation | When paid or made available | Shielded by 4 U.S.C. §114 if paid over ten or more years or over life |

The practical effect is that the executive receives a nonresident return obligation in the former state for years after the physical move, one that shrinks with each vesting tranche as the share of Florida workdays grows. A large capital event alongside the equity, such as a business or stock sale, is a separate timing question covered in moving to Florida before selling a business.

What Is the Federal Deferred-Compensation Shield?

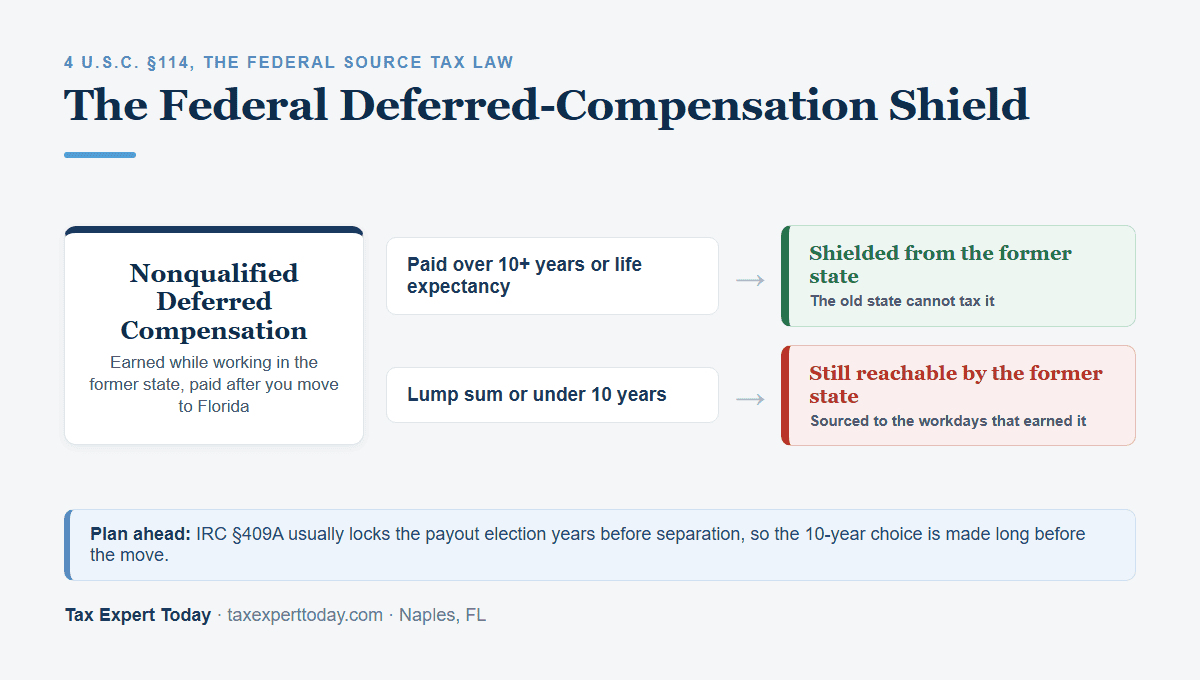

The federal Source Tax law at 4 U.S.C. §114 prohibits any state from taxing the retirement income of a person who is not a resident or domiciliary of that state. Retirement income includes qualified plan distributions and certain nonqualified deferred compensation, but the deferred compensation qualifies only when it is paid in substantially equal periodic payments over the recipient’s life or life expectancy, or over a period of not less than ten years.

This distinction drives the payout election. A nonqualified deferred compensation plan described in IRC §3121(v)(2) that is paid to a Florida resident as a lump sum, or over a period shorter than ten years, falls outside the shield, and the former state can source it to the workdays that earned it. The same plan paid over ten years or more escapes the old state entirely. Because IRC §409A locks deferral and payout elections well before separation, the ten-year decision usually has to be made years ahead of the move, not at the moment of departure.

- Shielded from the former state

- Qualified plan distributions, and nonqualified deferred compensation paid over life expectancy or over a period of at least ten years, under the safe harbor in 4 U.S.C. §114.

- Still reachable by the former state

- Restricted stock units and stock options sourced by workday allocation, and any deferred compensation paid as a lump sum or over fewer than ten years, which the old state can tax on the in-state share.

How Should Executives Time a Florida Move Around Equity Vesting?

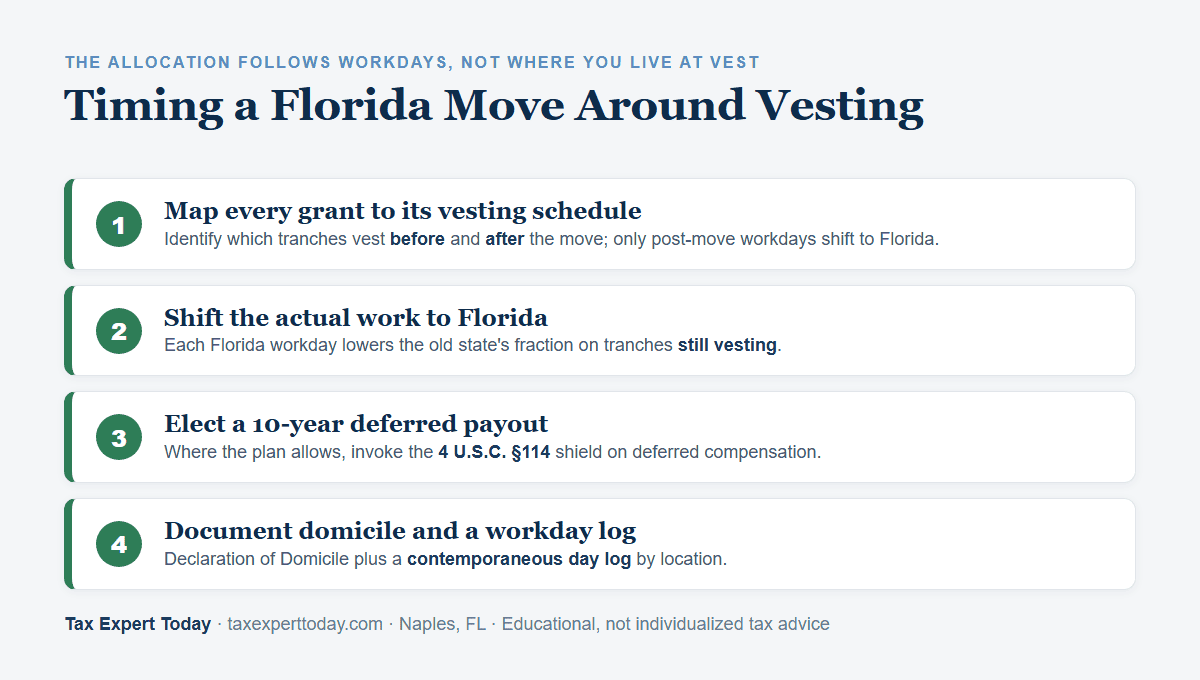

Executives should coordinate the move with the vesting calendar, because the workday allocation is fixed by where services are performed during each vesting period, not by where the executive lives at vest. Moving does not re-source income already earned in the former state, but every workday shifted to Florida after the move lowers the old state’s fraction on tranches that are still vesting, so an earlier move captures more of the multi-year grants.

- Map every open grant and its vesting schedule, and identify which tranches will vest before and after the planned move date, since only the post-move workdays shift toward Florida.

- Relocate physically and change where the work is performed, because the allocation follows workdays, and a remote role that genuinely moves to Florida steadily reduces the former state’s share.

- Review nonqualified deferred compensation elections under IRC §409A well before separation, and where the plan allows it, elect a payout of at least ten years or over life to invoke the 4 U.S.C. §114 shield.

- Establish Florida domicile in a documented way, including a Florida driver license, voter registration, and a Declaration of Domicile, following the full checklist in how to establish Florida residency.

- Keep a contemporaneous workday log by location, because a former-state audit of equity income turns on how many days you actually worked there during each vesting period, the same evidence tested in a Florida residency audit.

- Guard against statutory residency in the old state, since keeping a home and too many days there can pull all of your income back in regardless of domicile, a risk explained in the dual state residency trap.

How Do You Establish Florida Domicile as a Remote Executive?

You establish Florida domicile by making Florida the true center of your life and documenting the change, then cutting the ties that let the former state keep claiming you. The core steps are a Florida driver license, voter registration, a Declaration of Domicile under Florida Statutes §222.17, moving primary banking, advisors, and physicians to Florida, and reducing time and property in the old state. A remote executive has an added factor, which is where the work itself happens, so shifting the actual place of work to Florida reinforces both the domicile record and the workday allocation on future equity.

A documented Florida move also opens the state’s creditor protections, from the unlimited homestead shield to tenancy by the entirety on marital accounts. Our guide on Florida asset protection for new residents covers what a relocating executive should confirm.

Because the deeper checklist and the audit factors are covered in our existing guides, this article does not repeat them. See how to establish Florida residency for the full domicile checklist and the Florida residency audit guide for how a former state tests a claimed move.

Florida Domicile for Executives: Help in Naples and Southwest Florida

Executives who also run a company in a no-income-tax state can review our guide to the Texas franchise tax for business owners.

Tax Expert Today LLC helps executives and business owners in Naples and across Southwest Florida structure a Florida move around equity compensation and deferred pay. That work includes mapping each grant to its vesting schedule, modeling the former state’s workday allocation on restricted stock units and options, reviewing deferred compensation payout elections against the 4 U.S.C. §114 shield, and building the domicile and workday records that survive a former-state review. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, serving clients nationwide. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET. You can review the firm’s Naples tax planning and Florida tax services for related help.

Frequently Asked Questions

Do I owe California tax on RSUs that vest after I move to Florida?

Often yes, in part. California sources restricted stock unit income by the share of California workdays during the vesting period, so units granted while you worked in California and vesting after your move remain partly taxable in California even as a Florida resident. The California portion shrinks for each grant as more of the vesting period is spent working in Florida, and it disappears only once no vesting-period workdays fall in California.

Does establishing Florida domicile protect my deferred compensation?

Only if the deferred compensation is paid in a qualifying form. Under 4 U.S.C. §114, a former state cannot tax nonqualified deferred compensation paid to a nonresident over life expectancy or over a period of at least ten years. The same pay taken as a lump sum, or over a shorter period, falls outside the shield and can still be sourced to the state where you earned it, which makes the payout election as important as the domicile change.

Are stock options and RSUs treated the same way after a move?

They are sourced by the same workday method but on different periods. Restricted stock units are generally allocated over the grant-to-vest period and taxed as ordinary income at vesting, while nonstatutory stock options are generally allocated from grant to the date they become exercisable or are exercised, and taxed on the spread at exercise. In both cases the former state taxes the fraction tied to in-state workdays, and Florida taxes none of it.

Should I move before or after my equity vests?

Moving earlier generally captures more of a multi-year grant, because the workday allocation follows where you perform services during the vesting period. Income already earned in the former state cannot be re-sourced by a later move, but each workday performed in Florida after the move lowers the old state’s fraction on tranches still vesting. The right sequence depends on your grant calendar, your deferred compensation elections, and the statutory residency rules of the state you are leaving.

Where can I get help with executive relocation and equity timing in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps executives in Naples and across Southwest Florida plan a Florida move around restricted stock units, options, and deferred compensation, model the former state’s workday allocation, and document domicile. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and advises clients in residency and tax matters nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional on Executive Relocation and Equity Timing

If you hold multi-year equity grants or a deferred compensation balance and are planning a Florida move, the planning is worth doing before the move rather than after a nonresident notice arrives. The judgment calls are how each grant is sourced across the move, whether a deferred compensation payout can be structured to reach the 4 U.S.C. §114 shield, how to sequence the move against the vesting calendar, and how to keep a workday record that a former state will accept. Those are the points where preparation changes the result, and where representation matters if a residency or sourcing audit opens. Tax Expert Today LLC advises executives on Florida relocation and represents taxpayers in residency and tax matters nationwide.

Call (239) 441-2005 or schedule a consultation to map your grants, test your deferred compensation elections, and structure a Florida move that captures the most of your equity. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 8, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005