By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Texas LLC taxes work differently from those in most states. A Texas LLC pays no state personal income tax on its profits, but it remains subject to the Texas franchise tax, which produces no tax due when annualized total revenue stays at or below $2,650,000 for the 2026 report year. Federal tax still applies in full through pass-through treatment on the owners’ returns, and many LLCs also need a Texas sales tax permit.

What Taxes Does a Texas LLC Actually Pay?

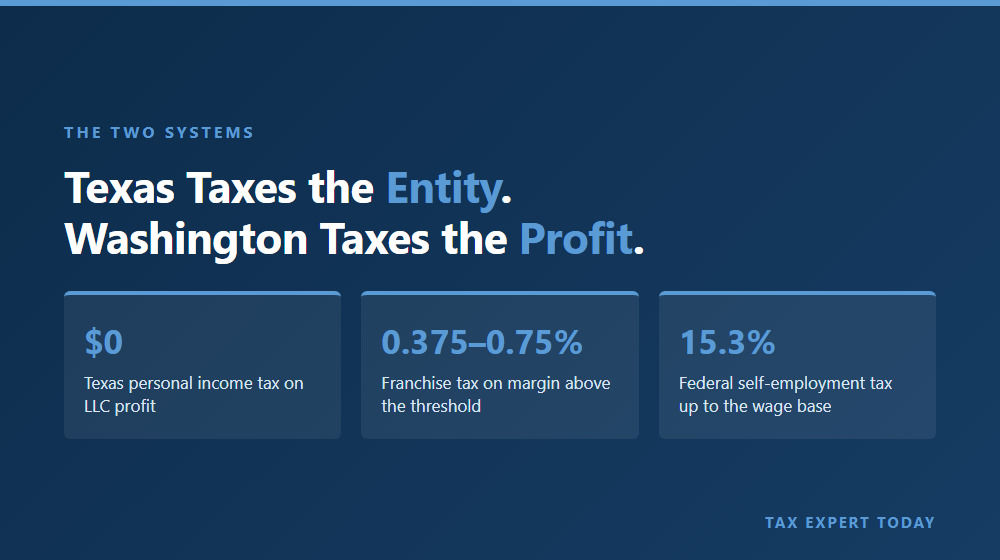

A Texas LLC faces two separate systems. Texas itself imposes no personal income tax, so LLC profits are not taxed by the state on the owner’s individual return. The state instead reaches business entities through the franchise tax under Tex. Tax Code Ch. 171. Separately, the federal government taxes the same profits in full.

That split is the single most useful thing to understand about Texas LLC taxes, and it is where most of the confusion starts. Owners who relocate from a state such as California or New York often hear “Texas has no income tax” and conclude that a Texas LLC is close to tax free. It is not. The federal layer does not change when a business crosses a state line, and it is usually the larger of the two numbers by a wide margin.

The table below summarizes what a Texas LLC generally owes, and the sections that follow explain each line in turn.

| Tax | Applies when | Rate or effect (2026) | Filed with |

|---|---|---|---|

| Texas personal income tax | Never | None; Texas imposes no individual income tax | Not applicable |

| Texas franchise tax | Entity is organized in or doing business in Texas | No tax due at or below $2,650,000 annualized total revenue; otherwise 0.375% or 0.75% of taxable margin | Texas Comptroller |

| Federal income tax | Always, on the owners’ returns by default | The owners’ individual marginal rates | IRS |

| Federal self-employment tax | Generally on active members’ distributive shares | 15.3% up to the Social Security wage base, then 2.9% plus any Additional Medicare Tax | IRS |

| Texas sales and use tax | Selling taxable goods or taxable services in Texas | 6.25% state, plus up to 2% local, for a maximum combined 8.25% | Texas Comptroller |

Does a Texas LLC Pay State Income Tax?

No. Texas does not impose a personal income tax, so an LLC’s profits that flow through to its members are not subject to state income tax in Texas. There is no state return for the members to file on that income, and no state withholding on distributions. This is a genuine structural advantage, not a loophole, and it does not depend on the LLC making any election.

What the absence of an income tax does not mean is that Texas collects nothing from the business. The state funds itself through the franchise tax, sales and use tax, and property tax rather than through an income tax. For an LLC, the franchise tax is the state-level item that most often requires attention, and it is assessed on the entity rather than on the members.

It is worth being precise about the boundary here. Texas not taxing the income does not stop another state from taxing it. An LLC organized in Texas that performs services in a state with an income tax may create nexus there, and income sourced to that state may be taxable on a nonresident return. Members who have not fully severed domicile with a former state may also find that the former state still asserts a claim to the same profits. Those are questions about the other state’s law, not about Texas.

Does My Texas LLC Owe Franchise Tax?

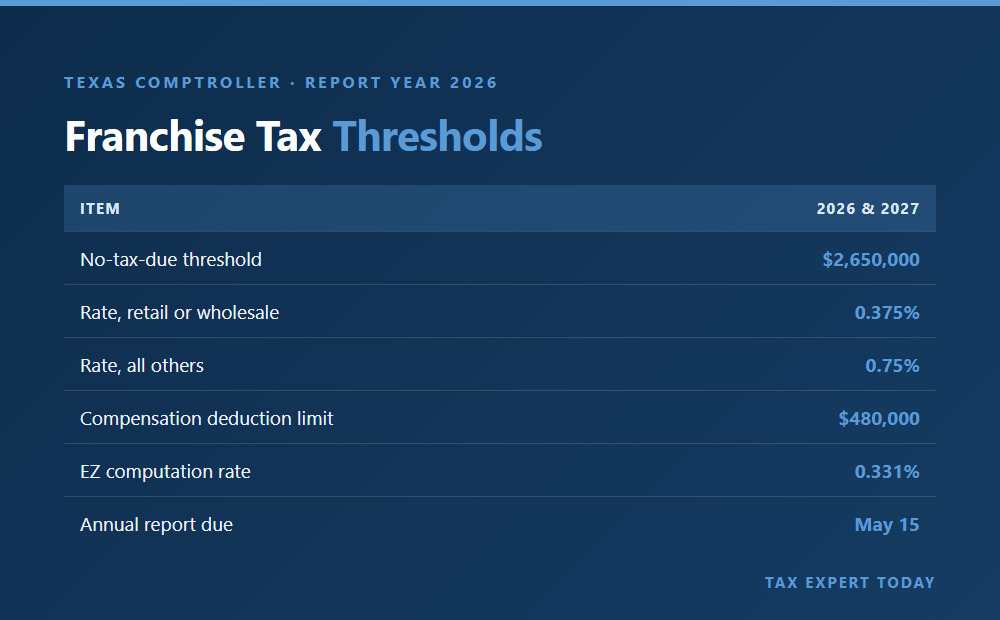

Most small LLCs owe no franchise tax, but nearly all of them still have a filing obligation. For the 2026 and 2027 report years, the Texas Comptroller sets the no-tax-due threshold at annualized total revenue of $2,650,000. An entity at or below that figure owes no franchise tax. An entity above it calculates tax on its taxable margin.

The rates published by the Texas Comptroller for the 2026 report year are as follows.

| Item | 2026 and 2027 report years | 2024 and 2025 report years |

|---|---|---|

| No-tax-due threshold | $2,650,000 | $2,470,000 |

| Tax rate, retail or wholesale | 0.375% | 0.375% |

| Tax rate, other than retail or wholesale | 0.75% | 0.75% |

| Compensation deduction limit per person | $480,000 | $450,000 |

| EZ computation revenue threshold | $20,000,000 | $20,000,000 |

| EZ computation rate | 0.331% | 0.331% |

The filing point deserves emphasis because it is the most common compliance miss on this track. For report years 2024 and later, an entity at or below the no-tax-due threshold is no longer required to file a No Tax Due Report, which was discontinued for reports originally due on or after January 1, 2024. The entity is still required to file Form 05-102, Public Information Report, or Form 05-167, Ownership Information Report. Owners who read “no tax due” as “nothing to file” tend to discover the error when the account falls out of good standing.

Annual franchise tax reports are due May 15. If May 15 falls on a weekend or holiday, the due date moves to the next business day. Our companion guide on the Texas franchise tax walks through the margin calculation methods, the EZ computation, and the mechanics in more depth than this overview allows.

How Is a Texas LLC Taxed at the Federal Level?

By default, the federal government does not treat the LLC as a taxpayer at all. Under the check-the-box rules described on the IRS LLC page, a domestic LLC with at least two members is classified as a partnership, and a single-member LLC is disregarded as an entity separate from its owner. Either way, the profit lands on the owners’ returns.

The practical effect depends on the default classification and on any election the LLC makes.

| Structure | Default federal classification | Where the income is reported |

|---|---|---|

| Single-member LLC, individual owner | Disregarded entity | Schedule C, E, or F on the owner’s Form 1040 |

| Multi-member LLC | Partnership | Form 1065, with each member receiving a Schedule K-1 |

| LLC electing S corporation status | S corporation | Form 1120-S, with each shareholder receiving a Schedule K-1 |

| LLC electing C corporation status | C corporation | Form 1120, with tax paid at the entity level |

Self-employment tax is the item that surprises relocating owners most. Because Texas takes no income tax, the federal self-employment layer becomes proportionally more visible in the total bill. An active member of a multi-member LLC generally pays self-employment tax on the distributive share, and a single-member LLC owner generally pays it on Schedule C net profit, at 15.3% up to the Social Security wage base and 2.9% above it, plus any Additional Medicare Tax. Owners can model the effect with our self-employment tax calculator.

Because no state or employer withholds on this income, quarterly estimated payments generally carry the burden. Underpaying them invites an addition to tax that has nothing to do with Texas and everything to do with federal timing rules. Our quarterly estimated tax calculator is a useful starting point for that projection.

Should a Texas LLC Elect S Corporation Status?

An S corporation election is a federal election, not a Texas one, and it is the planning lever owners ask about most. An LLC that meets the eligibility requirements of IRC §1361 may elect S corporation treatment by filing Form 2553. The LLC keeps its state-law identity as an LLC and simply changes how the IRS characterizes it.

The mechanism is straightforward. An S corporation pays its owner-employees reasonable compensation as W-2 wages, which carry employment taxes, and the remaining profit passes through as a distributive share that is generally not subject to self-employment tax. Where the facts support it, that can reduce the total employment tax burden relative to the default classification.

The election is not free, and it is not right for every LLC. Payroll must actually be run, the compensation must be reasonable rather than nominal, a separate Form 1120-S is required, and basis and distribution rules become materially less forgiving. The eligibility limits in §1361 also matter, since an S corporation may not have more than 100 shareholders, may generally not have nonresident alien shareholders, and may have only one class of stock. Whether the election helps depends on profit level, the reasonable compensation the role commands, and the owner’s other circumstances.

The franchise tax interaction is worth naming, because owners often assume the election changes it. It generally does not. Texas taxes the entity based on its total revenue and margin, and an entity that is a taxable entity under Chapter 171 remains one regardless of how it is classified federally. Electing S corporation status is a federal employment tax decision, not a franchise tax strategy.

Does a Texas LLC Need a Sales Tax Permit?

An LLC needs a Texas sales tax permit if it sells, leases, or rents taxable goods, or provides taxable services, in Texas. Texas imposes a 6.25% state sales and use tax, and local taxing jurisdictions may add up to 2%, for a maximum combined rate of 8.25%. Registration is required before making taxable sales, and the permit itself carries no fee.

Service businesses are where this gets misread. Texas does not tax services generally; it taxes an enumerated list of taxable services. Data processing, information services, security services, and real property repair are on that list, while many professional services are not. Two consultants with similar-sounding businesses can land on opposite sides of that line, so the classification question deserves an actual answer rather than an assumption early on.

Remote sellers have a separate safe harbor. Under the Comptroller’s remote seller rules, a remote seller with total Texas revenue of less than $500,000 in the preceding twelve calendar months is not required to obtain a permit or to collect, report, and remit state and local use tax. Total Texas revenue for that test is measured on gross revenue from both taxable and nontaxable sales of tangible personal property and services into Texas, which is broader than many owners expect.

What Do Owners Get Wrong About Texas LLC Taxes?

Five errors account for most of the avoidable problems we see on Texas engagements. None of them are exotic, and each follows from the same root cause, which is treating “no state income tax” as though it settled the whole question.

- Assuming no tax due means no filing. The franchise tax report threshold and the information report requirement are different obligations. An LLC under the threshold still files Form 05-102 or Form 05-167, and skipping it can put the entity out of good standing.

- Forgetting the federal layer entirely. Moving to Texas changes the state math. It changes nothing about federal income tax or self-employment tax on the same profit.

- Treating the S corporation election as automatic. The election requires real payroll, reasonable compensation, and a separate return. Where those are not actually implemented, the intended benefit generally does not survive review.

- Ignoring trailing nexus in the former state. An LLC that still has employees, inventory, or customers in a prior state may still have filing obligations there, and the members’ own domicile may still be contested if the move was not fully documented.

- Missing the sales tax permit. Because the taxable services list is specific rather than general, businesses that assumed they were exempt sometimes discover an uncollected liability that they cannot bill back to customers after the fact.

Texas LLC Tax Help in Naples & Southwest Florida

Tax Expert Today LLC advises business owners on Texas LLC taxes, franchise tax reporting, entity classification, and multi-state compliance from our office at 11983 Tamiami Trail N, Naples, FL 34110. Our team includes tax advisors, enrolled agents, CPAs, and attorneys, and we work with clients in all 50 states, so a Texas LLC owner does not need to be in Texas to work with us. Texas franchise tax and sales tax are state matters handled through the Texas Comptroller rather than the IRS, and the engagement is scoped accordingly. To discuss an entity, call (239) 441-2005, Monday through Friday, 10am to 5pm ET.

When to Engage a Professional

Some Texas LLC questions are administrative and some are structural. Filing a Public Information Report is administrative. Deciding whether an S corporation election fits, whether a service is taxable, whether a former state still has a claim on the profit, or whether revenue is approaching the franchise tax threshold is structural, and the cost of getting those wrong compounds quietly across years.

Engaging a professional generally makes sense when annualized revenue is approaching $2,650,000, when the LLC operates in more than one state, when members have recently relocated, when an S corporation election is on the table, or when the taxable status of what the business sells is genuinely unclear. Outcomes depend on the specific facts, and this guide is educational rather than advice on any particular entity. You can also review our Texas tax services to see how we typically scope this work.

Frequently Asked Questions

Does a Texas LLC pay state income tax?

No. Texas imposes no personal income tax, so LLC profits flowing through to members are not subject to Texas income tax. The state instead reaches businesses through the franchise tax under Tex. Tax Code Ch. 171, along with sales and use tax and property tax. Federal income tax and self-employment tax still apply in full.

How much is the Texas franchise tax for an LLC?

For the 2026 report year, an LLC with annualized total revenue at or below $2,650,000 owes no franchise tax. Above that threshold, the rate is 0.375% of taxable margin for retail or wholesale entities and 0.75% for others. An EZ computation at 0.331% is available to entities at or below $20,000,000 in total revenue.

Does a single-member Texas LLC file its own tax return?

Not federally, by default. The IRS treats a single-member LLC as a disregarded entity, so the activity is reported on the owner’s Form 1040, generally on Schedule C, E, or F. The LLC may still have its own Texas franchise tax report obligation and its own sales tax permit obligation as a separate entity.

Can a Texas LLC elect S corporation status?

Yes, where the LLC meets the eligibility requirements of IRC §1361 and files Form 2553 with the IRS. The election changes federal classification only, and the LLC keeps its state-law identity. Whether the election reduces total tax depends on profit level, reasonable compensation for the owner’s role, and the cost of running payroll and filing Form 1120-S.

Where can I get help with Texas LLC taxes in Naples, FL?

Tax Expert Today LLC works with Texas LLC owners from 11983 Tamiami Trail N, Naples, FL 34110, and serves clients in all 50 states. The team includes tax advisors, enrolled agents, CPAs, and attorneys covering entity classification, franchise tax reporting, sales tax questions, and multi-state compliance. Call (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Published July 15, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005