By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: A state residency audit is a review by your former state to decide whether you genuinely changed your domicile to Florida or stayed a taxable resident of the state you left. High-tax states such as New York and California examine departing residents closely because Florida imposes no state income tax. Two questions decide the outcome, whether you changed your domicile and whether you are still a statutory resident, and both turn on documentary proof of where your life is actually centered. A move documented in advance is far easier to defend than one reconstructed after a notice arrives.

Published: June 2026

Moving to Florida removes the state income tax bill, but it does not end your old state’s interest in you. When a high earner leaves New York, California, New Jersey, Illinois, or another high-tax state for Naples or anywhere in Florida, the departing state often reviews the move to confirm the change was real rather than a mailing address on paper. That review is a residency audit, and it tends to focus on the year of a large one-time event such as a business sale, a stock award that vests, or a retirement payout. This guide explains how a Florida residency audit works, the two tests that decide it, what auditors actually examine, and how to establish Florida domicile in a way that holds up if your former state asks questions.

What Is a State Residency Audit?

A state residency audit is an examination by your former state’s tax authority to determine whether you remained a taxable resident there after claiming a move to Florida. The state requests records covering where you lived, worked, and spent your days, then weighs them against its own residency tests. If the state concludes you never truly left, it can assess income tax, interest, and penalties on income you reported only to Florida, which collects none.

These audits are document driven rather than opinion driven. The auditor is not asking whether you like Florida. The auditor is reconciling cell phone records, credit card statements, travel records, and property use against the day counts and connection factors the state’s law sets out. That is why preparation before the move matters far more than argument after the notice.

Why Do States Audit People Who Move to Florida?

States audit Florida moves because Florida has no state income tax, so every confirmed departure is revenue the former state loses permanently. New York, California, and similar states fund a large share of their budgets from a small number of high earners, which gives them a strong incentive to verify that a high-income departure is genuine. The audit risk rises sharply in any year with a large, mobile item of income.

Certain events reliably draw attention. Selling a business or a large block of stock, exercising options, receiving deferred compensation, or taking a substantial retirement distribution in the same year you claim a new domicile creates a visible mismatch the state can flag. A part-year return, a recently sold former home, or keeping a home and strong ties in the old state can all trigger a closer look. None of these facts is fatal on its own, but together they signal that the file is worth opening.

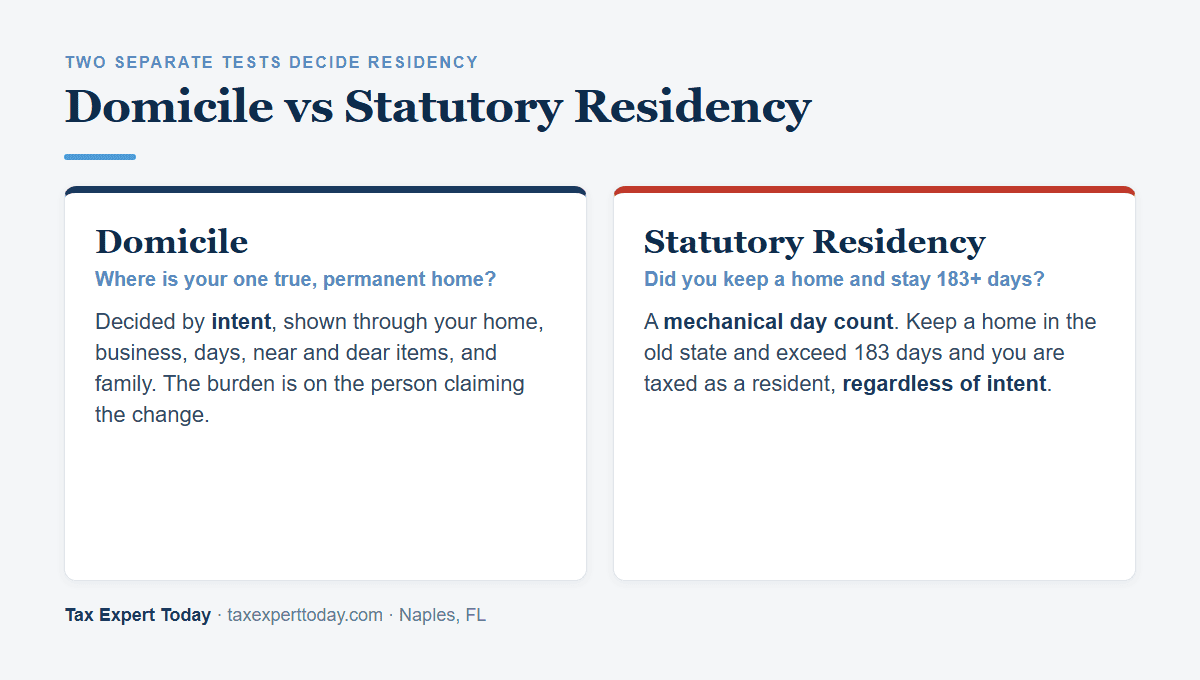

What Is the Difference Between Domicile and Statutory Residency?

Domicile is the one place you treat as your true, fixed, permanent home and intend to return to, while statutory residency is a separate day-count rule that can tax you as a resident even if your domicile is elsewhere. Most high-tax states apply both tests, so you can win the domicile question and still be taxed as a resident if you spend too many days in the old state. Defending a move means satisfying both.

Snowbirds and part-year residents face this most directly, because keeping a home and too many days in the old state can trigger a second residency. Our guide on dual state residency and the snowbird tax trap explains how to clear both tests.

| Test | What it asks | How it is decided |

|---|---|---|

| Domicile | Where is your one true, permanent home? | Intent shown through the connection factors below; the burden is on the person claiming the change |

| Statutory residency | Did you keep a home in the old state and spend more than 183 days there? | A mechanical count of days, regardless of intent; under New York Tax Law §605(b) a part of a day generally counts as a full day |

The statutory test is the trap most people miss. You can move your life to Naples, file a Declaration of Domicile, and still be taxed as a New York resident if you kept an apartment there and spent 184 days in the state, because that test does not care about intent. Counting days carefully, and keeping the proof, is as important as the domicile evidence.

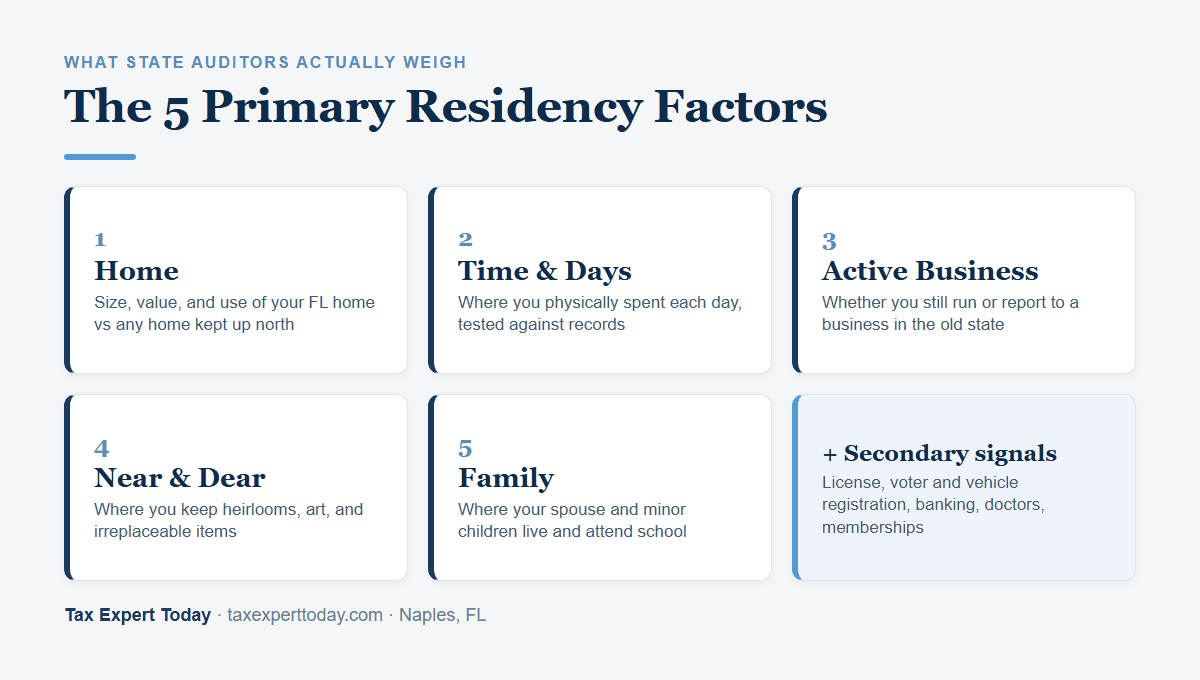

What Do Residency Auditors Actually Examine?

Auditors weigh a defined set of connection factors to judge where your life is centered, not a single document. State audit guidelines, including the New York State Nonresident Audit Guidelines that auditors follow, group the strongest evidence into a handful of primary factors and treat the rest as supporting detail. The five primary factors carry the most weight.

- Home

- The size, value, and use of your Florida home compared with any residence you kept in the old state. A primary home in Naples and a sold or clearly secondary property up north is strong evidence; keeping a larger, year-round home in the old state cuts the other way.

- Time and days

- Where you physically spent your days across the year. This is the factor auditors can test against phone, card, toll, and travel records, so a contemporaneous day log is worth more than a recollection.

- Active business involvement

- Whether you still run a business or report daily to an office in the former state. Passive ownership weighs less than showing up in person to manage operations.

- Near and dear items

- Where you keep the things you value most, such as heirlooms, art, collections, and family records. Auditors read the location of irreplaceable items as a sincere signal of where home really is.

- Family connections

- Where your spouse and minor children live and attend school. A spouse and children who remain in the old state make a claimed move much harder to sustain.

Secondary signals fill in the picture, including your driver license, voter registration, vehicle registration, the address on your federal return, where you bank and see doctors, and club or religious memberships. No single item decides the audit, but the factors should point in the same direction. Contradictions, such as a Florida Declaration of Domicile paired with a New York gym checked in to four days a week, are exactly what auditors look for.

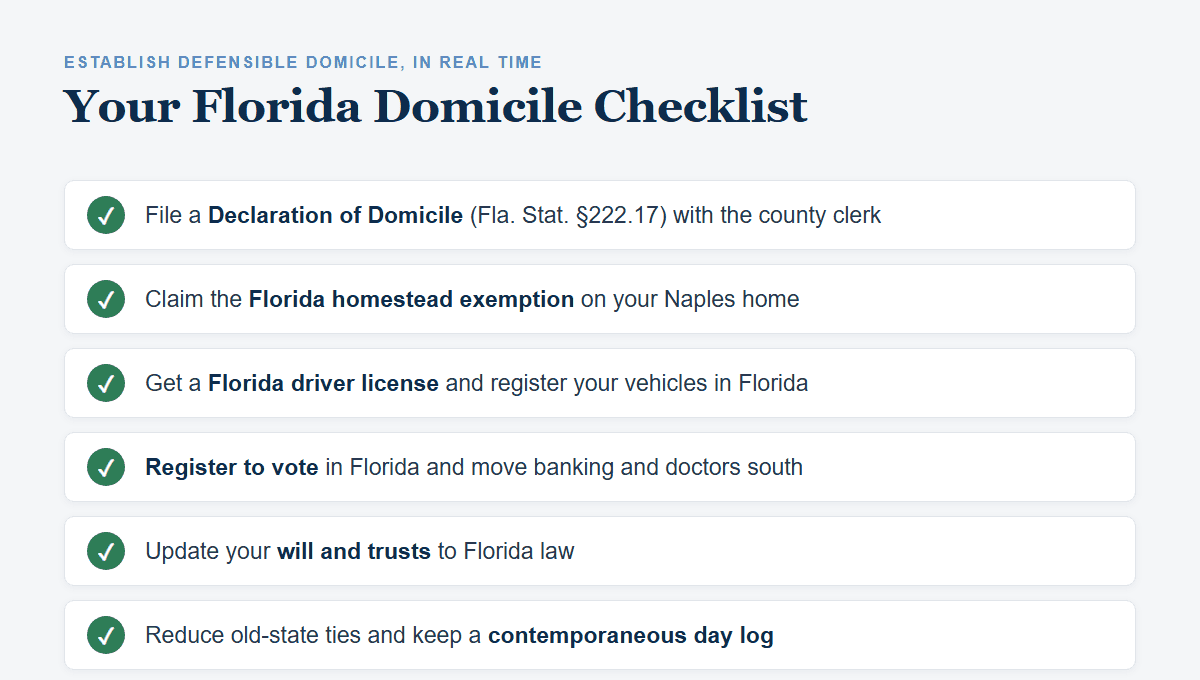

How Do You Establish Florida Domicile That Survives an Audit?

You establish defensible Florida domicile by taking concrete, dated steps that show Florida is your true home, ideally completed in the same window as the move rather than months later. Florida law at Florida Statutes §196.015 lists many of these same actions as evidence of intent to make Florida a permanent residence, which makes the checklist below both practical and grounded in statute.

The same domicile record also supports Florida’s creditor protections, because the homestead shield and the Chapter 222 exemptions apply to a Florida resident. See our guide on Florida asset protection for new residents for how those protections work.

- File a Declaration of Domicile with the clerk of court in your Florida county, such as Collier County for a Naples move.

- Apply for the Florida homestead exemption on your Naples home, which under Florida Statutes §196.012 requires that the home be your permanent residence.

- Obtain a Florida driver license and surrender the old state license, and register your vehicles in Florida.

- Register to vote in Florida and actually vote there.

- Move your banking, financial accounts, and primary physician to Florida, and update the home address on your federal tax return and passport.

- Update your estate plan, including your will and any trusts, to reflect Florida residence and Florida law.

- Reduce ties to the old state by selling or genuinely downgrading the former home and resigning local memberships, and keep a day log proving where you spend your time.

The deeper version of this checklist, including the estate and trust steps that pair with a Florida move, is covered in our guide on how to establish Florida residency. Doing these things contemporaneously, and keeping the receipts, is what converts a claimed move into a documented one.

How Does the 183-Day Rule Affect a Residency Audit?

The 183-day rule is the statutory residency test, and it can tax you as a resident of your old state if you kept a permanent home there and spent more than half the year in the state, regardless of where your domicile is. Because many states count any part of a day spent in the state as a full day, the count is stricter than it sounds, and a travel day through a major airport can count.

The practical defense is to keep a permanent home out of the old state if possible, spend well under the day threshold, and document it as you go rather than reconstruct it later. You can model how the day count works with our Florida 183-day rule calculator, then keep a contemporaneous log supported by travel and card records so the number is defensible if the state asks.

Florida Residency Audit Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and business owners in Naples and across Southwest Florida plan and document a move to Florida and respond to residency audits from former states. That work includes structuring the timing of the move around a business sale or other large income event, building the domicile file before the return is filed, and representing the taxpayer if the old state opens an audit. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, serving clients nationwide. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET. You can review the firm’s audit support and Naples tax planning services for related help.

Frequently Asked Questions

How long does a state residency audit take?

A state residency audit commonly runs 12 to 24 months from the initial information request to a final determination, and longer if the case is contested through the state’s appeals process. The timeline depends on how complete your records are. A taxpayer who can produce a contemporaneous day log, travel records, and a documented domicile file generally resolves the audit faster than one who has to reconstruct a year after the fact.

Can I be taxed as a resident of two states in the same year?

Yes. Because domicile and statutory residency are separate tests, you can be treated as a statutory resident of your old state while also being a Florida resident, which can expose the same income to tax in the departing state. Florida levies no state income tax, so it offers no offsetting credit, which makes losing the statutory residency test costly. Counting days carefully and limiting time in the former state is the way to avoid this result.

Does filing a Florida Declaration of Domicile end the audit risk?

No. A Declaration of Domicile under Florida Statutes §222.17 is useful evidence of intent, but it is one factor among many and does not override the day-count test or contrary facts. An auditor weighs the declaration against where you actually spent your time, kept your home, ran your business, and located your family. The declaration helps most when the rest of your record points the same way.

What records should I keep to defend a Florida move?

Keep a contemporaneous day log showing where you were each day, supported by travel itineraries, credit card and cell phone records, and toll or mileage data. Keep proof of the domicile steps as well, including the Declaration of Domicile, homestead approval, Florida driver license, voter registration, and vehicle registration. The goal is a file assembled as the year happens, because records created in real time carry far more weight than a summary built after a notice arrives.

Where can I get help with a Florida residency audit in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps individuals and business owners in Naples and across Southwest Florida document a move to Florida, plan the timing around large income events, and respond to residency audits from former states. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers in residency and tax matters nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a Residency Audit

If you are moving to Florida in a year that includes a business sale, a large stock or option event, deferred compensation, or a major retirement distribution, the move is worth planning before the calendar year closes rather than after. When the income event is a company sale, our guide on moving to Florida before selling a business explains how the timing of the domicile change affects the tax on the gain. The judgment calls are the timing of the move relative to the income event, how to handle a home you want to keep in the old state, and how to build a record that satisfies both the domicile and the statutory residency tests. Those are the points where preparation prevents an assessment, and where representation matters if an audit opens. Tax Expert Today LLC advises individuals and business owners on Florida relocation and represents taxpayers in residency and tax matters nationwide.

Call (239) 441-2005 or schedule a consultation to plan your move to Florida, time it around a major income event, and build a residency file that holds up. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 29, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005