By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

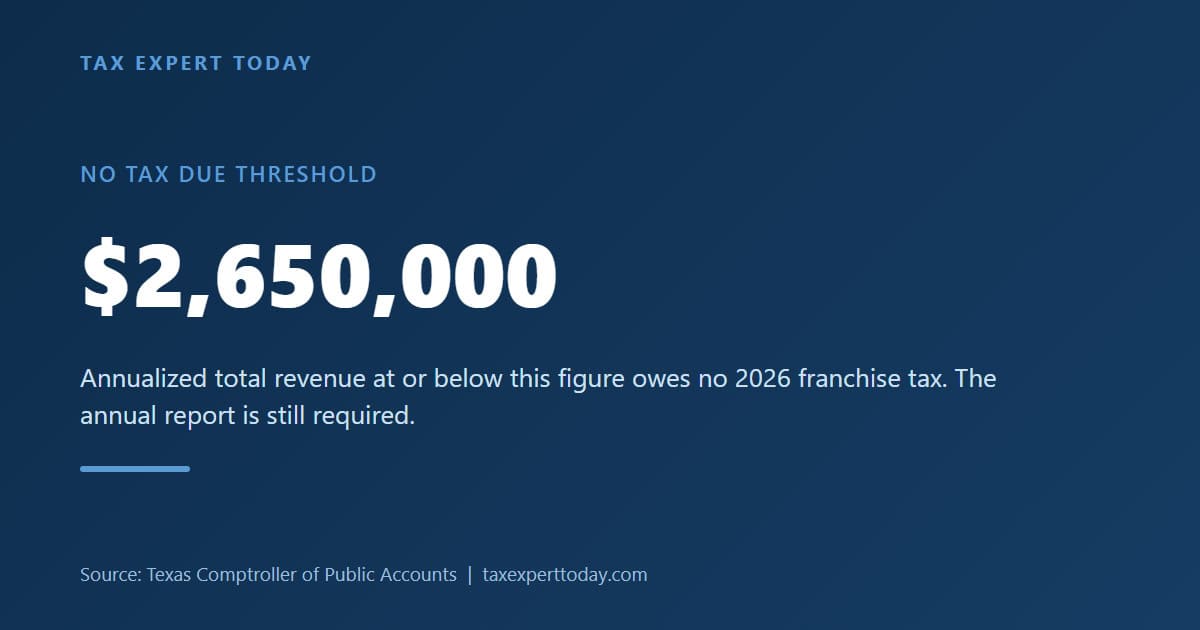

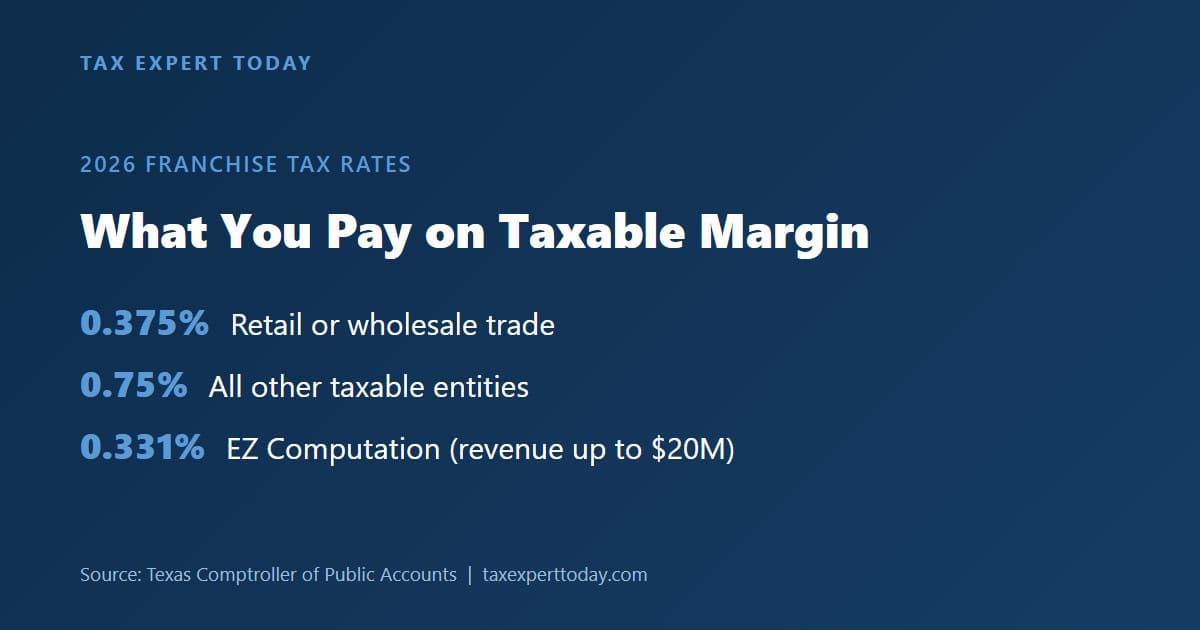

Quick Answer: The Texas franchise tax is a privilege tax the Texas Comptroller imposes on most business entities formed in or doing business in Texas, including LLCs, corporations, and partnerships. For the 2026 report year, an entity owes no tax if its annualized total revenue is at or below the $2,650,000 no-tax-due threshold. Above that, tax is calculated on taxable margin at 0.375 percent for retail or wholesale businesses and 0.75 percent for all others.

If your entity is an LLC, our companion guide on Texas LLC taxes covers how the franchise tax fits alongside federal pass-through treatment, the S corporation election, and sales tax permits.

What Is the Texas Franchise Tax?

The Texas franchise tax is a privilege tax imposed on each taxable entity that is formed in Texas or does business in Texas, under Tex. Tax Code Chapter 171. It is a state-level tax administered by the Texas Comptroller of Public Accounts. It is not a federal tax and is entirely separate from anything reported to the IRS on a business return.

Texas has no personal income tax, so many owners assume the state imposes no business-level tax either. That assumption is the single most common franchise tax error. The franchise tax reaches most limited liability companies, corporations, S corporations, professional associations, and limited partnerships, even when the entity owes zero dollars in a given year.

Who Has to Pay Texas Franchise Tax?

Most taxable entities that are chartered in Texas or that do business in Texas are subject to the franchise tax. This includes LLCs, C corporations, S corporations, professional associations, business trusts, and most limited partnerships. Sole proprietorships and general partnerships owned entirely by natural persons are generally not taxable entities for franchise tax purposes.

The word “subject to” matters. An entity can be subject to the franchise tax and still owe no tax because its revenue falls at or below the no-tax-due threshold. Being subject to the tax means the entity still has an annual reporting obligation, even in a zero-tax year. The following entity types are generally covered:

- Limited liability companies (single-member and multi-member)

- C corporations and S corporations

- Professional associations and professional corporations

- Limited partnerships and limited liability partnerships

- Business trusts and certain other legal entities

Federal classification is a separate question. An LLC may be a disregarded entity or a partnership for IRS purposes under the federal LLC rules, yet it remains one taxable entity for the Texas franchise tax. The two systems do not mirror each other.

What Is the No-Tax-Due Threshold for 2026?

For the 2026 report year, the no-tax-due threshold is $2,650,000 in annualized total revenue. An entity whose annualized total revenue is at or below that figure owes no franchise tax. The threshold is indexed periodically, so it is not a fixed number. The table below shows how it has changed by report year, per the Texas Comptroller.

| Report Year | No-Tax-Due Threshold | Rate (Retail/Wholesale) | Rate (Other) |

|---|---|---|---|

| 2026 and 2027 | $2,650,000 | 0.375% | 0.75% |

| 2024 and 2025 | $2,470,000 | 0.375% | 0.75% |

| 2022 and 2023 | $1,230,000 | 0.375% | 0.75% |

A change that catches many owners: for report years 2024 and later, an entity at or below the threshold is no longer required to file a separate No Tax Due Report. The Comptroller discontinued that form for reports originally due on or after January 1, 2024. The entity still must file Form 05-102, Public Information Report, or Form 05-167, Ownership Information Report. Skipping that filing because “no tax is due” is a frequent and avoidable mistake.

How Is the Texas Franchise Tax Calculated?

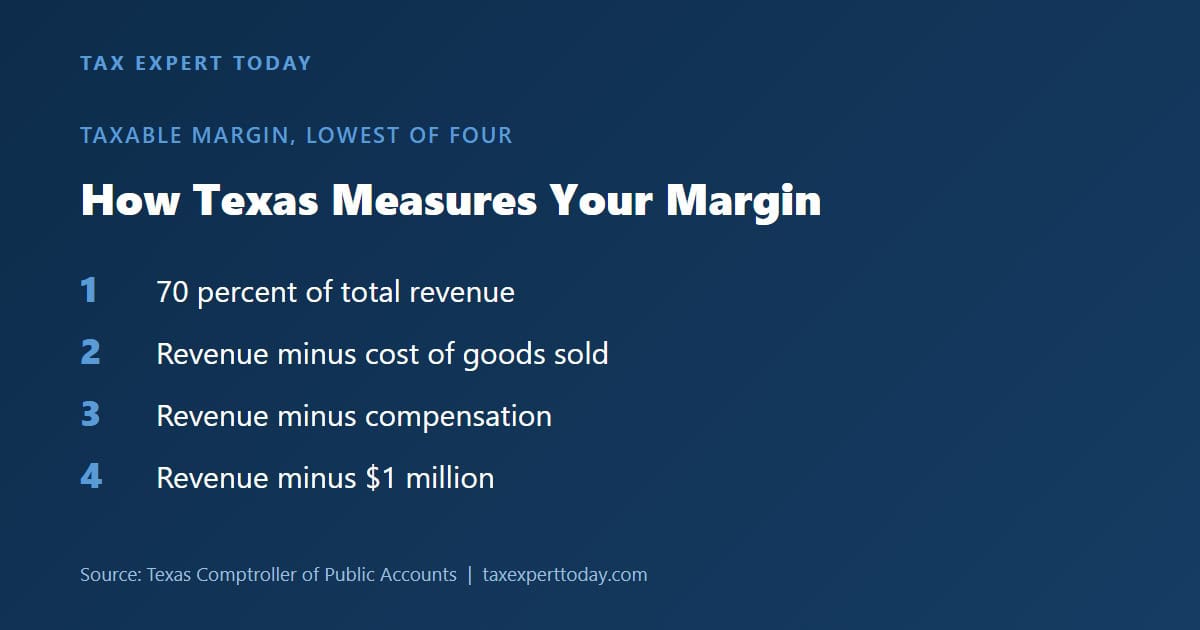

The franchise tax is calculated on taxable margin, not on net income. Under Tex. Tax Code Section 171.101, an entity computes margin as the lowest result of four allowed methods, then apportions that margin to Texas and applies the rate. Because the statute lets you use the lowest of the four, method selection is where planning matters most.

| Margin Method | Formula | Best For |

|---|---|---|

| 70% of revenue | Total revenue × 0.70 | Low-cost, high-margin service firms |

| Revenue minus COGS | Total revenue − cost of goods sold | Manufacturers, retailers, and wholesalers |

| Revenue minus compensation | Total revenue − wages and benefits (capped per person) | Labor-heavy or professional-services firms |

| Revenue minus $1 million | Total revenue − $1,000,000 | Smaller entities just above the threshold |

The compensation deduction is capped per person. For the 2026 report year the wage-and-cash-compensation deduction limit is $480,000 per employee or officer, per the Comptroller schedule. Once margin is determined, it is multiplied by the apportionment factor (Texas gross receipts divided by total gross receipts) and then by the applicable rate.

How the math works: Consider an entity that is not retail or wholesale, with $4,000,000 in total revenue, all sourced to Texas, and $1,500,000 in eligible compensation. The revenue-minus-compensation method yields a $2,500,000 margin, and at the 0.75 percent rate the franchise tax is $18,750. The 70 percent method would produce a $2,800,000 margin, so the compensation method is lower and would be selected. The figures are illustrative and depend on each entity’s facts.

What Is the EZ Computation Report?

The EZ Computation is a simplified filing available to an entity or combined group with annualized total revenue of $20 million or less. It applies a lower rate of 0.331 percent to apportioned total revenue, with no margin subtraction. In exchange for the simpler math, an entity using the EZ method may not take any margin deduction, may not claim franchise tax credits, and may not carry over the temporary credit for business loss carryforward.

The EZ Computation is a convenience option, not always the cheapest one. For a labor-heavy business, the long-form report using the compensation deduction often produces a lower tax even after the higher rate. Comparing both computations before filing is a routine planning step.

When Is the Texas Franchise Tax Report Due?

The annual franchise tax report is due May 15 each year, covering the prior year of activity. If May 15 falls on a weekend or holiday, the due date moves to the next business day. An entity may request an extension, though an extension of time to file is not an extension of time to pay any tax owed.

Newly formed or newly registered entities file an initial report, and entities that close must file a final report to end the reporting obligation. Missing the annual filing, even in a no-tax-due year, can place the entity in a “not in good standing” status and can eventually lead to forfeiture of its right to transact business in Texas.

How Does Apportionment Work for the Texas Franchise Tax?

Apportionment decides how much of a multistate entity’s margin Texas may tax. Texas uses a single-factor formula under Tex. Tax Code Section 171.106: Texas gross receipts divided by gross receipts everywhere. That ratio is multiplied by total margin to give the margin actually subject to Texas tax. Sourcing rules decide which receipts count as Texas receipts.

Apportionment is where owners of businesses operating in more than one state most often overpay or underpay. Receipts genuinely sourced outside Texas reduce the Texas factor and therefore the tax, but only when the sourcing is documented correctly. A business selling into many states, or delivering services to out-of-state customers, should confirm how each receipt category is sourced before filing rather than defaulting every dollar to Texas.

Do Out-of-State Businesses Owe Texas Franchise Tax?

An entity formed outside Texas can still owe the franchise tax when it is doing business in Texas. Beyond physical presence, the Comptroller applies an economic-nexus standard: a foreign entity with Texas gross receipts of $500,000 or more in a period has franchise tax nexus under 34 Tex. Admin. Code Section 3.586, even without property or employees in the state.

This reaches many remote and e-commerce sellers that never set foot in Texas. An out-of-state entity that later ends its Texas nexus does not simply stop filing; it must file a final report and pay any amount due within 60 days of ceasing to have nexus, per the Texas Comptroller. Owners expanding into Texas, or winding down a Texas presence, should test nexus in both directions.

What Happens If You Do Not File the Texas Franchise Tax Report?

Missing the franchise tax report carries escalating consequences, even in a year when no tax is owed. The Comptroller assesses a flat penalty on each late report, adds a percentage penalty when tax is paid late, and can ultimately strip the entity of its right to do business in Texas until the account is brought current. The table below summarizes the standard consequences.

| Situation | Consequence |

|---|---|

| Report filed after the due date | $50 penalty per report |

| Tax paid 1 to 30 days late | 5% penalty on the tax due |

| Tax paid more than 30 days late | 10% penalty on the tax due, plus interest |

| Prolonged nonfiling | Loss of the right to transact business and forfeiture of corporate privileges until reinstated |

Forfeiture is reversible, but only by filing the delinquent reports, paying what is due with penalties and interest, and requesting reinstatement. Because the reporting obligation continues in no-tax-due years, the cleanest protection is simply filing on time every year, including the Public Information Report or Ownership Information Report when no tax is owed.

Common Texas Franchise Tax Mistakes Business Owners Make

Most franchise tax problems come from a handful of recurring errors rather than from the calculation itself. The most frequent are these:

- Assuming no tax means no filing. An entity below the threshold still files the Public Information Report or Ownership Information Report.

- Using only one margin method. The statute allows the lowest of four; testing only one can overstate the tax.

- Defaulting to the EZ Computation. For compensation-heavy firms the long form is often lower.

- Ignoring apportionment. Revenue sourced outside Texas reduces the Texas margin and is easy to overlook.

- Forgetting the final report on closure. Without it, the reporting obligation and standing issues continue after the business stops operating.

Texas Franchise Tax Help in Naples & Southwest Florida

Tax Expert Today LLC is a multidisciplinary tax-advisory firm based at 11983 Tamiami Trail N, Naples, FL 34110, reachable at (239) 441-2005, open Monday through Friday, 10:00 a.m. to 5:00 p.m. ET. The firm works with business owners on state tax matters nationwide, and Texas franchise tax planning is a core part of our Texas tax services. Texas clients are served from the Naples office alongside clients across all 50 states, so a business owner in Houston, Austin, Dallas, or San Antonio receives the same margin-method analysis and filing review as a local one. The team brings CPA, EA, and advisory credentials to entity structure, margin computation, and multi-state apportionment questions.

When to Engage a Professional

Consider professional guidance when your entity approaches or crosses the no-tax-due threshold, when you operate in more than one state, when you are choosing between the EZ Computation and the long form, or when you are forming, restructuring, or closing a Texas entity. Business owners weighing a move to a no-income-tax state can also review our guidance on domicile planning for executives and on timing a relocation before a business sale. Whether a particular method or filing position applies depends on your specific facts and is subject to review by the Texas Comptroller. To discuss your situation, call Tax Expert Today at (239) 441-2005.

Frequently Asked Questions

Does an LLC with no income owe Texas franchise tax?

An LLC below the 2026 no-tax-due threshold of $2,650,000 in annualized total revenue owes no franchise tax. It still must file the Public Information Report or Ownership Information Report each year, because the reporting obligation continues even when no tax is due.

Is the Texas franchise tax the same as an income tax?

No. The franchise tax is a privilege tax on taxable margin, not a tax on net income, and Texas imposes no personal income tax. Margin is computed under Tex. Tax Code Section 171.101 as the lowest of four allowed methods, then apportioned to Texas and multiplied by the applicable rate.

What is the Texas franchise tax rate for 2026?

For the 2026 report year, the rate is 0.375 percent for entities primarily engaged in retail or wholesale trade and 0.75 percent for all other taxable entities. Entities using the EZ Computation apply a 0.331 percent rate to apportioned total revenue with no margin deduction.

When is the Texas franchise tax report due?

The annual report is due May 15, covering the prior year. If May 15 falls on a weekend or holiday, the deadline moves to the next business day. An extension of time to file does not extend the time to pay any tax owed.

Where can I get help with Texas franchise tax in Naples, FL?

Tax Expert Today LLC at 11983 Tamiami Trail N, Naples, FL 34110, telephone (239) 441-2005, advises business owners on Texas franchise tax and multi-state matters. The firm serves Texas clients nationwide from its Naples office and can review margin methods, thresholds, and annual filings for entities of most sizes.

Published July 12, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005