By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Florida estate planning changes in three ways when you move. Florida imposes no state estate tax and no state income tax on trusts, so the state-level drag disappears. The federal estate tax still applies, with a $15,000,000 per-person exclusion in 2026. The rest surprises new residents: your former state can still tax property you left behind, a trust drafted there can remain taxable there, and Florida law restricts who inherits your homestead.

Published: July 2026

People move to Florida for the weather, the absence of a state income tax, and, for many high earners and retirees, for what happens to the estate. On that last point Florida delivers: there is no state estate tax, no inheritance tax, and no state income tax reaching the trusts you administer here. The part that gets less attention is that a move does not carry your existing plan with it cleanly. Your documents were drafted under another state’s law, your trusts may still answer to that state’s tax authority, the property you left behind is still sitting in that state’s estate tax base, and Florida law has its own rules about who must inherit your home and what your spouse is entitled to claim. This guide explains what actually changes on the day you become a Florida resident, what follows you regardless, and which parts of the plan need a second look before they age.

What Changes in Florida Estate Planning When You Move?

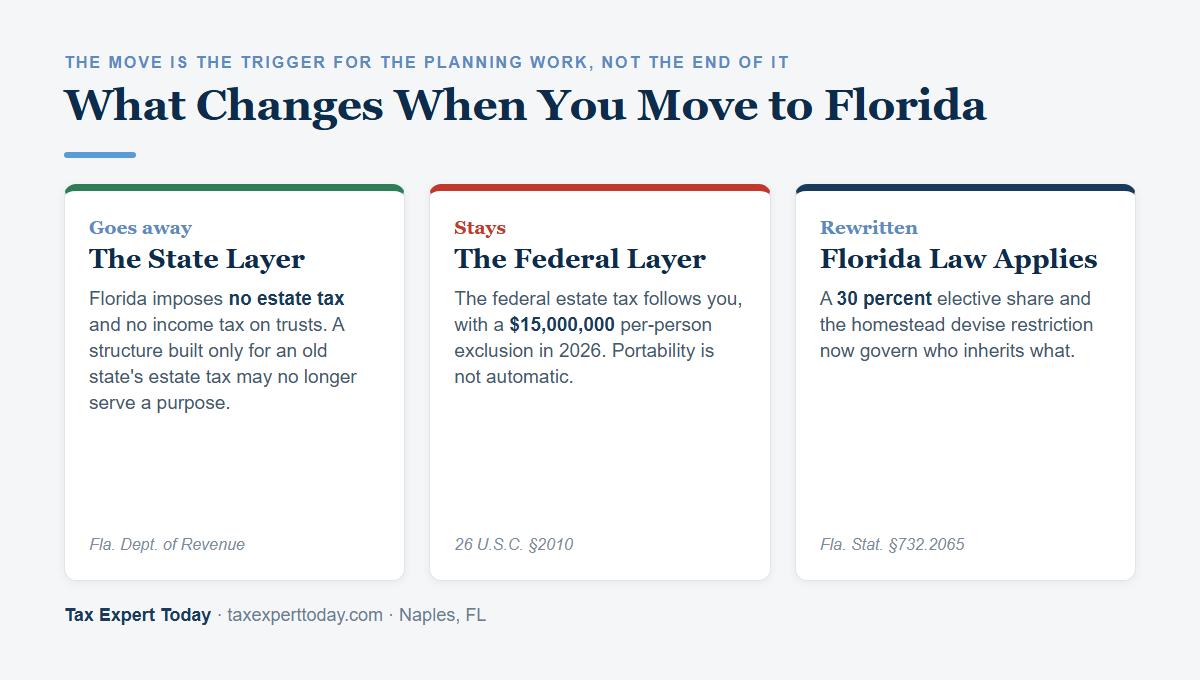

Moving to Florida removes the state layer of estate tax and the state layer of income tax on your trusts, but it does not touch the federal estate tax and it does not automatically rewrite documents drafted under another state’s law. Three things change immediately: your domicile, the law governing your will and trusts, and the property rules that apply to your home.

The mistake worth avoiding is treating the move as the end of the planning work. In practice the move is the trigger for it. A plan built around a state estate tax you no longer owe can be inefficient, and a plan built around another state’s spousal and homestead rules can be invalid or produce a result you did not intend once Florida law applies.

| Planning element | What happens when you become a Florida resident |

|---|---|

| State estate tax | Florida imposes none. Any credit shelter structure built solely to manage an old state’s estate tax may no longer serve a purpose. |

| Federal estate tax | Unchanged. The $15,000,000 per-person basic exclusion for 2026 applies wherever you live. |

| State income tax on trusts | Florida imposes no individual income tax, so a Florida-administered trust generally faces no state-level income tax. |

| Old-state trusts | May remain taxable in the old state depending on that state’s resident-trust rules, regardless of your move. |

| Spousal rights | Florida’s 30 percent elective share replaces your former state’s spousal-protection regime. |

| Your home | Florida homestead law restricts to whom you may leave the property if you are survived by a spouse or a minor child. |

| Property left in the old state | Real property and tangible personal property located there generally stay within that state’s estate tax reach. |

Each of these is examined below. The domicile question sits underneath all of them, because none of the Florida-side benefits attach until Florida is genuinely your domicile. If you have not yet made the move, start with our guide on how to establish Florida residency and the Florida 183-day rule calculator.

The terms that recur below:

- Domicile

- Your true, fixed, permanent home, and the place you intend to return to. It is the anchor for the whole plan, because it decides where your intangible property is taxed at death.

- Basic exclusion amount

- The amount that passes free of federal estate tax, set at $15,000,000 per person for decedents dying in 2026 under 26 U.S.C. §2010(c)(3).

- Portability, or the DSUE amount

- The deceased spousal unused exclusion, which allows a surviving spouse to use what the first spouse did not. It applies only if the first spouse’s estate elects it on a filed Form 706.

- Elective estate

- The broad pool Florida measures the 30 percent spousal elective share against. It reaches beyond probate assets to items such as revocable trust property and certain lifetime transfers.

- Resident trust

- A trust that a state treats as its own for income tax purposes, often based on the trustee, the beneficiaries, or where the trust was created, rather than on where the grantor now lives.

Does Florida Have an Estate Tax in 2026?

No. Florida imposes no estate tax and no inheritance tax. The Florida Department of Revenue states that a federal change eliminated Florida’s estate tax for people who died after December 31, 2004, and since July 1, 2023 personal representatives no longer file an Affidavit of No Florida Estate Tax Due. Florida’s estate tax was a pickup tax tied to a federal credit that Congress phased out, so when the credit disappeared, so did the tax.

The federal estate tax is a separate matter and it follows you to Florida. Under 26 U.S.C. §2010(c)(3), as amended by Public Law 119-21, the basic exclusion amount is $15,000,000 for decedents dying after December 31, 2025, with inflation indexing resuming for years after 2026 using calendar year 2025 as the base. A married couple who preserve both exclusions can therefore shelter $30,000,000 in 2026.

Preserving the second exclusion is not automatic. Portability under §2010(c)(5)(A) requires the first spouse’s estate to elect it on a filed Form 706, even when no tax is due and no return would otherwise be required. When that election is missed, Rev. Proc. 2022-32 provides a simplified path: an estate with no filing requirement under §6018(a) may file a complete Form 706 on or before the fifth anniversary of the date of death, with a statement at the top of the return that it is filed pursuant to that revenue procedure. Whether relief applies depends on the estate’s specific facts.

Can Your Former State Still Tax Your Estate After You Move?

Yes, in part. A state that imposes an estate tax generally reaches the real property and tangible personal property physically located within its borders, even when the owner died domiciled elsewhere. Intangible property such as publicly traded stock, bonds, and bank accounts generally follows your domicile, so it moves with you to Florida. The result is that the vacation house or the boat you kept up north can remain exposed long after you have become a Floridian.

| What you own | Typical old-state estate tax reach after you become a Florida resident |

|---|---|

| Real property still located in the old state | Generally remains within that state’s estate tax base as nonresident property. |

| Tangible personal property kept there, such as vehicles, boats, art, or furnishings | Generally remains within that state’s estate tax base if it has an actual location there. |

| Publicly traded stock, bonds, and bank accounts | Generally sourced to domicile, so it follows you to Florida and escapes the old state’s estate tax. |

| An interest in an operating business located in the old state | Depends on entity form and on that state’s sourcing rules; an interest in an entity is often intangible, but the analysis is fact-specific. |

New York illustrates the mechanics well and it is a common origin state for Southwest Florida arrivals. New York requires the estate of a nonresident to file when the estate includes real or tangible property located in New York State and the federal gross estate plus includible gifts exceeds the basic exclusion amount, which is $7,350,000 for dates of death in 2026. New York also applies a cliff rather than a graduated phase-out. Under New York Tax Law §952(c), no credit is allowed to the estate of a decedent whose New York taxable estate exceeds 105 percent of the basic exclusion amount.

| New York estate tax, 2026 figures | Amount |

|---|---|

| Basic exclusion amount for dates of death in 2026 | $7,350,000 |

| Cliff threshold, being 105 percent of the exclusion | $7,717,500 |

| Consequence of exceeding the cliff | The credit is lost entirely and the estate is taxed from the first dollar. |

The cliff is why the composition of what you leave behind matters as much as the fact of the move. An estate positioned just over the threshold loses the benefit of the exclusion completely rather than losing it gradually. Where a northern property is retained, the ownership form, the value, and the timing of any sale all become planning variables. The sourcing analysis that applies to a sale is covered in our guide on moving to Florida before selling a business, and the same domicile evidence that protects an income tax position also supports the estate tax position.

What Happens to a Trust Created in Your Old State?

A trust does not automatically become a Florida trust because the person who created it moved to Florida. Each state applies its own resident-trust test, and several of them look to factors that your move does not change, such as where the trust was created, where the grantor lived when it became irrevocable, who serves as trustee, or where the beneficiaries live. The trust can therefore keep paying state income tax in the old state while you pay none in Florida.

California is the most aggressive example. Under California Revenue and Taxation Code §17742, the entire taxable income of a trust is subject to California tax if the fiduciary or a noncontingent beneficiary is a California resident. The residence of the person who created the trust is not the test. A Florida retiree whose trust has a California trustee, or a California child as a noncontingent beneficiary, may find the trust still filing in California.

New York applies a different structure. A trust is generally a New York resident trust if the grantor was domiciled in New York when the trust became irrevocable, which is a status the grantor’s later move cannot undo, although a statutory exception can exempt such a trust from New York tax when the trustees, the assets, and the source of income are all outside New York. The details are technical and the conditions are strict.

The practical response is a review rather than an assumption. Depending on the facts, the options may include changing the trustee, moving the administration of the trust, decanting into a new Florida trust where state law and the trust terms allow it, or simply accepting the old-state filing where the trust cannot be moved cleanly. Each option carries its own tax and legal consequences and each should be evaluated with counsel before anything is signed. Our estate and trust planning team coordinates the tax analysis with the drafting attorney.

How Does the Florida Elective Share Change Your Plan?

Florida law entitles a surviving spouse to a fixed share of the estate that a will cannot cut off. Florida Statutes §732.2065 provides that the elective share is an amount equal to 30 percent of the elective estate. The elective estate is broad. It reaches well beyond probate assets to include items such as revocable trust property, certain joint accounts, and certain transfers made during life, which means a plan cannot defeat the share simply by avoiding probate.

This matters most in two situations. The first is a second marriage where the plan was built to direct assets to children from a prior marriage. A structure that worked under the old state’s rules may now collide with a 30 percent claim. The second is where a prenuptial or postnuptial agreement was drafted under another state’s law. Florida allows a spouse to waive the elective share, but the waiver must satisfy Florida’s requirements, and an agreement drafted elsewhere should be reviewed rather than assumed to carry over.

Why Does Florida Restrict Who Inherits Your Homestead?

Florida homestead law is best known as a creditor shield, but it also restricts inheritance, and this catches new residents by surprise. Article X §4(c) of the Florida Constitution provides that the homestead shall not be subject to devise if the owner is survived by a spouse or a minor child, except that the homestead may be devised to the owner’s spouse if there is no minor child. In plain terms, if you are survived by a minor child, you cannot leave your Florida home to whomever you choose.

When a devise violates the restriction, the property does not pass under the will. It passes under Florida Statutes §732.401 instead, which generally gives the surviving spouse a life estate with the remainder to the descendants, or allows the spouse to elect a one-half interest as a tenant in common within the statutory election period. Either outcome can be very different from the plan on paper, and a home left in trust without accounting for the restriction can produce a result no one intended.

The creditor-shield side of homestead has its own timing rules for people who have just arrived, including a federal bankruptcy cap on a recently acquired homestead. Those rules are covered in our guide on Florida asset protection for new residents.

What Happens to Community Property When You Move to Florida?

Couples arriving from a community property state such as California, Texas, Washington, Arizona, or Nevada are giving up a meaningful federal income tax benefit unless they plan for it. Under 26 U.S.C. §1014(b)(6), when one spouse dies, community property receives a new basis for both halves, not just the half owned by the deceased spouse. Florida is not a community property state, so ordinary joint ownership here produces a new basis on only the decedent’s half.

On long-held, highly appreciated assets that difference can be substantial for the surviving spouse who later sells. Florida responded with the Florida Community Property Trust Act. Florida Statutes §736.1503 allows spouses to create a qualifying community property trust, which requires an express declaration that it is a community property trust, at least one qualified trustee, execution by both spouses with the required formalities, and a specific capital-letter warning at the beginning of the agreement.

That warning exists for a reason. The statute itself advises that the consequences may be very extensive, including effects on rights with respect to creditors, and that each spouse should seek competent and independent legal advice. Converting separate property into community property changes what happens on divorce and can change creditor exposure, so the basis benefit is only one side of the ledger. Whether the trade is worth making depends entirely on the couple’s assets, their marriage, and their risk tolerance, and it should be evaluated with an attorney before execution.

Which Estate Planning Documents Should New Florida Residents Update?

Most out-of-state wills and trusts remain valid in Florida if they were validly executed where they were signed, so the usual answer is that documents need review rather than wholesale replacement. The exceptions matter, though, and a few document types genuinely do not travel well.

| Document | Why it needs attention after the move |

|---|---|

| Will | Generally still valid if validly executed elsewhere, but a will that is not self-proved under Florida law can complicate probate. Florida also does not permit a nonresident to serve as personal representative unless the person is a relative within the statutory categories. |

| Revocable trust | Review the governing-law and situs provisions, the trustee, and any credit shelter formula built around an old state’s estate tax exemption. |

| Durable power of attorney | Florida has specific execution and enumeration requirements. Out-of-state forms are frequently questioned or refused by Florida financial institutions. |

| Health care documents | Florida uses its own designation of health care surrogate and living will forms. Replacing these is inexpensive and avoids an argument at the worst possible moment. |

| Deed to the Florida home | Confirm the ownership form, whether tenancy by the entirety applies, and whether the homestead devise restriction defeats the intended disposition. |

| Beneficiary designations | Retirement accounts and life insurance pass outside the will. They are the most commonly overlooked item and the easiest to fix. |

| Declaration of domicile | Filing under Florida Statutes §222.17 is one piece of the evidence that Florida is your domicile, which underpins the entire plan. |

The through-line is domicile. Every Florida-side benefit described in this guide depends on Florida being your actual domicile, and an old state that disagrees can challenge that position. The evidence that supports a residency position is the same evidence that supports the estate plan, which is why the two should be built together rather than separately. See our guides on the dual-state residency trap, surviving a Florida residency audit, and establishing Florida domicile for executives.

Florida Estate Planning Help in Naples and Southwest Florida

Tax Expert Today LLC works with new and prospective Florida residents in Naples, Bonita Springs, Fort Myers, Marco Island, and across Southwest Florida on the tax side of a relocation plan: the federal estate tax exposure, the portability election, the old-state trust question, and the domicile evidence that supports all of it. The firm is multidisciplinary, with tax advisors, enrolled agents, CPAs, and attorneys, and advises clients in residency, tax, and planning matters nationwide. We coordinate with your estate planning attorney on drafting and execution, since Florida homestead, elective share, and community property trust documents require Florida counsel.

The office is at 11983 Tamiami Trail N, Naples, FL 34110, and consultations can be arranged at (239) 441-2005, Monday through Friday, 10:00am to 5:00pm ET. You can also review our Naples tax planning and Florida tax services pages, or contact us directly.

Frequently Asked Questions

Does Florida have an estate tax or an inheritance tax in 2026?

No. Florida imposes neither. The Florida Department of Revenue confirms that a federal change eliminated Florida’s estate tax for people who died after December 31, 2004, and since July 1, 2023 no Affidavit of No Florida Estate Tax Due is filed. The federal estate tax still applies wherever you live, with a $15,000,000 per-person basic exclusion for decedents dying in 2026 under 26 U.S.C. section 2010(c)(3).

Can my old state still tax my estate after I move to Florida?

Partly. A state that imposes an estate tax generally reaches real property and tangible personal property physically located there, even for a decedent domiciled elsewhere. Intangibles such as stock and bank accounts generally follow your domicile to Florida. New York, for example, requires a nonresident estate to file when it includes New York real or tangible property and the federal gross estate plus includible gifts exceeds the 2026 exclusion of $7,350,000.

Do I need a new will when I move to Florida?

Not always. A will validly executed in another state is generally valid in Florida, so the usual step is a review rather than a replacement. That said, a will that is not self-proved under Florida law can complicate probate, Florida restricts who may serve as a nonresident personal representative, and powers of attorney and health care documents often need to be replaced with Florida forms. Whether a new will is warranted depends on your documents and your facts.

Will my out-of-state trust stop paying state income tax once I move?

Not necessarily. Each state applies its own resident-trust test and your move may not change the answer. California taxes the entire income of a trust if the fiduciary or a noncontingent beneficiary is a California resident under Revenue and Taxation Code section 17742. New York generally treats a trust as a resident trust if the grantor was domiciled there when it became irrevocable, subject to a narrow statutory exception. A trust review is the only way to know.

Where can I get help with Florida estate planning in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps new and prospective Florida residents across Naples and Southwest Florida coordinate the tax side of an estate plan, including federal estate tax exposure, the portability election, old-state trust and estate tax reach, and the domicile evidence that supports the plan. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and works alongside your estate planning attorney on Florida drafting. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional on Florida Estate Planning

Florida estate planning rewards an early review rather than a late correction. The situations that most often justify professional help are a taxable estate approaching the federal exclusion, a trust created in a state with an aggressive resident-trust rule, a second marriage where the elective share can override the plan, a homestead with a surviving spouse or a minor child in the picture, a couple arriving from a community property state, and real property retained in a state that imposes its own estate tax. Any one of these can turn a plan that reads correctly on paper into an outcome the family did not expect.

Outcomes depend on individual facts, and nothing in this guide is a promise about how any particular estate will be taxed or administered. Tax Expert Today LLC provides the tax analysis and coordinates with your estate planning attorney, who handles Florida drafting and execution. If you have moved to Florida recently, or you intend to, a review before the documents age is the least expensive version of this work. Call (239) 441-2005 or contact us to arrange a consultation.

Published July 15, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005