By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: A cash balance plan is an IRS-qualified defined benefit retirement plan that lets a high-income business owner contribute far more than a 401(k) allows, often well into six figures per year, with the contribution deducted by the business. The maximum is actuarially determined by age, compensation, and the Internal Revenue Code Section 415(b) annual benefit limit, which rises to $290,000 for 2026. Amounts and eligibility depend on individual facts.

What is a cash balance plan?

A cash balance plan is a qualified defined benefit pension plan that expresses each participant’s benefit as a hypothetical account balance rather than a monthly pension at retirement. Each year the account receives a pay credit, often a percentage of compensation or a flat dollar amount, plus an interest credit set by the plan document. The plan is governed by IRC Section 401(a) and the accrued benefit rules of IRC Section 411.

Because it is a defined benefit plan, an actuary certifies the funding each year and the business, not the employee, bears the investment risk. The IRS describes cash balance plans as a form of defined benefit plan that looks and feels like a defined contribution account to the participant. See the IRS Defined Benefit Plan overview.

How much can a business owner contribute to a cash balance plan in 2026?

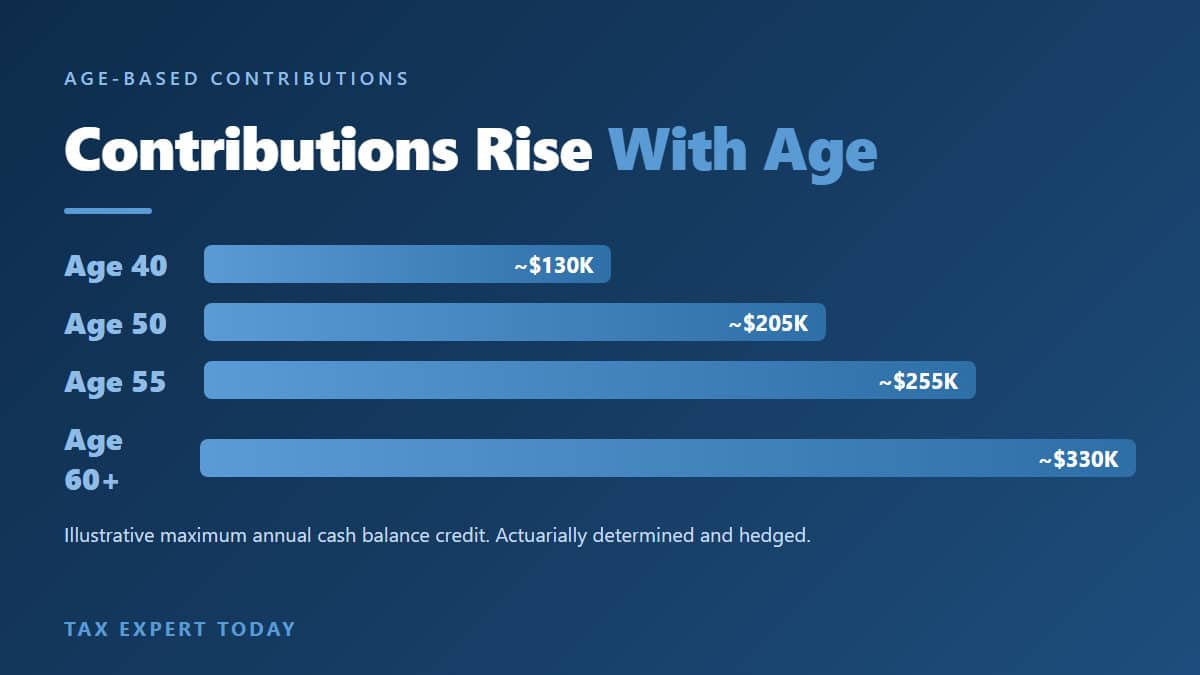

The contribution is actuarially determined, so it is not a single published number the way a 401(k) limit is. It is calculated so the hypothetical account can grow to fund the maximum lifetime benefit allowed under IRC Section 415(b), which is $290,000 of annual benefit for 2026. In practice the allowable annual contribution rises steeply with age, because an older owner has fewer years to fund the same target benefit.

The table below shows illustrative maximum annual pay credits by age. These figures are approximate, are actuarially determined, and depend on compensation, plan design, the plan’s interest crediting rate, and IRS assumptions. They are shown to illustrate the mechanism, not to promise a result.

| Owner age | Illustrative maximum annual cash balance credit (2026) |

|---|---|

| 40 | Approximately $110,000 to $150,000 |

| 45 | Approximately $140,000 to $185,000 |

| 50 | Approximately $180,000 to $235,000 |

| 55 | Approximately $225,000 to $290,000 |

| 60 | Approximately $275,000 to $335,000 |

| 62 to 65 | Approximately $300,000 to $360,000 |

Illustrative only. Actual amounts are certified by an enrolled actuary each year and vary with the facts of the plan. The maximum lump sum a cash balance account can hold at retirement is likewise capped by the Section 415(b) limit.

Who is a cash balance plan best suited for?

A cash balance plan generally fits a profitable business owner or professional practice with strong, stable cash flow, an owner who is typically age 40 or older, and relatively few non owner employees. The strategy tends to work best when the owner wants to contribute more than the 401(k) and profit sharing limits permit and can commit to funding the plan for several years, since a defined benefit plan is intended to be a durable commitment rather than a one year move.

- High income owners of professional practices, such as medical, dental, legal, and consulting firms.

- Owners age 40 and above who are behind on retirement savings and want to catch up quickly.

- Businesses with consistent profits that can support the required annual funding.

- Owner heavy or spouse only businesses, where the owner captures most of the contribution.

Because the plan must satisfy nondiscrimination testing under IRC Section 401(a)(4), a business with many rank and file employees may need to provide meaningful staff contributions, which changes the cost benefit analysis. Whether the plan makes sense depends on the specific census and facts.

How does a cash balance plan work with a 401(k) and profit sharing?

Cash balance plans are most powerful when paired with a 401(k) and profit sharing plan. The defined contribution plan captures the elective deferral and a profit sharing allocation, while the cash balance plan layers a much larger age based contribution on top. When the two plans are combined, the deduction is governed by the combined limit rules of IRC Section 404(a)(7), and the deductible profit sharing contribution may be limited to 6 percent of compensation for the covered group.

For 2026, the relevant defined contribution figures are the $24,500 elective deferral limit, the $8,000 age 50 and over catch up, and the $72,000 overall defined contribution limit under IRC Section 415(c). Compensation counted for plan purposes is capped at $360,000 under IRC Section 401(a)(17).

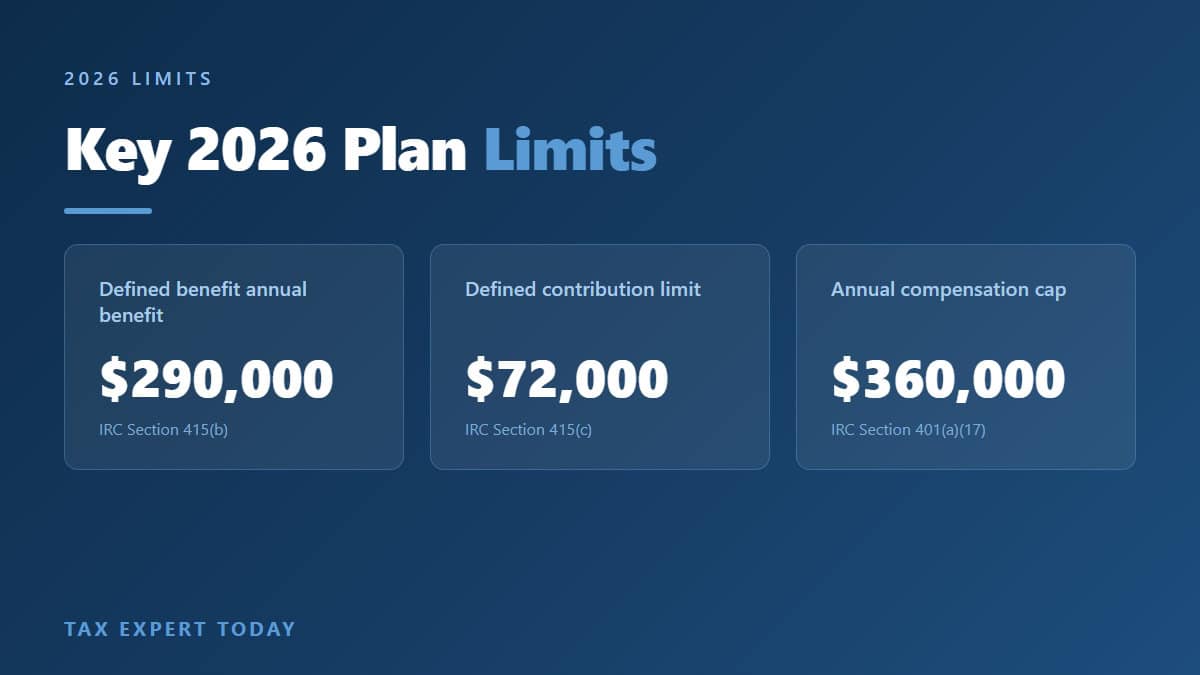

What are the 2026 contribution and benefit limits?

The limits that shape a cash balance and 401(k) design come from IRC Section 415 and are adjusted for inflation each year. The current figures are published in the IRS cost of living adjustment tables and the 2026 IRS announcement.

| 2026 limit | Amount | 2025 |

|---|---|---|

| Defined benefit annual benefit limit, Section 415(b) | $290,000 | $280,000 |

| Defined contribution limit, Section 415(c) | $72,000 | $70,000 |

| Annual compensation limit, Section 401(a)(17) | $360,000 | $350,000 |

| 401(k) elective deferral | $24,500 | $23,500 |

| Catch up, age 50 and over | $8,000 | $7,500 |

| Catch up, ages 60 to 63 | $11,250 | $11,250 |

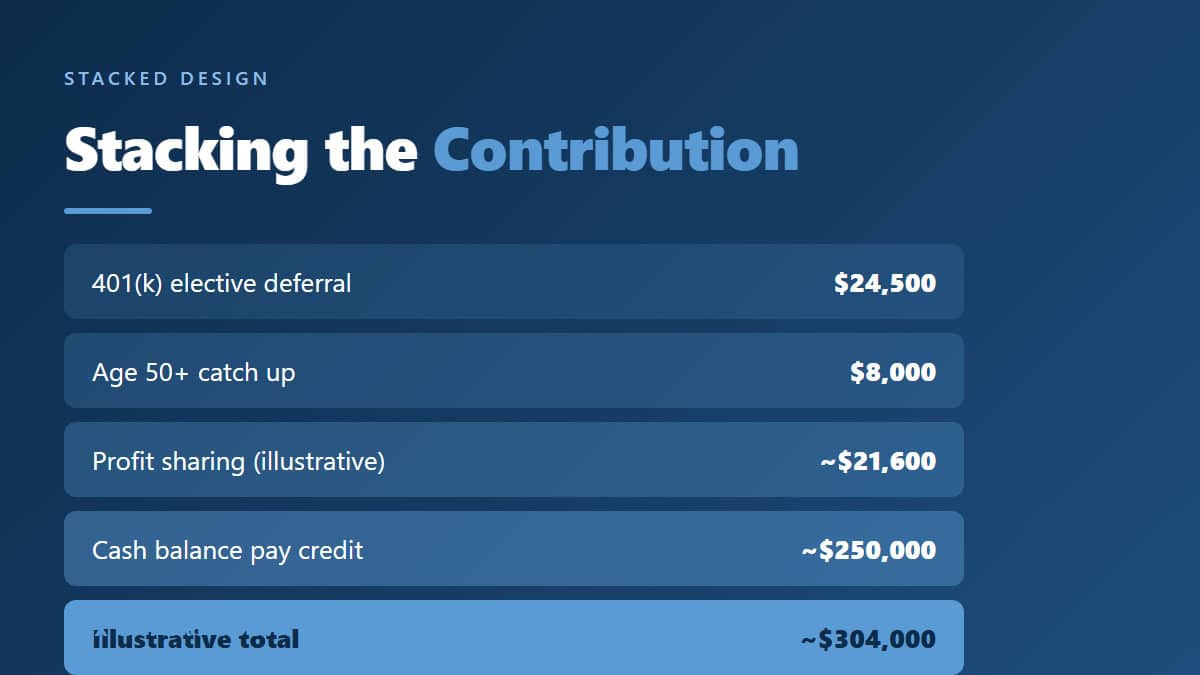

What is a worked example of the stacked contribution?

Consider a hypothetical owner, age 55, whose plan compensation reaches the $360,000 cap and whose business has strong, consistent profits. The figures below illustrate how the defined contribution and defined benefit pieces can stack. This is a mechanism illustration, not a prediction. Actual numbers depend on the actuarial certification, the plan design, and nondiscrimination testing.

| Component | Illustrative 2026 amount |

|---|---|

| 401(k) elective deferral | $24,500 |

| Age 50 and over catch up | $8,000 |

| Employer profit sharing (subject to the 6 percent combined limit) | Approximately $21,600 |

| Cash balance pay credit (actuarially determined) | Approximately $250,000 |

| Illustrative total tax deductible contribution | Approximately $304,000 |

The full contribution is generally deductible by the business under IRC Section 404, subject to the combined plan limits, and the earnings grow tax deferred until distribution. Whether this level of funding is appropriate depends on cash flow, the employee census, and long term goals.

What are the tax benefits and the deduction rules?

The core benefit is a large current year deduction. Employer contributions to a qualified cash balance plan are deductible under IRC Section 404, the assets grow tax deferred, and the participant is taxed only when the benefit is distributed, typically in retirement when the marginal rate may be lower. At separation or plan termination the balance can generally be rolled into an IRA, which preserves the deferral.

For an owner in a high marginal bracket, moving a large, otherwise taxable amount of business income into a deductible plan contribution can meaningfully reduce current taxable income. The deduction is not a permanent exclusion, it is a deferral, so the planning value comes from the rate difference between the contribution year and the distribution years, plus years of tax deferred compounding.

What is the deadline to adopt a cash balance plan for 2026?

Since the SECURE Act, a business can adopt a new qualified retirement plan as late as the due date of its tax return for the year, including extensions, and treat the plan as adopted for that year under IRC Section 401(b)(2). For a calendar year S corporation on extension, that can push the 2026 adoption decision into September 2027, which makes the strategy one of the few large deductions still available after the year has closed.

Waiting is still not free. The actuary needs time to design the benefit formula and run nondiscrimination testing, funding must be deposited by the plan’s funding deadline, and a plan adopted retroactively cannot accept elective 401(k) deferrals for the closed year. Owners who expect a strong year are usually better served by designing the plan during the year it will first apply.

Can a cash balance plan be combined with a Solo 401(k)?

Yes. An owner-only business can pair a one-participant 401(k) with a cash balance plan, and that combination produces the largest deductible contributions available to a self-employed owner. Elective deferrals remain fully allowed alongside the defined benefit funding.

One coordination rule matters: when an employer maintains both a defined benefit and a defined contribution plan, the combined deduction limits of IRC Section 404(a)(7) generally cap the deductible employer profit sharing contribution at 6 percent of compensation. Plan designs in this situation typically pair the full cash balance credit with the elective deferral and a 6 percent profit sharing layer, which is the structure shown in the worked example above. An actuary runs these limits each year, because exceeding them creates a nondeductible contribution subject to excise tax.

What are the risks and downsides?

A cash balance plan is a commitment, not a one year election. The main considerations are below.

- Required funding. Because it is a defined benefit plan, the annual contribution is largely mandatory once the plan year is set. A business with volatile cash flow may struggle in a down year.

- Employee cost. Nondiscrimination testing under IRC Section 401(a)(4) may require meaningful contributions for staff, which raises the total cost.

- Administrative complexity. The plan needs an enrolled actuary, annual Form 5500 filing, and a Schedule SB actuarial certification.

- Investment risk on the business. If plan investments underperform the interest crediting rate, the business must make up the shortfall.

These factors are manageable with proper design, but they are the reason a cash balance plan calls for coordinated actuarial, tax, and investment advice rather than a do it yourself setup.

Cash Balance Plan Help in Naples and Southwest Florida

Tax Expert Today LLC advises business owners and professional practice owners in Naples and across Southwest Florida on cash balance and combined plan design, coordinating the tax planning with the actuarial and investment work. As a multidisciplinary firm, we integrate the retirement plan decision with entity structure, compensation planning, and the owner’s broader tax picture rather than treating it as a standalone product. Our office is at 11983 Tamiami Trail N, Naples, FL 34110, and you can reach us at (239) 441-2005, Monday through Friday, 10am to 5pm ET. We serve clients in all 50 states, with a concentration in Florida, California, Texas, and Georgia. Learn more on our Naples tax planning page.

When to Engage a Professional

A cash balance plan can move a large amount of income into a deductible, tax deferred vehicle, but the design, funding commitment, and employee testing require professional coordination. If you are a business owner or practice owner with strong profits who wants to contribute well beyond 401(k) limits, a conversation with a qualified advisor can help you decide whether the strategy fits your facts. Tax Expert Today LLC, led by Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA, provides tax planning and business advisory services and works alongside actuaries and investment professionals on plan design. Explore our tax planning services or call (239) 441-2005 to discuss your situation. Outcomes depend on individual circumstances.

Frequently Asked Questions

How much can I contribute to a cash balance plan?

The contribution is actuarially determined by age, compensation, and plan design, and it is capped so the account funds no more than the Section 415(b) annual benefit limit, which is $290,000 for 2026. Older owners can generally contribute more because they have fewer years to fund the benefit. Amounts depend on individual facts.

Can I have a cash balance plan and a 401(k) at the same time?

Yes. Cash balance plans are commonly paired with a 401(k) and profit sharing plan so the owner can capture the elective deferral, a profit sharing allocation, and a large age based cash balance credit. When combined, the deduction is subject to the combined plan rules of IRC Section 404(a)(7).

Is a cash balance plan contribution tax deductible?

Employer contributions to a qualified cash balance plan are generally deductible by the business under IRC Section 404, and the assets grow tax deferred until distribution. The benefit is a deferral of tax, not a permanent exclusion, so the value depends on the rate difference between the funding year and the distribution years.

What are the downsides of a cash balance plan?

The main considerations are the largely mandatory annual funding, potential contribution costs for staff under nondiscrimination testing, administrative requirements such as an enrolled actuary and Form 5500, and investment risk that falls on the business if returns lag the interest crediting rate. It suits owners with stable, strong cash flow.

Where can I get help with a cash balance plan in Naples, FL?

Tax Expert Today LLC in Naples, Florida advises business owners on cash balance and combined plan design as part of an integrated tax planning approach, coordinating with actuaries and investment professionals. The office is at 11983 Tamiami Trail N, Naples, FL 34110, reachable at (239) 441-2005. The firm serves clients across all 50 states.

Published July 12, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005