By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: Florida asset protection is one of the strongest creditor shields in the country, built on three pillars: an unlimited-value homestead exemption from forced sale, tenancy by the entirety for married couples, and statutory exemptions for wages, life insurance, annuities, and retirement accounts. For someone who has just moved to Florida, the protection is real but not instant. A federal bankruptcy rule caps a recently acquired homestead at $214,000 for the first 1,215 days, and the state whose exemptions apply is set by where you were domiciled during the prior two years, so documenting the move matters as much as making it.

Published: July 2026

People move to Florida for the weather and the absence of a state income tax, but many high earners and business owners also move for a second reason that gets less attention: Florida offers some of the most protective creditor and asset-shield law in the United States. A homestead here cannot be forced into sale by most creditors, a married couple can hold property in a form that a single spouse’s creditors cannot touch, and wages, life insurance, annuities, and retirement accounts each carry their own statutory shield. The catch for a new resident is timing. Several of these protections turn on how long you have owned the home or how long you have been domiciled in Florida, so the day you move is the day the clock starts, not the day the shield is complete. This guide explains how the Florida homestead creditor shield works, how tenancy by the entirety protects a married couple, which other assets are exempt, and what a new resident has to document to make the protection hold.

What Does Florida Asset Protection Cover for New Residents?

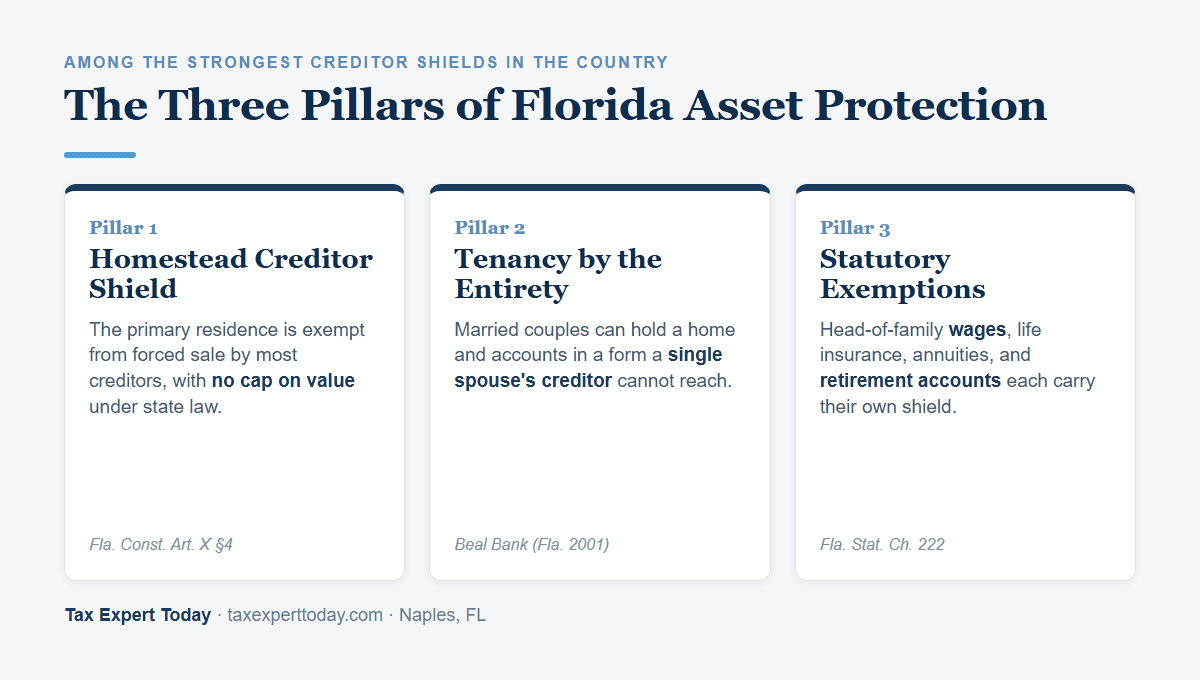

Florida asset protection covers the primary residence through an unlimited-value homestead exemption from forced sale, jointly held marital property through tenancy by the entirety, and a set of statutory exemptions for wages, life insurance, annuities, and retirement accounts. Together these shield a large share of a typical household balance sheet from most creditors, though each protection has its own conditions, and a new resident faces added timing rules that a long-time Floridian does not.

The point that surprises many newcomers is that these shields are creditor protections, not tax breaks. The homestead creditor shield in Article X §4 of the Florida Constitution is separate from the property-tax homestead exemption. The property-tax exemption removes up to $50,000 of assessed value from the tax roll and caps annual assessment growth under the Save Our Homes provision, and it is worth claiming, but it is a modest dollar benefit and is not the reason Florida is known for asset protection. This article focuses on the creditor shield and the domicile evidence that supports it, because that is the planning conversation that actually moves the needle for a relocating business owner or professional.

How Does the Florida Homestead Creditor Shield Work?

The Florida homestead creditor shield protects an unlimited dollar value of your primary residence from forced sale by most creditors. Unlike the homestead laws of nearly every other state, Florida sets no cap on the protected value under state law. The limit is on land area, not dollars: the exemption covers up to one-half acre of contiguous land inside a municipality, or up to 160 acres outside a municipality, under Article X §4(a)(1) of the Florida Constitution.

The protection is broad but not absolute. Article X §4 itself carves out three categories of obligation that can still reach the home, so a homestead does not shield you from a debt in any of these classes.

- Taxes and assessments

- Property taxes and government assessments on the homestead remain enforceable, and an unpaid federal tax lien can also attach.

- Obligations to buy, improve, or repair the home

- A purchase-money mortgage, a home equity loan, and a construction or mechanic’s lien for work on the property are all enforceable against the homestead.

- Obligations for labor on the property

- A debt contracted for house, field, or other labor performed on the homestead can be enforced against it.

Outside those three classes, a general creditor, including one holding a money judgment from a lawsuit, generally cannot force the sale of a Florida homestead. That is the feature that draws relocating professionals, physicians, and business owners who face liability exposure. The homestead protection is a shield against forced sale, not a promise that no lien can ever exist, and how the home is titled and devised carries separate estate-planning consequences discussed later in this guide.

Those devise consequences are the estate-planning side of the same homestead. Florida restricts who may inherit the home when the owner is survived by a spouse or a minor child, and the spousal elective share reaches well beyond probate assets. Our guide on Florida estate planning for new residents covers both, along with the old-state trust and estate tax questions a recent arrival should review.

Does the Homestead Shield Protect a New Resident Right Away?

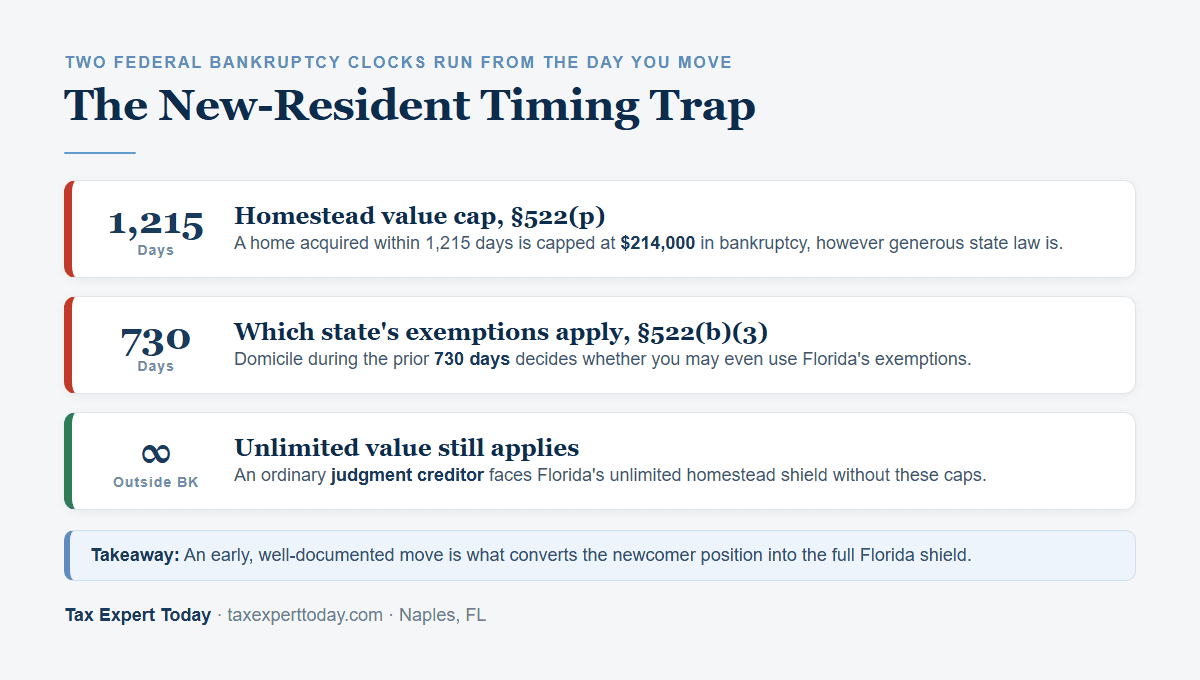

Not fully. In bankruptcy, a homestead you acquired within 1,215 days, roughly three years and four months, before filing is capped at $214,000 of protected value under 11 U.S.C. §522(p), no matter how generous Florida law is. A separate rule, 11 U.S.C. §522(b)(3), decides which state’s exemptions you may even use, based on where you were domiciled during the 730 days before filing. So a very recent arrival can be forced to use the prior state’s exemption scheme, and a recent home purchase can be capped, even in Florida.

This is the core reason the phrase “for new residents” matters. The unlimited homestead value that Florida is famous for applies with full force to a long-time resident, but a newcomer sits under two federal timing rules until the clock runs. Two points soften this. First, the $214,000 cap and the domicile-selection rule apply in bankruptcy, so they do not govern an ordinary judgment creditor chasing a Florida homestead outside a bankruptcy case, where the state’s unlimited protection still controls. Second, both clocks run from the move and the purchase, so an early, well-documented relocation is what converts the newcomer position into the full Florida shield.

| Rule | What it does to a new resident | When the clock clears |

|---|---|---|

| Homestead value cap, §522(p) | Caps a newly acquired homestead at $214,000 in bankruptcy | 1,215 days after you acquire the home |

| Exemption-selection rule, §522(b)(3) | May require using the former state’s exemptions, not Florida’s | 730 days of Florida domicile before filing |

| State-law forced-sale shield | Protects unlimited homestead value outside bankruptcy | On establishing a Florida homestead |

What Is Tenancy by the Entirety in Florida?

Tenancy by the entirety is a form of joint ownership available only to married couples that treats the spouses as a single legal owner, so property held this way is protected from the creditors of one spouse acting alone. A creditor of only the husband, or only the wife, generally cannot reach an entireties asset, because neither spouse owns a separate, divisible share that a creditor can seize. The protection ends if the couple divorces, if one spouse dies, or if both spouses owe the same joint debt.

Florida is notable for extending tenancy by the entirety beyond real estate to personal property, including bank and brokerage accounts. In Beal Bank, SSB v. Almand and Associates, 780 So. 2d 45 (Fla. 2001), the Florida Supreme Court held that a bank account opened by a married couple is presumed to be held as tenants by the entirety unless the account or the bank’s records show otherwise. For a relocating couple, this means titling a Florida home and the primary marital accounts correctly can shield them from a claim against just one spouse, which is a common exposure for a professional or business owner whose liability is individual. Because the protection depends on precise titling and the marriage, it is a planning step to confirm at the move, not an assumption to make.

Which Other Assets Does Florida Protect?

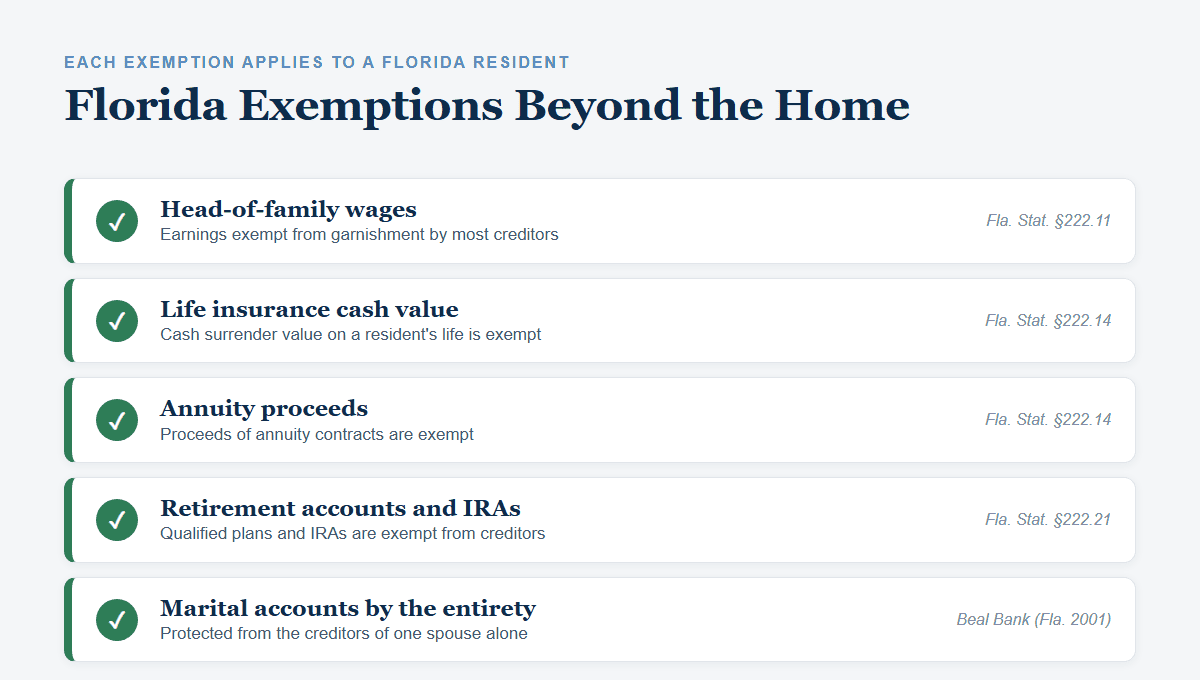

Beyond the home, Florida law exempts several categories of personal property from most creditors: the wages of a head of family, the cash surrender value of life insurance, the proceeds of annuity contracts, and qualified retirement accounts and individual retirement accounts. Each exemption sits in Chapter 222 of the Florida Statutes and applies to a Florida resident, which is another reason establishing domicile carefully is part of the asset-protection plan.

| Asset | Florida authority | Protection |

|---|---|---|

| Wages of a head of family | Fla. Stat. §222.11 | Earnings are exempt from garnishment by most creditors, subject to the statute’s conditions |

| Life insurance cash value | Fla. Stat. §222.14 | Cash surrender value on the life of a Florida resident is exempt from creditors |

| Annuity proceeds | Fla. Stat. §222.14 | Proceeds of annuity contracts issued to a Florida resident are exempt |

| Retirement accounts and IRAs | Fla. Stat. §222.21 | Qualified plans and IRAs are exempt from the claims of creditors |

| Marital accounts and property | Tenancy by the entirety, Beal Bank (Fla. 2001) | Protected from the creditors of one spouse acting alone |

These exemptions are powerful, but they are not a license to shield assets after a claim has already arisen. Florida’s Uniform Voidable Transactions Act at Fla. Stat. §726.105 lets a court unwind a transfer made with the intent to hinder, delay, or defraud a creditor, which means moving money into an exempt form on the eve of a known lawsuit can be reversed. Asset protection works when it is set up in calm weather, well before a claim exists, and when it uses the exemptions the law already provides rather than a last-minute maneuver.

How Do You Document Florida Domicile to Support Asset Protection?

You document Florida domicile the same way you would for income-tax purposes, by making Florida the true center of your life and creating a paper trail that a court or creditor cannot easily dispute. The centerpiece is a Declaration of Domicile under Florida Statutes §222.17, a sworn statement filed with the clerk of court declaring Florida as your permanent home. Around it, the standard steps build the record: a Florida driver license, Florida voter registration, retitling the home and primary accounts in Florida, and moving banking, advisors, and physicians to the state.

Domicile matters for asset protection for two reasons. It starts the 730-day clock under 11 U.S.C. §522(b)(3) that determines whether you may use Florida’s exemptions at all, and the Chapter 222 exemptions for wages, life insurance, annuities, and retirement accounts each apply to a Florida resident. The domicile checklist itself overlaps entirely with the residency planning covered in our guide on how to establish Florida residency, and the evidence a former state tests in a Florida residency audit is the same evidence that supports an exemption claim. A move that also crosses a high-tax state line raises the separate risk of being pulled back as a statutory resident, which we cover in the dual state residency trap.

Relocation timing runs through the firm’s related guides as well, from Florida domicile for executives with equity compensation to moving to Florida before selling a business.

Asset protection also intersects with estate planning, because Article X §4 restricts how a Florida homestead can be devised when the owner is survived by a spouse or a minor child, and because trusts and beneficiary designations govern how exempt assets pass at death. Coordinating the creditor shield with the estate plan is where the two disciplines meet, and it is a core part of our estate and trust planning work.

Florida Asset Protection Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals, professionals, and business owners moving to Naples and across Southwest Florida structure the asset-protection side of a Florida move alongside the income-tax side. That work includes confirming how a homestead is titled and devised, reviewing whether marital accounts qualify for tenancy by the entirety, mapping the 1,215-day and 730-day federal clocks against a planned home purchase and move date, and building the domicile record that supports both the residency position and the Chapter 222 exemptions. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and it serves clients in residency, tax, and planning matters nationwide. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET. You can review the firm’s Naples tax planning and Florida tax services for related help.

Frequently Asked Questions

Does Florida really protect an unlimited home value from creditors?

Under state law, yes, subject to acreage limits and three exceptions. Article X §4 of the Florida Constitution exempts a homestead from forced sale by most creditors with no cap on value, covering up to one-half acre inside a municipality or 160 acres outside one. Taxes and assessments, obligations to buy or improve the home such as a mortgage, and labor liens on the property are the exceptions that can still reach it. In bankruptcy, a separate federal rule caps a home acquired within 1,215 days at $214,000, so a very recent purchase is limited even in Florida.

How long after moving to Florida am I fully protected?

The state-law forced-sale shield applies once you establish a Florida homestead, but two federal bankruptcy clocks affect a newcomer. You generally must be domiciled in Florida for 730 days before a bankruptcy filing to use Florida’s exemptions, and a homestead acquired within 1,215 days before filing is capped at $214,000 in bankruptcy. Outside of bankruptcy, an ordinary judgment creditor faces Florida’s unlimited homestead protection without those caps, so the full picture depends on the type of claim.

What is tenancy by the entirety and who can use it?

Tenancy by the entirety is a joint-ownership form available only to married couples that shields the property from the creditors of one spouse acting alone. Florida applies it to real estate and, under Beal Bank (Fla. 2001), presumes it for a married couple’s bank accounts unless the records show otherwise. The protection ends on divorce or the death of a spouse, and it does not shield the couple from a debt they both owe jointly.

Can I move assets into exempt accounts once I am being sued?

That is risky and often reversible. Florida’s Uniform Voidable Transactions Act at Fla. Stat. §726.105 allows a court to unwind a transfer made with the intent to hinder, delay, or defraud a creditor, so shifting money into an exempt form after a claim arises can be set aside. Asset protection is most effective when it is arranged well before any claim exists, using the exemptions the law already provides.

Where can I get help with Florida asset protection in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, helps new and prospective Florida residents in Naples and across Southwest Florida coordinate the homestead creditor shield, tenancy by the entirety, and the Chapter 222 exemptions with a documented domicile plan. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and advises clients in residency, tax, and planning matters nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional on Florida Asset Protection

If you are relocating to Florida with meaningful liability exposure, a business, or a large home purchase, the asset-protection planning is worth doing before the move rather than after a claim appears. The judgment calls are how to title and devise the homestead, whether marital accounts qualify for tenancy by the entirety, how to sequence a home purchase and the move against the 1,215-day and 730-day federal clocks, and how to coordinate the creditor shield with an estate plan and the Chapter 222 exemptions. Those are the points where preparation changes the result, and where the timing of the move genuinely matters. Tax Expert Today LLC advises relocating clients on the tax and asset-protection sides of a Florida move and works in residency and planning matters nationwide.

Call (239) 441-2005 or schedule a consultation to review your homestead titling, test your accounts for entireties protection, and build a documented Florida move. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 13, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005