By Dr. Pellumb Kabashi, DBA, MBA, EA, CFE, CES

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: The difference in the FBAR vs Form 8938 question comes down to two separate laws and two separate agencies. The FBAR (FinCEN Form 114) is filed with the Financial Crimes Enforcement Network under the Bank Secrecy Act when your foreign financial accounts exceed $10,000 in aggregate at any point in the year. Form 8938 is filed with the IRS as part of your income tax return under FATCA when your specified foreign financial assets exceed a threshold that starts at $50,000 and rises with filing status and foreign residence. They cover overlapping but different assets, carry different penalties, and many taxpayers have to file both. Filing one does not satisfy the other.

Published: July 14, 2026

If you hold money or investments outside the United States, you may have run into two forms that look almost identical from a distance: the FBAR and Form 8938. They both ask about foreign accounts, they both carry steep penalties for getting them wrong, and they are easy to confuse. They are not the same filing, and satisfying one does not excuse the other. This 2026 guide walks through what each one is, who has to file it, the very different dollar thresholds, what happens if you skip it, and how to tell whether you owe one, both, or neither. If you are worried about years you already missed, our guide to FBAR penalties covers the exposure, and the threshold question of whether you need an FBAR at all is covered in do I need to file an FBAR.

What Is the Difference Between the FBAR and Form 8938?

The core difference is legal origin. The FBAR is a Bank Secrecy Act report filed with the Treasury Department’s Financial Crimes Enforcement Network, while Form 8938 is a tax form filed with the IRS under the Foreign Account Tax Compliance Act. Because they come from different statutes, they have different thresholds, different filing mechanics, and different definitions of what counts as a reportable asset. The FBAR is about foreign financial accounts. Form 8938 reaches a broader set of foreign financial assets, including some that are not held in an account at all. One goes to FinCEN electronically; the other is attached to your Form 1040.

A useful way to hold the distinction is to think of the questions each form asks. The FBAR asks where your foreign accounts are, and Form 8938 asks what specified foreign assets you held and what income they produced. The two overlap heavily, because a foreign bank account frequently appears on both, yet they are administered by different parts of the government for different purposes. That is exactly why filing one has no effect on your obligation to file the other.

Who Has to File the FBAR?

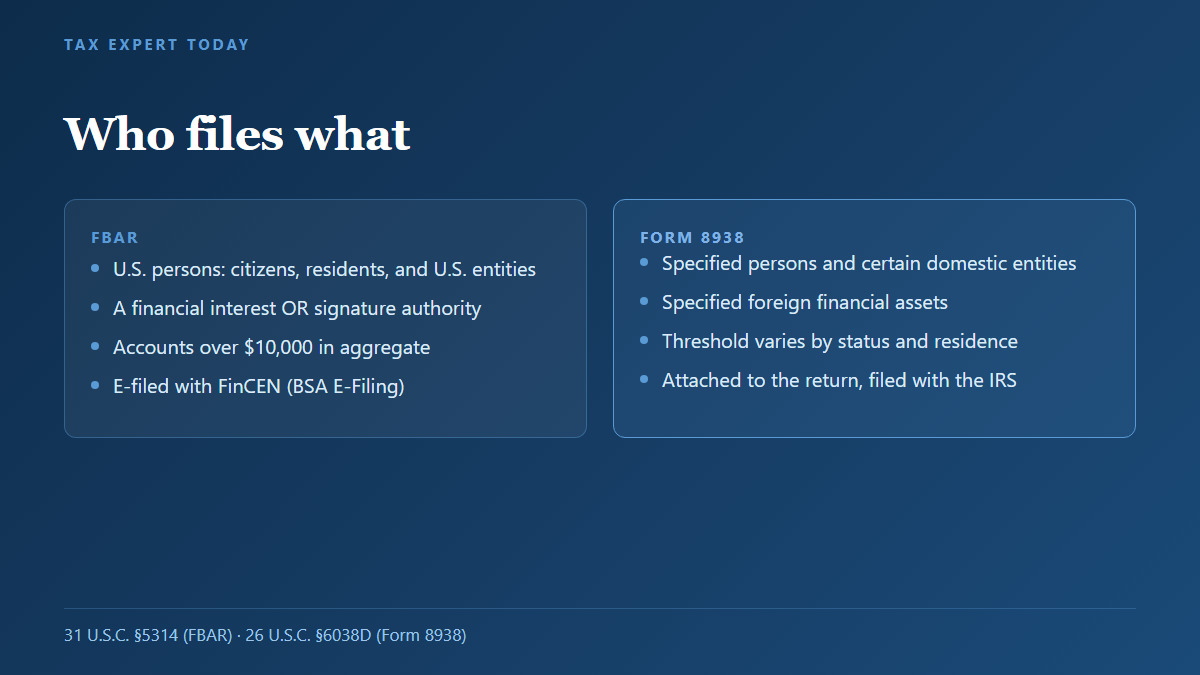

You have to file the FBAR if you are a U.S. person with a financial interest in, or signature authority over, one or more foreign financial accounts whose aggregate value exceeded $10,000 at any time during the calendar year. A U.S. person includes citizens, resident aliens, and entities such as corporations, partnerships, LLCs, trusts, and estates formed under U.S. law. The requirement comes from 31 U.S.C. §5314 and its regulation, 31 CFR 1010.350.

Two features of the FBAR catch people off guard. First, the $10,000 test is an aggregate figure across all of your foreign accounts, not a per-account figure, so five accounts holding $2,500 each trigger the filing even though none of them individually reaches $10,000. Second, signature authority alone can require a filing even when the money is not yours. An employee who can sign on a foreign corporate account, or an adult child on a parent’s overseas account, may have to file. The FBAR is filed electronically with FinCEN through the BSA E-Filing System, separately from your tax return.

Who Has to File Form 8938?

You have to file Form 8938 if you are a specified person whose specified foreign financial assets exceed the reporting threshold for your filing status and residence. Specified persons are individuals, meaning U.S. citizens, resident aliens, and certain nonresident aliens, and, since 2016, certain domestic entities formed or used to hold foreign assets. The obligation comes from 26 U.S.C. §6038D, the FATCA statute enacted in 2010.

Form 8938 is not a standalone filing. It is attached to your annual income tax return and travels with it to the IRS, so you only file it in a year you are already required to file a return. The thresholds are far higher than the FBAR’s $10,000 and, unlike the FBAR, they change depending on whether you live in the United States or abroad and whether you file jointly. That structure means a taxpayer can easily cross the FBAR threshold without coming anywhere near the Form 8938 threshold, which is one of the most common sources of confusion in the FBAR vs Form 8938 comparison.

What Are the Filing Thresholds for the FBAR and Form 8938?

The FBAR threshold is a flat $10,000 aggregate for everyone, while Form 8938 thresholds start at $50,000 and scale up with filing status and foreign residence. The table below shows the current figures drawn directly from the IRS comparison chart. For Form 8938, meeting either the year-end value test or the any-time-during-the-year test triggers the filing.

| Filer situation | FBAR (FinCEN 114) | Form 8938 (FATCA) |

|---|---|---|

| Single or married-separate, living in the U.S. | $10,000 aggregate, any time | More than $50,000 on the last day, or more than $75,000 any time |

| Married filing jointly, living in the U.S. | $10,000 aggregate, any time | More than $100,000 on the last day, or more than $150,000 any time |

| Single or married-separate, living abroad | $10,000 aggregate, any time | More than $200,000 on the last day, or more than $300,000 any time |

| Married filing jointly, living abroad | $10,000 aggregate, any time | More than $400,000 on the last day, or more than $600,000 any time |

The gap between the two thresholds is the practical takeaway. A U.S. resident with a single foreign account holding $30,000 files an FBAR but not a Form 8938. A married couple living abroad with $250,000 in foreign accounts files the FBAR and, because they are under the $400,000 year-end and $600,000 any-time thresholds, may not have to file Form 8938. You cannot assume that crossing one line crosses the other.

What Assets Does Each Form Cover?

The FBAR covers foreign financial accounts, meaning bank accounts, brokerage and securities accounts, mutual funds, and similar accounts held at an institution outside the United States. Form 8938 covers those same accounts and, in addition, a broader category of specified foreign financial assets held for investment that are not inside an account, such as foreign stock or securities held directly, interests in foreign entities, and foreign financial instruments or contracts with a non-U.S. counterparty. That broader reach is why Form 8938 can apply to an investment the FBAR never touches.

Neither form reaches everything abroad. Directly held foreign real estate is not reportable on either form, although rental income is taxable and an account that holds real estate may be reportable. Physical assets held directly, such as a foreign vacation home, gold coins in a foreign safe deposit box, or foreign currency in your hand, are generally outside both forms. The distinction turns on whether the asset is a financial account or a specified financial asset, not simply on whether it sits overseas, and that is a place where careful classification matters.

Do I Have to File Both the FBAR and Form 8938?

Yes, many taxpayers have to file both, and filing one never substitutes for the other. If your foreign accounts exceed $10,000 in aggregate you file the FBAR with FinCEN, and if your specified foreign financial assets also exceed the Form 8938 threshold for your situation you additionally file Form 8938 with your tax return. The same foreign bank account can appear on both forms in the same year, and that duplication is expected rather than a mistake.

It is equally possible to owe only one. A person with $30,000 in a single foreign account files the FBAR alone. A person whose only foreign asset is directly held foreign stock worth $80,000, held outside any account, may owe Form 8938 but not the FBAR, because that asset is not a financial account. Working through both tests separately, rather than assuming they move together, is the reliable way to get the FBAR vs Form 8938 answer right for a given year.

What Are the Penalties for Not Filing Each One?

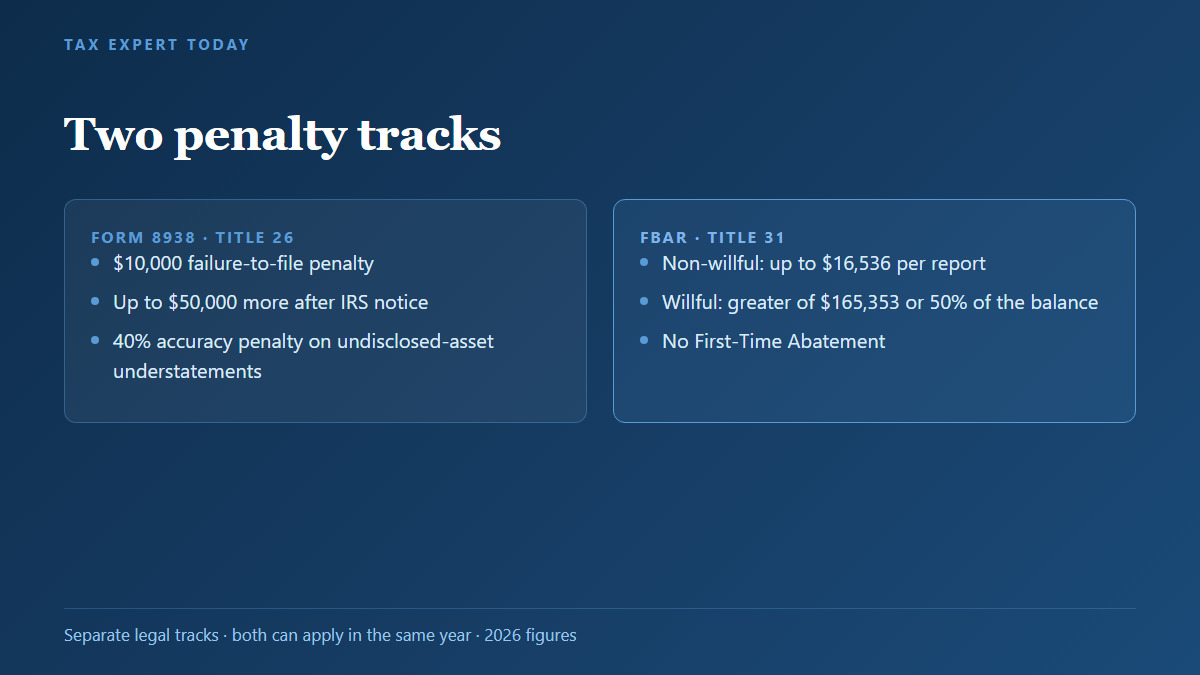

Form 8938 carries a failure-to-file penalty of $10,000, plus up to an additional $10,000 for each 30-day period the failure continues after the IRS mails a notice, capped at $50,000, along with a 40% accuracy-related penalty under IRC §6662(j) on any understatement tied to an undisclosed asset. The FBAR penalties run on a separate Bank Secrecy Act track. A non-willful violation can reach up to $16,536 per report for 2026, and a willful violation can reach the greater of $165,353 or 50% of the account balance, per year.

Because the FBAR is a Title 31 penalty rather than a Title 26 tax penalty, some familiar relief tools work differently. First-Time Abatement, for example, does not apply to FBAR penalties, and the reasonable-cause standard for a non-willful FBAR violation is statutory and distinct from the tax reasonable-cause standard. A taxpayer who missed both forms may be exposed under both regimes at once, which is why the analysis and any request for relief have to address each track on its own terms. Our guides to reasonable cause and how to get IRS penalties removed explain the relief framework, and the willful-versus-non-willful line is covered in the FBAR penalties guide.

When Are the FBAR and Form 8938 Due, and Where Do They Go?

Both are tied to the tax calendar, but they go to different places. The FBAR is due April 15 with an automatic extension to October 15, so no separate extension request is required, and it is filed electronically with FinCEN through the BSA E-Filing System rather than with the IRS. Form 8938 is due when your income tax return is due, including extensions, and it is attached to that return and filed with the IRS.

The practical consequence is that the FBAR is easy to overlook precisely because it does not ride along with your Form 1040. A preparer focused on the income tax return may complete Form 8938 and still leave the separate FinCEN filing undone, or the reverse. Treating them as two obligations with two destinations, one to FinCEN and one to the IRS, is the habit that keeps taxpayers out of trouble on both.

FBAR and Form 8938 Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and business owners in Naples and across Southwest Florida sort out which foreign-account reports they actually owe, prepare and file the FBAR and Form 8938 correctly, and address prior years where one or both were missed. Much of this work is classification, meaning deciding whether an asset is a foreign financial account, a specified foreign financial asset, both, or neither, and then applying the right threshold for the taxpayer’s filing status and residence. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Dr. Pellumb Kabashi is the founder of Tax Expert Today LLC. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

What is the difference between the FBAR and Form 8938?

The FBAR (FinCEN Form 114) is a Bank Secrecy Act report filed with the Financial Crimes Enforcement Network when foreign financial accounts exceed $10,000 in aggregate at any time during the year. Form 8938 is a FATCA tax form filed with the IRS as part of your income tax return when specified foreign financial assets exceed a threshold that starts at $50,000. They come from different laws, go to different agencies, cover overlapping but different assets, and are filed separately.

Do I have to file both the FBAR and Form 8938?

Often, yes. If your foreign accounts exceed $10,000 in aggregate you file the FBAR, and if your specified foreign financial assets also exceed the Form 8938 threshold for your filing status and residence you additionally file Form 8938 with your return. The same account can appear on both. Filing one does not satisfy the requirement to file the other, and it is also possible to owe only one of them.

What are the Form 8938 filing thresholds?

For taxpayers living in the United States, the threshold is more than $50,000 on the last day of the year or more than $75,000 at any time for single filers, and more than $100,000 or $150,000 for married filing jointly. For taxpayers living abroad, the thresholds rise to more than $200,000 or $300,000 for single filers and more than $400,000 or $600,000 for married filing jointly. Meeting either the year-end or any-time test triggers the filing.

Does foreign real estate go on the FBAR or Form 8938?

Directly held foreign real estate is not reported on either the FBAR or Form 8938, because it is not a financial account or a specified foreign financial asset. If the property is held through a foreign entity, the interest in that entity can be reportable on Form 8938, and a foreign account connected to the property may be reportable on the FBAR. Rental income remains taxable and reportable on your return regardless.

What are the penalties for not filing Form 8938 or the FBAR?

Form 8938 carries a $10,000 failure-to-file penalty, up to an additional $50,000 for continued failure after IRS notice, and a 40% accuracy-related penalty on understatements tied to undisclosed assets. FBAR penalties for 2026 can reach up to $16,536 per report for non-willful violations and the greater of $165,353 or 50% of the account balance per year for willful violations. The two run on separate legal tracks and can apply at the same time.

Where can I get help with the FBAR or Form 8938 in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with determining which foreign-account reports apply, preparing the FBAR and Form 8938, and addressing prior missed years. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for Foreign-Account Reporting

The FBAR vs Form 8938 question rewards precision and punishes assumptions. The decisions that matter, such as whether an asset is an account or a specified asset, which threshold applies, whether signature authority alone creates a filing, and how to fix a year that was missed, all turn on facts that are easy to misread, and the penalties for guessing wrong sit on two separate tracks. Quietly filing a missed prior-year FBAR outside a formal program, or filing Form 8938 while overlooking the separate FinCEN filing, are the mistakes that most often turn a manageable situation into a larger one. Tax Expert Today LLC represents individuals and business owners in foreign-account compliance matters nationwide.

Call (239) 441-2005 or schedule a consultation to review which foreign-account reports apply to your situation and what bringing prior years current would involve. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 14, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005