By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: FBAR penalties depend entirely on whether the failure was willful. A non-willful violation carries a civil penalty of up to $16,536 for 2026 (the inflation-adjusted figure under 31 CFR 1010.821), and after the Supreme Court’s 2023 decision in Bittner it applies per unfiled report (per year), not per account. A willful violation is far worse: the greater of $165,353 or 50% of the account balance, assessed per account, per year. FBAR is a Bank Secrecy Act penalty under 31 U.S.C. §5321, so First-Time Abatement does not apply — but a statutory reasonable-cause defense does for non-willful cases, and the Streamlined Filing Compliance Procedures remain open in 2026 for taxpayers whose conduct was genuinely non-willful.

Published: June 30, 2026

An unfiled FBAR is one of the few compliance problems where the penalty can dwarf the tax. The report itself collects no revenue — it just discloses foreign accounts — yet the civil penalty for ignoring it runs into five and six figures, and in willful cases can exceed the entire balance of the account. Taxpayers sorting out which foreign-account reports they owe can compare the two filings in our guide to FBAR vs Form 8938. This 2026 guide explains how the penalties are actually calculated under 31 U.S.C. §5321, what changed when the Supreme Court decided Bittner, how the IRS separates a willful violation from an honest one, and the real paths to reduce or avoid the penalty. If you are still deciding whether you even had to file, start with our guide on whether you need to file an FBAR and come back here for the consequences.

What Are the Penalties for Not Filing an FBAR?

The penalty for not filing an FBAR splits into two tiers — non-willful and willful — and the gap between them is enormous. A non-willful failure (you didn’t know, or you made an honest mistake) is capped at $16,536 per report for 2026. A willful failure (you knew and chose not to file, or were recklessly indifferent) is the greater of $165,353 or half the account balance, for each account, every year. Both are civil penalties under 31 U.S.C. §5321; willful violations can also carry criminal exposure in the most serious cases.

Because FBAR lives in the Bank Secrecy Act (Title 31) rather than the tax code (Title 26), the relief tools taxpayers know from regular penalties work differently here. There is no First-Time Abatement for an FBAR penalty. The mitigation that does exist comes from the reasonable-cause exception written into the statute for non-willful cases, the IRS’s internal mitigation guidelines in IRM 4.26.16, and the offshore disclosure programs. The single most important variable in the whole analysis is willfulness, because it changes the ceiling by an order of magnitude.

| Violation type | 2026 maximum penalty | How it’s counted |

|---|---|---|

| Non-willful | Up to $16,536 | Per report (per year) — Bittner |

| Willful | Greater of $165,353 or 50% of the account balance | Per account, per year |

| Criminal (most serious willful cases) | Fines and potential imprisonment under 31 U.S.C. §5322 | Charged separately by DOJ |

The dollar figures move every year. The $10,000 and $100,000 amounts written into the statute in 2004 are adjusted for inflation under 31 CFR 1010.821, which is why the 2026 non-willful ceiling is $16,536 rather than a round $10,000. Always check the current table before assuming an amount.

How Much Is the Non-Willful FBAR Penalty in 2026?

The non-willful FBAR penalty for 2026 is up to $16,536 per unfiled report, and it is assessed once per year, not once per account. That second point is the change taxpayers most often get wrong, because for years the IRS argued the opposite. A taxpayer who failed to file FBARs for five years with a dozen foreign accounts faces a maximum exposure of 5 × $16,536 — roughly $82,680 — not twelve times that figure per year.

To put numbers on your own facts, run our FBAR penalty calculator, which applies the 2026 amounts and the per report rule automatically.

The word “maximum” matters. $16,536 is a ceiling, not an automatic charge. The IRS examiner handbook in IRM 4.26.16 directs examiners to consider mitigation and, in many non-willful cases involving smaller balances, to assert a single penalty for one year rather than stacking a penalty on every year. Where the facts support reasonable cause, the penalty can be removed entirely. The takeaway: a non-willful determination plus a clean reasonable-cause story is a very different exposure than the headline number suggests.

How Much Is the Willful FBAR Penalty?

The willful FBAR penalty for 2026 is the greater of $165,353 or 50% of the balance in the unreported account, and it applies per account, for each year of violation. This is the penalty that can exceed the money in the account itself. Two willful years on an account that held $400,000 can reach $200,000 per year — $400,000 total — before interest, and the IRS can assess it on each separately willful account.

Willful penalties also did not change under Bittner. The Supreme Court’s per-report rule applies only to non-willful violations; willful penalties remain account-by-account, which is exactly why the willful-versus-non-willful line is the whole ballgame. When I represent a client with unfiled FBARs, the first work is an honest, documented assessment of which side of that line the facts fall on — before a single form is filed — because the wrong characterization is expensive in both directions.

Did the Supreme Court Change FBAR Penalties? (Bittner v. United States)

Yes. In Bittner v. United States, 598 U.S. ___ (2023), decided February 28, 2023, the Supreme Court held 5-4 that the non-willful FBAR penalty accrues on a per-report basis, not a per-account basis. The practical effect was dramatic: the government had calculated Alexandru Bittner’s penalty at $2.72 million by charging $10,000 for each of 272 accounts across five years, and the Court reduced the theory to $10,000 per year — five reports, $50,000.

What Bittner did and didn’t do is worth being precise about, because the case is widely misread:

- It capped non-willful penalties at one per annual report, regardless of how many accounts that report should have listed.

- It did not touch willful penalties, which are still assessed per account, per year.

- It did not create a defense — it did not decide whether Bittner had reasonable cause or whether any penalty was owed at all, only how the per-violation math works.

So Bittner is genuinely good news for non-willful filers with many accounts, and irrelevant to someone the IRS can show acted willfully. That distinction is the reason the next two sections matter more than the dollar tables.

How Does the IRS Decide an FBAR Violation Was Willful?

The IRS treats an FBAR violation as willful when the taxpayer either knew about the filing requirement and intentionally disregarded it, or acted with reckless disregard or willful blindness toward an obvious duty to file. Willfulness in this civil context does not require a confession or proof of an evil motive. Courts have upheld willful penalties based on circumstantial “badges” — signing a tax return whose Schedule B asked directly about foreign accounts and answering “no,” moving money to conceal it, using a foreign entity to hold the account, or being told of the requirement and doing nothing.

The mistake I see most often is a taxpayer assuming “I didn’t actually know” automatically means non-willful. It doesn’t. Reckless disregard — failing to investigate a requirement that a reasonable person in the same position would have looked into — can support a willful penalty even without actual knowledge. That is why the characterization is a fact-intensive legal judgment, not a self-assessment, and why a taxpayer with a borderline file should get that judgment made carefully before choosing a disclosure path. Certifying “non-willful” under penalty of perjury when the facts are actually willful is its own serious problem.

Can FBAR Penalties Be Reduced or Removed?

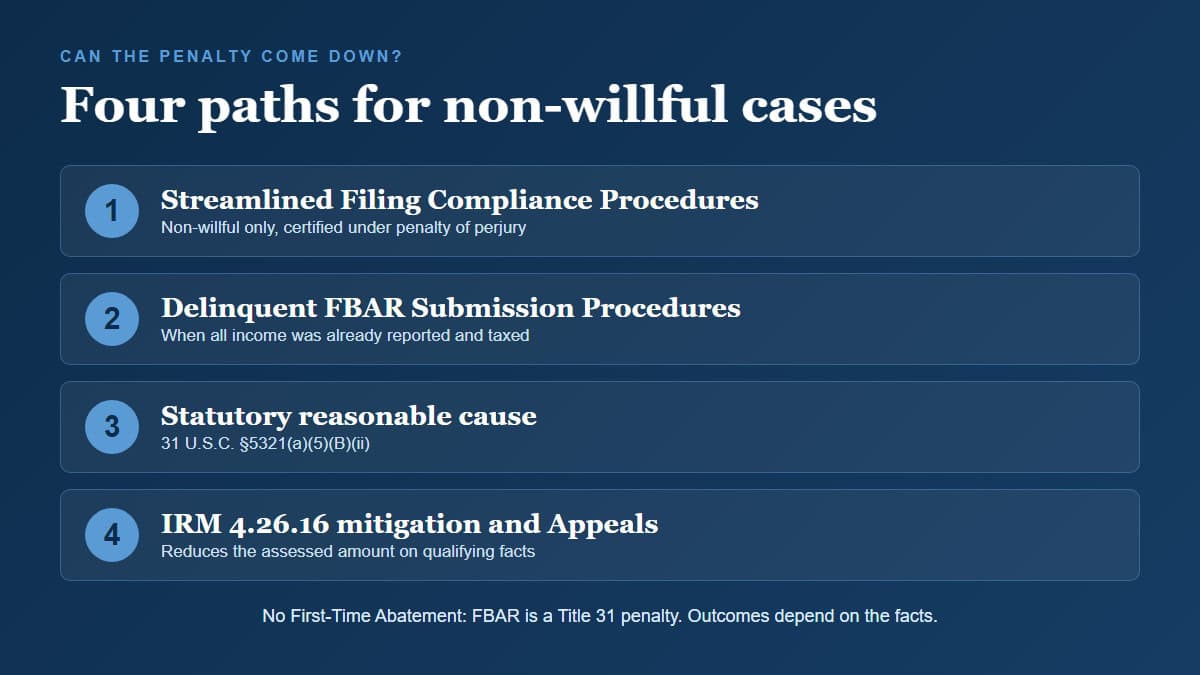

Yes, FBAR penalties can be reduced or removed, but the path depends on whether the conduct was non-willful and whether returns and income were otherwise correct. There is no First-Time Abatement for FBAR because it is a Title 31 penalty, so the realistic routes are these, roughly in order of how much exposure they resolve:

- Streamlined Filing Compliance Procedures. For taxpayers whose failure to file was non-willful, the Streamlined Filing Compliance Procedures let you file the delinquent FBARs and amended returns with a certification of non-willful conduct (Form 14653 for taxpayers abroad, Form 14654 for those in the U.S.). Taxpayers living outside the U.S. who qualify can resolve the matter with no FBAR penalty; U.S.-resident filers pay a 5% miscellaneous offshore penalty on the relevant assets instead of FBAR penalties. This program remains open in 2026, but it has no guaranteed end date and the IRS can close it on short notice — the window may not stay open indefinitely.

- Delinquent FBAR Submission Procedures. If you reported all your income and paid all your tax but simply missed the FBAR, you may be able to e-file the late FBARs with a reasonable-cause statement and avoid a penalty, in qualifying cases, without entering the streamlined program at all.

- Statutory reasonable cause. The non-willful penalty under 31 U.S.C. §5321(a)(5)(B)(ii) does not apply where the violation was due to reasonable cause and the balance was properly reported. This is raised in an examination or appeal and turns on the specific facts.

- Mitigation under IRM 4.26.16 and Appeals. Even where some penalty applies, the IRS mitigation guidelines and the Independent Office of Appeals can substantially reduce the assessed amount based on account balances, compliance history, and the strength of the reasonable-cause facts.

Outcomes vary substantially based on individual facts, and choosing among these paths is where most of the value — and most of the risk — sits. Picking the wrong program can forfeit relief or, worse, convert a defensible position into a false certification. The penalty-relief mechanics for ordinary tax penalties are covered in our guide on how to get IRS penalties removed, but the FBAR analysis is its own animal.

What Is the Reasonable-Cause Defense for FBAR Penalties?

The reasonable-cause defense for an FBAR penalty is a statutory exception that bars the non-willful penalty when the failure was due to reasonable cause and the account balance was correctly reported once the taxpayer became aware. It comes from the FBAR statute itself, 31 U.S.C. §5321(a)(5)(B)(ii), and it is narrower than the reasonable-cause standard taxpayers may know from income-tax penalties. Two points define it: it is available only for non-willful violations, and it requires that the underlying account information ultimately be reported correctly.

What counts as reasonable cause is a facts-and-circumstances test, weighed the way the tax reasonable-cause cases are weighed — reliance on a qualified professional who was given complete information, a genuine and reasonable lack of awareness given the taxpayer’s background, serious illness, or other circumstances outside the taxpayer’s control. It is not reasonable cause to simply not have looked into an obligation that applied to you. Because the FBAR version of the defense overlaps with, but is not identical to, the income-tax version explained in our reasonable cause IRS penalty guide, the documentation has to be built specifically for the FBAR statute.

FBAR Penalty Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and business owners in Naples and across Southwest Florida address unfiled FBARs, respond to FBAR penalty assessments, and come back into compliance through the streamlined or delinquent-submission procedures where they qualify. The work is bringing a taxpayer’s foreign-account reporting into compliance and presenting the facts on willfulness and reasonable cause accurately — not promising a particular result, since FBAR outcomes turn on the specific facts and the IRS’s review. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

How much is the FBAR penalty in 2026?

For 2026, the non-willful FBAR penalty is up to $16,536 per unfiled report, and after the Supreme Court’s 2023 decision in Bittner it is charged per report (per year) rather than per account. The willful penalty is the greater of $165,353 or 50% of the account balance, assessed per account, per year. These figures are inflation-adjusted annually under 31 CFR 1010.821, so the exact amounts change each year.

Is the FBAR penalty per account or per year?

For non-willful violations, the penalty is per report, meaning once per year regardless of how many accounts the FBAR should have listed — that is the holding of Bittner v. United States (2023). For willful violations, the penalty is still assessed per account, per year, which is why willful exposure can be many times larger than non-willful exposure for the same set of accounts.

Can I go to jail for not filing an FBAR?

Criminal prosecution is possible but reserved for the most serious willful cases, typically involving active concealment, and it is charged separately by the Department of Justice under 31 U.S.C. §5322. The vast majority of FBAR matters are resolved as civil penalties. A taxpayer whose failure was non-willful is dealing with a civil penalty that, where reasonable cause or the streamlined procedures apply, may be reduced or eliminated.

Does First-Time Abatement remove an FBAR penalty?

No. First-Time Abatement applies only to certain Title 26 tax penalties — failure to file, failure to pay, and failure to deposit — not to the FBAR penalty, which arises under the Title 31 Bank Secrecy Act. For FBAR, the relief routes are the statutory non-willful reasonable-cause exception, the Streamlined Filing Compliance Procedures, the Delinquent FBAR Submission Procedures, and mitigation in examination or Appeals.

Are the streamlined procedures still available in 2026?

Yes. As of mid-2026 the IRS Streamlined Filing Compliance Procedures remain open to taxpayers whose failure to file was non-willful, and they require a certification of non-willfulness under penalty of perjury on Form 14653 or 14654. The IRS has not announced an end date, but it can close the program on short notice, so eligible taxpayers generally should not assume the window stays open indefinitely.

Where can I get help with FBAR penalties in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with unfiled FBARs, FBAR penalty assessments, and the streamlined and delinquent-submission procedures. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for an FBAR Penalty

FBAR cases reward early, accurate characterization and punish guesswork. The judgment calls — whether the facts are non-willful, whether reasonable cause is genuinely available, and which disclosure path fits — have to be made before anything is filed, because a streamlined certification and a delinquent-submission statement say different things under penalty of perjury, and the wrong choice can forfeit relief or create a new problem. Quietly filing prior-year FBARs without analyzing willfulness first (a “quiet disclosure”) is the move that most often backfires. Tax Expert Today LLC represents individuals and business owners in foreign-account compliance and IRS penalty matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review an FBAR penalty notice or an unfiled-FBAR situation and the disclosure options that fit your facts. With the streamlined program’s future uncertain, the review is worth starting sooner rather than later. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published June 30, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005