By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: The IRS Streamlined Filing Compliance Procedures are a catch-up program for taxpayers whose failure to report foreign accounts and foreign income was non-willful. You file 3 years of amended returns and 6 years of delinquent FBARs, and certify non-willful conduct under penalty of perjury on Form 14653 or 14654. Taxpayers who live abroad and qualify (the Streamlined Foreign Offshore Procedures) pay no offshore penalty; U.S. residents (the Streamlined Domestic Offshore Procedures) pay a 5% miscellaneous offshore penalty on the highest year-end value of the unreported foreign assets, in place of the FBAR penalties that could otherwise reach $16,536 or more per year. The program remains open in 2026 — but it can be closed on short notice, and it is only for taxpayers who were genuinely non-willful.

Published: July 7, 2026

The streamlined procedures exist for one specific person: someone who genuinely did not know they had to report a foreign account or foreign income, and now wants to fix it before the IRS finds it first. If that describes you, this 2026 guide explains exactly how the program works, who qualifies, the difference between the domestic 5% path and the foreign no-penalty path, what you have to file, and the one thing that can turn a clean disclosure into a serious problem. If you have already received a penalty or want to understand the exposure you are avoiding, start with our guide to FBAR penalties, then come back here for the fix.

What Are the IRS Streamlined Filing Compliance Procedures?

The Streamlined Filing Compliance Procedures are an IRS program that lets taxpayers who non-willfully failed to report foreign financial accounts, foreign income, or foreign assets come into compliance by filing amended returns and delinquent FBARs with a reduced or zero offshore penalty. The IRS introduced the current version in 2014 to give honest non-filers a path that does not run through the much harsher voluntary-disclosure track built for willful conduct. Taxpayers whose unfiled tax returns are purely domestic follow the ordinary catch-up path instead. There are two tracks: Streamlined Foreign Offshore Procedures (SFOP) for taxpayers who live abroad, and Streamlined Domestic Offshore Procedures (SDOP) for those who live in the United States.

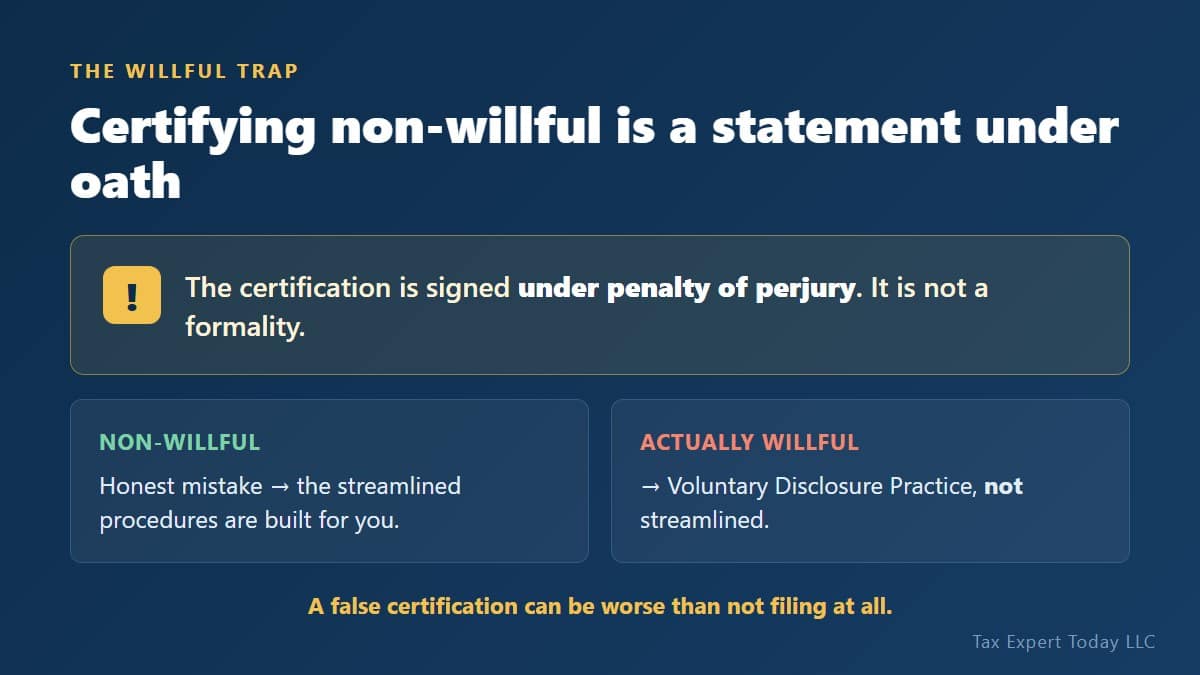

The defining feature of the program is the non-willful certification. You are not just filing late paperwork — you are signing a statement, under penalty of perjury, that your failure to file was due to non-willful conduct, meaning negligence, inadvertence, mistake, or a good-faith misunderstanding of the law. That certification is the gate. It is what makes the reduced penalty available, and it is also what makes the program dangerous for anyone whose conduct was actually willful.

Who Qualifies for the Streamlined Procedures?

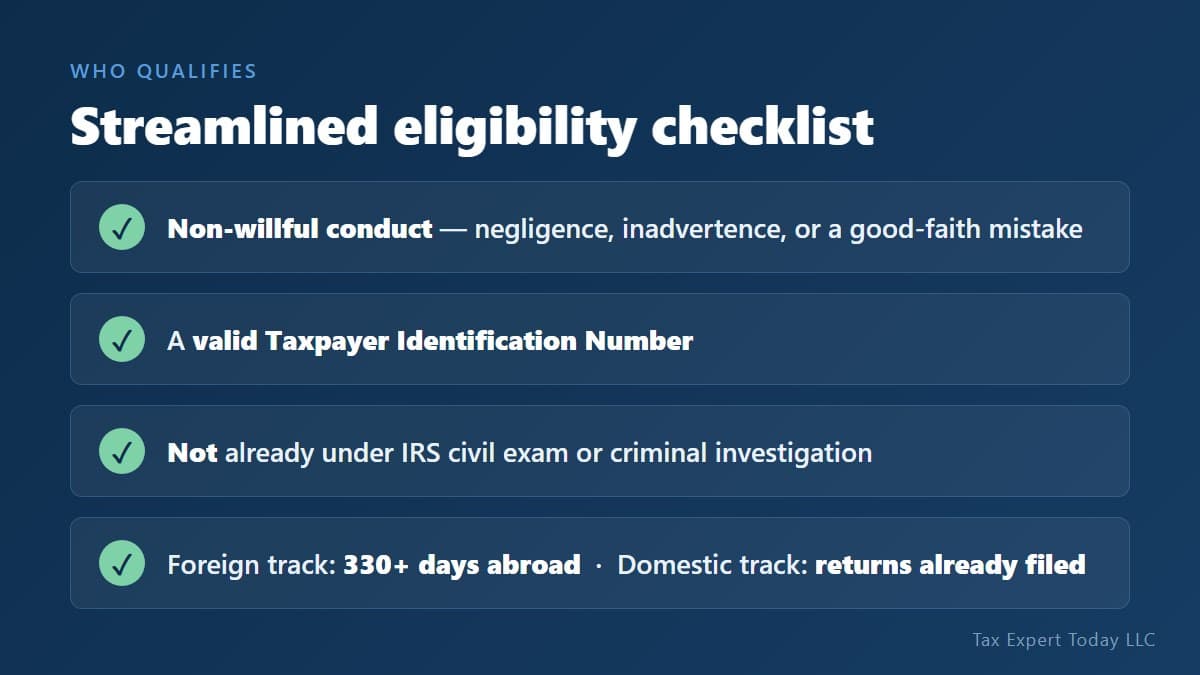

You qualify for the streamlined procedures if your failure to report foreign income and file FBARs was non-willful, you have a valid Taxpayer Identification Number, and the IRS has not already opened a civil examination or criminal investigation of your returns. The central requirement is non-willfulness — the conduct has to have been the result of a genuine mistake or lack of awareness, not a choice to hide accounts.

Beyond non-willfulness, eligibility splits by where you live:

- Foreign (SFOP): you must meet a non-residency requirement — generally, in at least one of the last three years you were physically outside the United States for at least 330 days and did not have a U.S. abode.

- Domestic (SDOP): you do not meet the foreign non-residency test (you are a U.S. resident), but you have already filed U.S. tax returns for each of the most recent three years and failed only to report the foreign income or assets on them.

One disqualifier catches people off guard: if the IRS has already started looking at you, the door is closed. The mistake I see most often is a taxpayer who waits, hoping the issue goes away, and loses access to the program the moment a notice or examination lands. The program rewards coming forward first.

What’s the Difference Between the Domestic and Foreign Streamlined Procedures?

The difference is the penalty: the Streamlined Foreign Offshore Procedures carry no offshore penalty, while the Streamlined Domestic Offshore Procedures carry a 5% miscellaneous offshore penalty on the unreported foreign assets. Both require the same returns, the same six years of FBARs, and the same non-willful certification — the dividing line is residency, and it is worth real money.

| Feature | Foreign (SFOP) | Domestic (SDOP) |

|---|---|---|

| Who it’s for | Taxpayers who meet the non-residency test | U.S. residents who already filed returns |

| Offshore penalty | None (0%) | 5% of highest year-end value of foreign assets |

| Amended returns | 3 years | 3 years |

| Delinquent FBARs | 6 years | 6 years |

| Certification form | Form 14653 | Form 14654 |

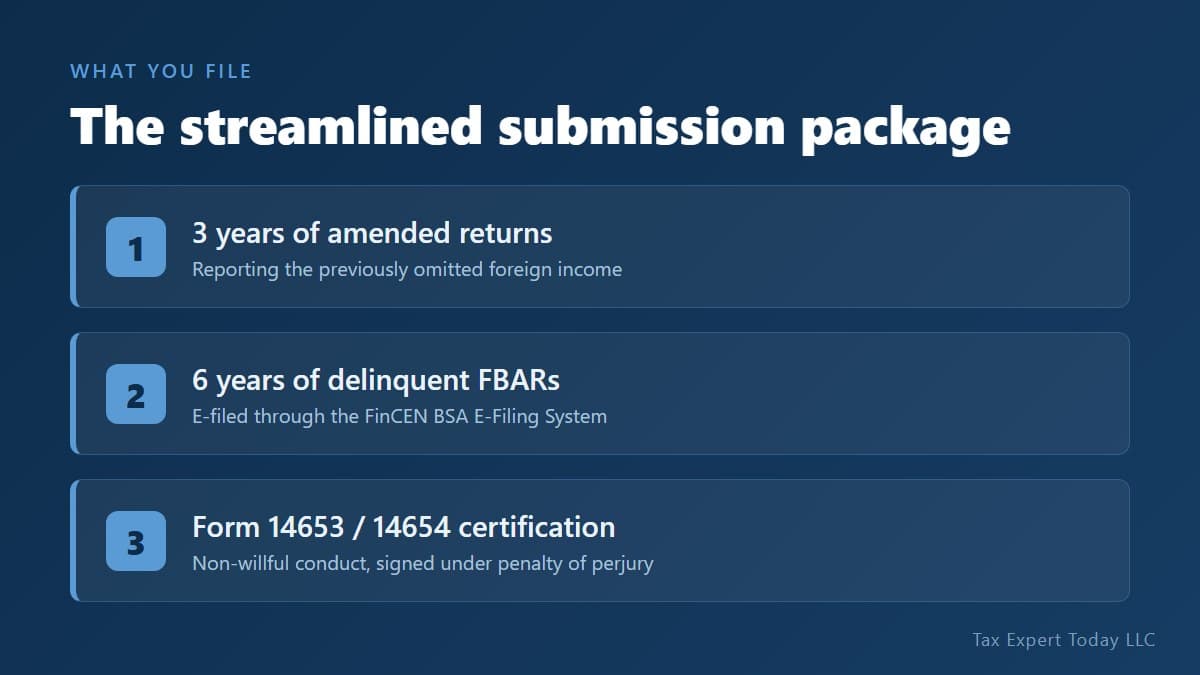

What Do You Have to File Under the Streamlined Procedures?

A streamlined submission has three parts: three years of amended or delinquent income tax returns reporting the previously omitted foreign income, six years of delinquent FBARs filed electronically, and the signed non-willful certification (Form 14653 for the foreign track, Form 14654 for the domestic track). The returns and certification go to the IRS by mail in a single package; the FBARs are e-filed separately through the FinCEN BSA E-Filing System with a streamlined explanation.

The certification is the heart of the package, not a formality. It has to lay out the specific facts and the story of why the failure happened — where the accounts came from, why they went unreported, what you understood at the time. A vague or boilerplate certification is the most common reason a submission draws scrutiny. For U.S.-resident filers, the package also has to compute and pay the 5% penalty plus the tax and interest due on the amended returns.

How Much Is the Streamlined Penalty?

For the domestic procedures, the penalty is 5% of the highest aggregate year-end balance or value of the foreign financial assets that were subject to reporting during the covered period; for the foreign procedures, there is no offshore penalty at all. The 5% is calculated once — it is not 5% per year. On foreign assets that peaked at a $300,000 year-end value, the domestic penalty is $15,000, paid with the submission, and it stands in for the FBAR penalties that could otherwise have applied for each unreported year.

To see what the statutory FBAR exposure could be without the program, run our FBAR penalty calculator and compare that number with the single 5 percent streamlined charge.

That trade is the whole point of the program. Compared with a non-willful FBAR penalty of up to $16,536 per year across multiple years — or the far larger willful exposure — a one-time 5% charge (or zero, if you live abroad and qualify) is why the streamlined path is so valuable for the taxpayer it was designed for. Outcomes still depend on the specific facts and on the IRS accepting the non-willful certification.

What Are the Risks If You Were Actually Willful?

If your conduct was actually willful, using the streamlined procedures is a serious mistake, because the non-willful certification is signed under penalty of perjury and a false certification can expose you to the full willful penalties and potential criminal liability. The program is not a loophole for someone who knew about the accounts and chose not to report them. The IRS reviews certifications, and a streamlined submission that is later found to be willful can be worse than never having filed it, because it adds a false statement to the original problem.

This is the judgment that has to be made before anything is filed, and it is genuinely a legal call rather than a self-assessment. Willfulness in this area includes reckless disregard and willful blindness, not just clear intent — the standard explained in our FBAR penalties guide. Where the facts are close, the analysis of whether streamlined is even the right program is the most important part of the whole engagement. A taxpayer with willful exposure usually belongs in the separate IRS Criminal Investigation Voluntary Disclosure Practice, not the streamlined track.

Are the Streamlined Procedures Still Available in 2026?

Yes, the Streamlined Filing Compliance Procedures remain open as of mid-2026, and the IRS has not announced an end date. That said, the IRS has the authority to modify or close the program at any time, on short notice and without a grace period, the way it ended the earlier Offshore Voluntary Disclosure Program in 2018. Commentators have flagged the possibility of the streamlined program tightening or closing as international reporting data improves.

What that means practically: eligibility is determined at the time you submit, so a taxpayer who qualifies today should not assume the same option exists indefinitely. Where the facts support a non-willful disclosure, the conservative move is to prepare and file rather than wait. The window is open now; nobody can promise it stays open.

Streamlined Filing Help in Naples and Southwest Florida

Tax Expert Today LLC helps individuals and business owners in Naples and across Southwest Florida evaluate whether the streamlined procedures fit their facts, prepare the amended returns and delinquent FBARs, and draft the non-willful certification that supports the disclosure. The work begins with an honest assessment of whether the conduct was non-willful and whether streamlined is the correct program at all — not a promise of a particular result, since eligibility and outcomes turn on the facts and on IRS acceptance. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys serving clients in all 50 states. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

What are the IRS Streamlined Filing Compliance Procedures?

They are an IRS program that lets taxpayers whose failure to report foreign accounts and income was non-willful come into compliance by filing three years of amended returns and six years of delinquent FBARs, along with a certification of non-willful conduct. Taxpayers who live abroad and qualify pay no offshore penalty under the Streamlined Foreign Offshore Procedures; U.S. residents pay a one-time 5% miscellaneous offshore penalty under the Streamlined Domestic Offshore Procedures.

Who qualifies for the streamlined procedures?

Taxpayers whose failure to report was non-willful, who have a valid Taxpayer Identification Number, and who are not already under IRS civil examination or criminal investigation. The foreign track additionally requires meeting a non-residency test (generally at least 330 days outside the U.S. in one of the last three years), while the domestic track is for U.S. residents who already filed returns but omitted the foreign income or assets.

How much is the streamlined penalty?

Under the Streamlined Domestic Offshore Procedures, the penalty is a one-time 5% of the highest aggregate year-end value of the foreign financial assets during the covered period. Under the Streamlined Foreign Offshore Procedures, there is no offshore penalty. Both still require paying any tax and interest due on the three years of amended returns.

What happens if the IRS thinks I was willful?

The streamlined certification is signed under penalty of perjury, so a taxpayer who was actually willful and certifies non-willful conduct can face the full willful FBAR penalties and potential criminal liability for a false statement. The program is only for genuinely non-willful conduct. A taxpayer with willful exposure generally belongs in the separate IRS Criminal Investigation Voluntary Disclosure Practice, and the willful-versus-non-willful judgment should be made before anything is filed.

Are the streamlined procedures still available in 2026?

Yes, as of mid-2026 the program remains open and the IRS has not announced an end date. The IRS can modify or close it at any time on short notice, as it did with the Offshore Voluntary Disclosure Program in 2018, so eligible taxpayers should not assume the option will remain available indefinitely.

Where can I get help with a streamlined filing in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, assists individuals and businesses in Naples and across Southwest Florida with evaluating eligibility, preparing the amended returns and delinquent FBARs, and drafting the non-willful certification. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and represents taxpayers before the IRS nationwide. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional for a Streamlined Submission

The streamlined procedures reward an accurate read of the facts and punish a careless one. The decisions that matter — whether the conduct was truly non-willful, whether the foreign or domestic track applies, how to compute the 5% base, and how to write a certification that holds up — all happen before the package is mailed, and the certification commits you under penalty of perjury. Filing a streamlined submission without first analyzing willfulness, or quietly filing prior-year FBARs outside any program (a “quiet disclosure”), are the two moves that most often turn a fixable problem into a worse one. Tax Expert Today LLC represents individuals and business owners in foreign-account compliance matters nationwide. Dr. Kabashi is an Enrolled Agent authorized to represent taxpayers before the IRS in all 50 states.

Call (239) 441-2005 or schedule a consultation to review whether the streamlined procedures fit your facts and what a submission would involve. With the program’s future uncertain, the review is worth starting sooner rather than later. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 7, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005