By Dr. Pellumb Kabashi, DBA, MBA, EA, CFE, CES

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

Quick Answer: The national offer in compromise acceptance rate fell to 14.1 percent in fiscal year 2025, the lowest level in at least a decade. IRS Data Book figures show the agency received 38,797 offers and accepted 5,464, down from 12,711 acceptances just two years earlier. Applications rose 28.6 percent over those same two years, which means more taxpayers are applying while far fewer are getting through. The average accepted offer settled for $17,962.

Published: July 14, 2026

Tax Expert Today Research · Report 2026-01

The Offer in Compromise Report, FY2016 to FY2025. An original analysis of eleven editions of the IRS Data Book. Every figure in this report was computed directly from IRS source tables, cross checked across overlapping editions, and is reproducible from the files listed above. This report is updated annually when the IRS releases new Data Book figures. Download the PDF edition or browse all TET Research reports.

The offer in compromise is the most searched form of IRS debt relief, and the numbers behind it just moved sharply. Tax Expert Today analyzed every IRS Data Book from fiscal year 2015 through fiscal year 2025 to build a verified ten year series on how many offers taxpayers submit, how many the IRS accepts, and what the accepted deals actually look like. The result is a picture of a program that has quietly become far more selective. This report presents the data, what changed, and what it means for anyone considering an offer under IRC Section 7122. For the program mechanics themselves, our companion guide to the IRS offer in compromise covers eligibility and the application process step by step.

What Is the IRS Offer in Compromise Acceptance Rate in 2026?

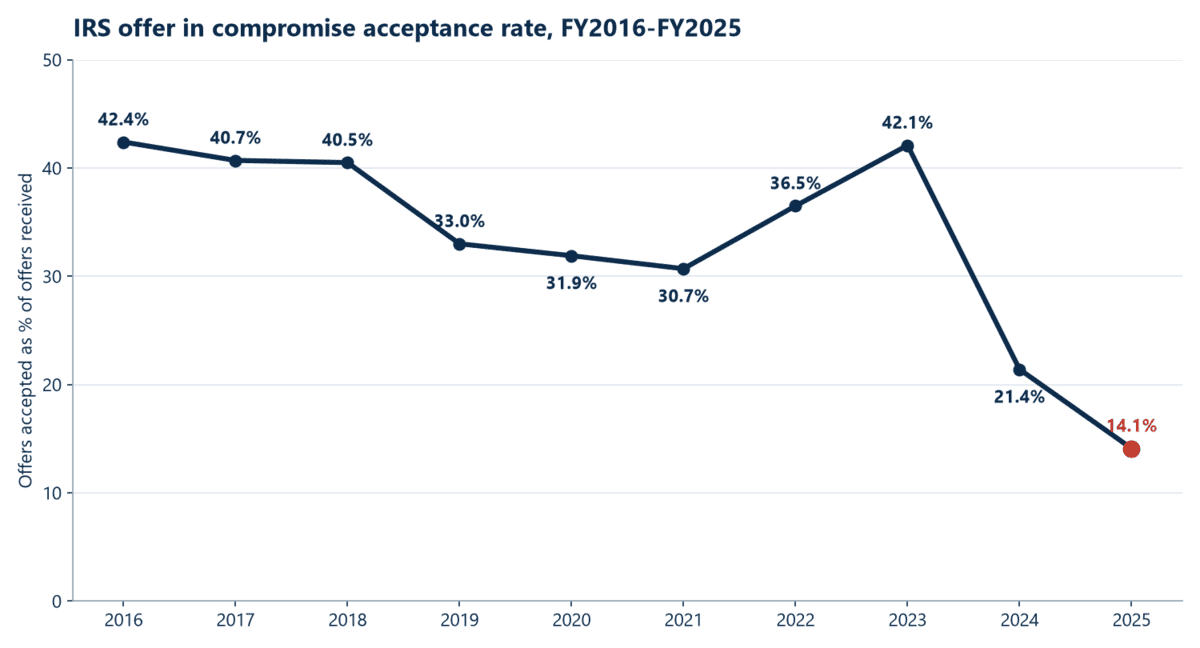

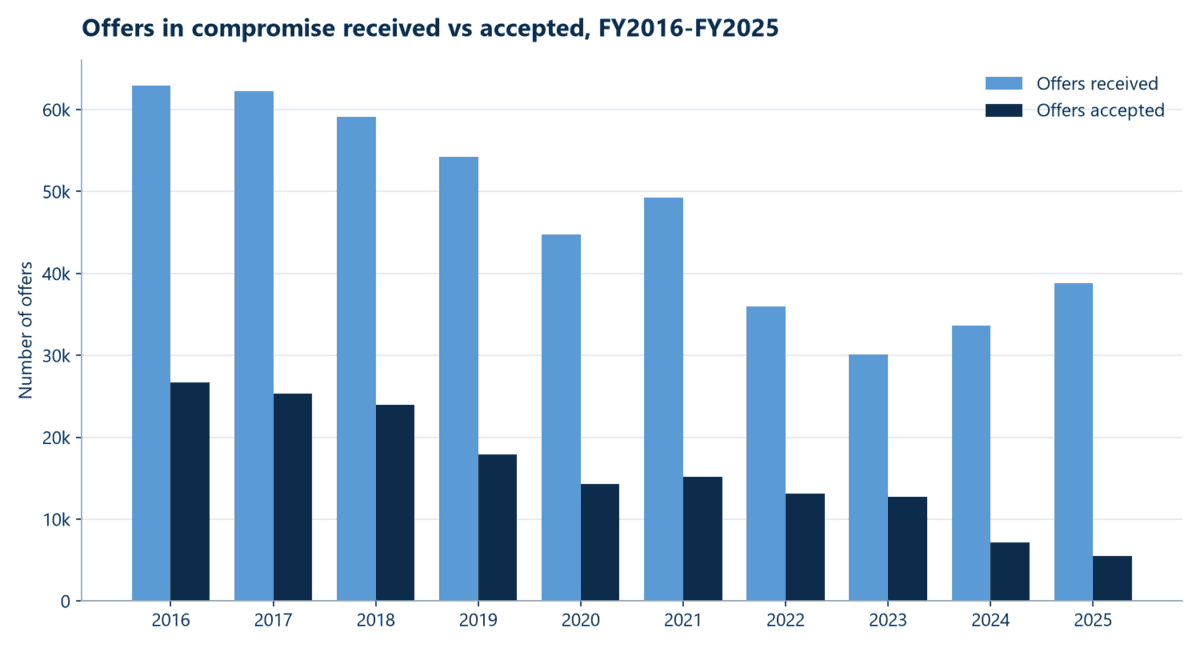

The most recent official figure is 14.1 percent, from fiscal year 2025, which ended September 30, 2025. The IRS received 38,797 offers in compromise that year and accepted 5,464, according to Table 4-1 of the FY2025 IRS Data Book. That is roughly one acceptance for every seven offers submitted.

To put 14.1 percent in context, the acceptance rate averaged 35.5 percent across the prior nine fiscal years and never fell below 30 percent between FY2016 and FY2023. The FY2025 figure is not a rounding quirk or a one year blip in an otherwise stable series. It is the second consecutive record low, following 21.4 percent in FY2024, and it represents a collapse from the 42.1 percent rate the program posted as recently as FY2023.

How Many Offers in Compromise Did the IRS Accept in FY2025?

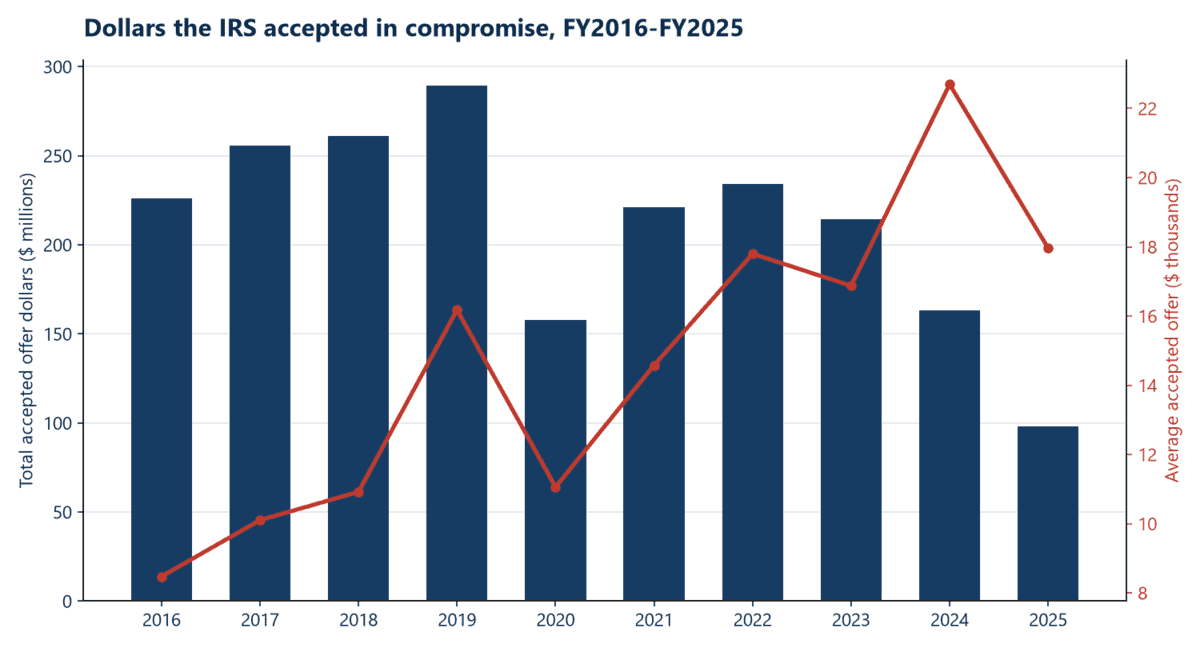

The IRS accepted 5,464 offers in compromise in fiscal year 2025, worth a combined $98.1 million. Both numbers are the lowest in the ten year series. FY2025 is the first year in the series in which total accepted offer dollars fell below $100 million, and the accepted count is less than a quarter of the 26,663 offers the IRS accepted in FY2016.

The average accepted offer in FY2025 was $17,962, computed as $98.1 million divided by 5,464 acceptances. That average has climbed over the decade, from $8,474 in FY2016 to a peak of $22,695 in FY2024, which suggests the offers that do get through increasingly involve larger settlements rather than small hardship compromises. The dollar figures measure what taxpayers agreed to pay, not the debt forgiven; the IRS does not publish the face value of the liabilities compromised in this table.

How Has the Acceptance Rate Changed Over the Last Decade?

The acceptance rate held between 30 and 42 percent for eight straight years, then fell off a cliff. From FY2016 through FY2023 the program was, by historical standards, generous: roughly four in ten offers were accepted at the decade’s two peaks in FY2016 and FY2023. In FY2024 the rate dropped to 21.4 percent, and in FY2025 it dropped again to 14.1 percent. The full verified series is below.

| Fiscal year | Offers received | Offers accepted | Acceptance rate | Dollars accepted | Average accepted offer |

|---|---|---|---|---|---|

| 2016 | 62,937 | 26,663 | 42.4% | $225.9M | $8,474 |

| 2017 | 62,243 | 25,326 | 40.7% | $255.9M | $10,103 |

| 2018 | 59,127 | 23,929 | 40.5% | $261.3M | $10,919 |

| 2019 | 54,225 | 17,890 | 33.0% | $289.4M | $16,178 |

| 2020 | 44,809 | 14,288 | 31.9% | $158.0M | $11,059 |

| 2021 | 49,285 | 15,154 | 30.7% | $220.9M | $14,579 |

| 2022 | 36,022 | 13,165 | 36.5% | $234.3M | $17,799 |

| 2023 | 30,163 | 12,711 | 42.1% | $214.5M | $16,874 |

| 2024 | 33,591 | 7,199 | 21.4% | $163.4M | $22,695 |

| 2025 | 38,797 | 5,464 | 14.1% | $98.1M | $17,962 |

Sources: IRS Data Book, delinquent collection activities table, FY2016 through FY2025 editions. Dollar amounts are totals of accepted offers. The acceptance rate divides offers accepted by offers received in the same fiscal year; see the methodology note for the limits of that ratio.

Why Are Fewer Offers Being Accepted?

The IRS Data Book reports what happened, not why, so any explanation involves judgment. What the data itself shows is a program processing a rising workload with sharply fewer approvals. Three observable shifts frame the decline, and together they point to a program that has become more selective at exactly the moment more taxpayers are asking for relief.

First, demand is rising. Offers received climbed 28.6 percent between FY2023 and FY2025, from 30,163 to 38,797, reversing seven years of declining application volume. Second, acceptances collapsed over the same window, falling 57.0 percent from 12,711 to 5,464. Third, the broader collection pipeline is swelling: the inventory of taxpayer delinquent accounts jumped from 2,050,877 at the end of FY2024 to 3,234,815 at the end of FY2025, a 57.7 percent increase in a single year, according to the same Data Book table. A larger backlog, more applications, and fewer approvals can reflect staffing constraints, slower processing that pushes decisions into later fiscal years, tighter screening, or all three at once. The Data Book does not separate those effects, and this report does not guess beyond what the table supports.

What Does a 14 Percent Acceptance Rate Mean If You Owe the IRS?

It means the offer in compromise is still a real option, but the margin for a casual application is gone. When I review offers that failed, the most common defect I see is a reasonable collection potential calculation that does not hold up, because the taxpayer valued assets or future income differently than Form 656 Booklet standards require. In a year when the IRS is accepting one offer in seven, an application with a soft spot in the math is the first one screened out.

The current program terms have not changed: a $205 application fee, a 20 percent initial payment on lump sum offers, and an exemption from both for taxpayers who meet the low income certification in the Form 656 Booklet. What has changed is the practical bar. Before filing, it is worth pressure testing three things: whether the reasonable collection potential figure is defensible line by line, whether a partial pay installment agreement or currently not collectible status reaches a similar monthly outcome with less execution risk, and whether penalty relief should come first, since removing penalties shrinks the balance an offer has to compromise. The FY2025 penalty data makes that last point concrete: the IRS abated $7.5 billion of the $33.1 billion in individual civil penalties it assessed, per Data Book Table 4-2, so penalty relief remains a far higher percentage play than the offer program itself.

Does a Rejected Offer in Compromise Make Things Worse?

A rejected offer does not increase what you owe, but it costs time, and time has a price on a delinquent account. Interest continues to accrue during the review, the collection statute of limitations under IRC Section 6502 is suspended while the offer is pending, and the 20 percent initial payment on a lump sum offer is applied to your liability rather than refunded if the offer is rejected.

Rejection also has a defined appeal path: the IRS must give written reasons, and you have 30 days to request review by the Independent Office of Appeals on Form 13711. The practical takeaway from the FY2025 numbers is not that taxpayers should stop applying. It is that the six in seven who are turned away spend months of suspended collection clock and often a nonrefundable deposit to learn their offer was not built to the standard the IRS actually applies. Preparation, not hope, is what separates the two groups.

How Was This Report Prepared?

Methodology. Tax Expert Today extracted the offers in compromise block (offers received, offers accepted, and amount of offers accepted) from the delinquent collection activities table in eleven editions of the IRS Data Book, Publication 55-B, covering fiscal years 2015 through 2025. Each edition reports two fiscal years, so every year from FY2016 through FY2024 appears in two editions; overlapping values were cross checked and matched in every case. Where an older edition rounds counts to thousands, the precise figure from the more detailed edition was used. The acceptance rate divides offers accepted by offers received in the same fiscal year. Because an offer accepted in one year may have been received in a prior year, this ratio is the standard practitioner measure of program selectivity rather than a true cohort disposition rate. Federal fiscal years run October 1 through September 30. All source files and calculations are retained and available on request. The full verified series is downloadable as a machine readable file: tet-oic-series-fy2016-fy2025.csv. The data may be reused with attribution to Tax Expert Today LLC.

Offer in Compromise Guidance in Naples and Southwest Florida

Tax Expert Today LLC advises individuals and business owners in Naples and across Southwest Florida who are weighing an offer in compromise against the other resolution paths the data favors, from penalty abatement to structured payment agreements. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and it builds each offer on a documented reasonable collection potential analysis before anything is filed, because that is the number the IRS tests first. The office is at 11983 Tamiami Trail N, Naples, FL 34110, and the team can be reached at (239) 441-2005, Monday through Friday, 10am to 5pm ET.

Frequently Asked Questions

What percentage of offers in compromise does the IRS accept?

The IRS accepted 14.1 percent of offers in compromise in fiscal year 2025, based on 5,464 acceptances out of 38,797 offers received in IRS Data Book Table 4-1. That is the lowest rate in at least a decade. Across fiscal years 2016 through 2023 the rate ranged between 30.7 percent and 42.4 percent, so the current figure represents a sharp break from the program’s historical pattern.

How much does the average accepted offer in compromise settle for?

The average accepted offer in fiscal year 2025 was $17,962, computed from $98.1 million in total accepted offer dollars across 5,464 accepted offers. The average has risen substantially over the decade, from $8,474 in fiscal year 2016 to a peak of $22,695 in fiscal year 2024. These figures measure the amount taxpayers agreed to pay, not the size of the debt that was compromised.

Is the offer in compromise program harder to qualify for now?

The eligibility rules have not formally changed, but the outcomes have. Acceptances fell 57 percent between fiscal years 2023 and 2025 while applications rose 28.6 percent, so a materially smaller share of applicants is getting through. The formal standards in IRC Section 7122 and the Form 656 Booklet remain the same, which makes the quality of the reasonable collection potential calculation the deciding factor in a far more selective environment.

What happens to my money if the IRS rejects my offer?

The $205 application fee is nonrefundable, and the 20 percent initial payment required with a lump sum offer is applied to your outstanding tax liability rather than returned. Interest continues to accrue while the offer is under review, and the collection statute of limitations is suspended during that period. You have 30 days from a rejection letter to appeal to the IRS Independent Office of Appeals using Form 13711.

Should I try penalty abatement before an offer in compromise?

Often, yes. The IRS abated $7.5 billion of the $33.1 billion in individual civil penalties it assessed in fiscal year 2025, per Data Book Table 4-2, so penalty relief succeeds at a far higher rate than the 14.1 percent offer acceptance rate. Removing penalties first shrinks the balance an offer must compromise, and in some cases it reduces the debt enough that a payment agreement becomes workable without an offer at all.

Where can I get help evaluating an offer in compromise in Naples, FL?

Tax Expert Today LLC, located at 11983 Tamiami Trail N, Naples, FL 34110, evaluates offer in compromise candidacy for taxpayers in Naples and across Southwest Florida, and represents clients before the IRS nationwide. The firm is multidisciplinary, with enrolled agents, CPAs, and attorneys, and it prepares the reasonable collection potential analysis before filing so the offer is built to the standard the IRS applies. Consultations can be arranged at (239) 441-2005.

When to Engage a Professional About an Offer in Compromise

The FY2025 data changes the calculus, not the goal. With one offer in seven accepted, the expensive mistake is filing an offer that was never competitive, spending the fee, the deposit, and a year of suspended collection clock to receive a rejection letter. A professional review earns its keep in the sequencing: verifying the reasonable collection potential number line by line, testing whether penalty relief or a payment agreement reaches a better outcome faster, and preparing the offer file to the documentation standard the Form 656 Booklet actually demands. Tax Expert Today LLC represents individuals and businesses in IRS collection matters nationwide, and Dr. Kabashi, the firm’s founder, leads the resolution practice.

Call (239) 441-2005 or schedule a consultation to review whether an offer in compromise, penalty relief, or a payment agreement fits your facts. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published July 14, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005