By Dr. Pellumb Kabashi, DBA, MBA, CES, CFE, EA

Founder, Tax Expert Today LLC · Tax advisors, enrolled agents, CPAs, and attorneys · Serving clients in all 50 states

First-Time Penalty Abatement is the fastest, cheapest, and most overlooked way to remove IRS penalties. The IRS approves it administratively under IRM 20.1.1.3.3.2.1. No reasonable cause story required. No supporting documentation. No Form 843 narrative. A single phone call to the IRS Practitioner Priority Service often handles it. Yet most taxpayers never request it, and many tax preparers fail to mention it. This guide walks through how First-Time Penalty Abatement works, who qualifies, and the procedural sequence for getting approved in 2026.

What Is First-Time Penalty Abatement (FTA)?

First-Time Penalty Abatement is an administrative waiver the IRS grants under its Internal Revenue Manual (IRM 20.1.1.3.3.2.1). The program removes specific penalties for taxpayers who maintained a clean compliance history before the penalty year. The IRS designed it to reward consistent filers who fell behind once.

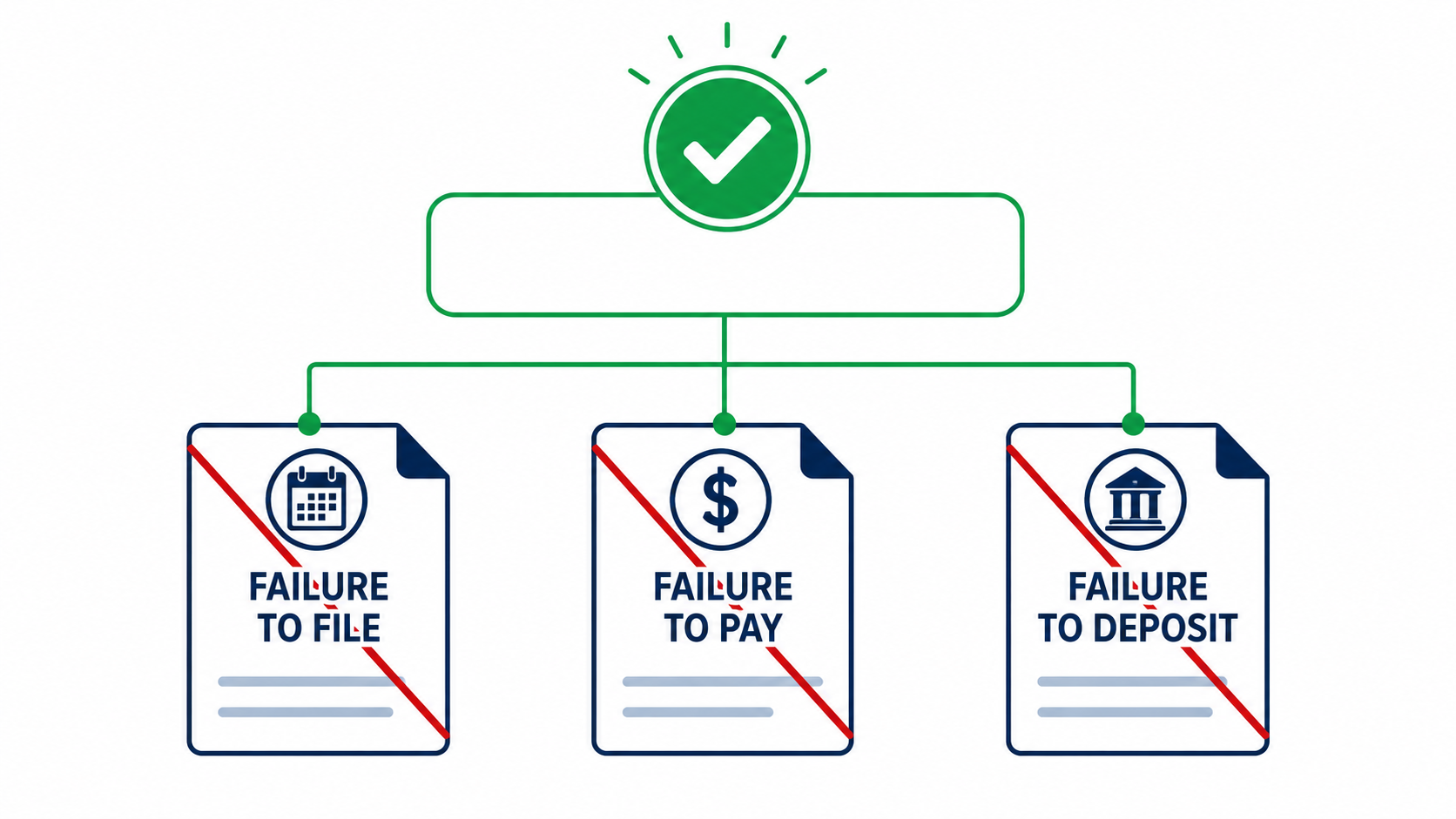

FTA applies to three penalties only:

Failure to File Penalty under IRC Section 6651(a)(1) — 5 percent of unpaid tax per month, capped at 25 percent.

Failure to Pay Penalty under IRC Section 6651(a)(2) and (a)(3) — 0.5 percent per month, capped at 25 percent.

Failure to Deposit Penalty under IRC Section 6656 — applies primarily to employment tax returns (Form 941) and ranges from 2 percent to 15 percent depending on lateness.

FTA does not apply to accuracy-related penalties, fraud penalties, estimated tax penalties under IRC Section 6654, or the failure-to-file penalty for partnership returns under IRC Section 6698. Those require reasonable cause or other relief mechanisms.

The dollar impact is significant. On a $50,000 unpaid balance filed five months late, the failure-to-file penalty alone reaches $12,500 at the cap. FTA wipes that to zero in one call, provided the taxpayer qualifies. The IRS does not advertise this. There is no notice that says “you may qualify for First-Time Penalty Abatement.” Taxpayers must request it.

Typical scenario: A small business owner who receives a CP14 notice for the first time after consistent prior-year compliance is generally a strong FTA candidate. The IRS Practitioner Priority Service handles eligible FTA requests by phone without requiring Form 843 documentation. Where FTA applies to a failure-to-file or failure-to-pay penalty, related interest is abated proportionally to the removed penalty under IRC Section 6601(e)(2).

Step-by-Step: How to Get First-Time Abatement

The mechanics matter. Following the right sequence in the right order makes the difference between approval in one call and a six-month appeal.

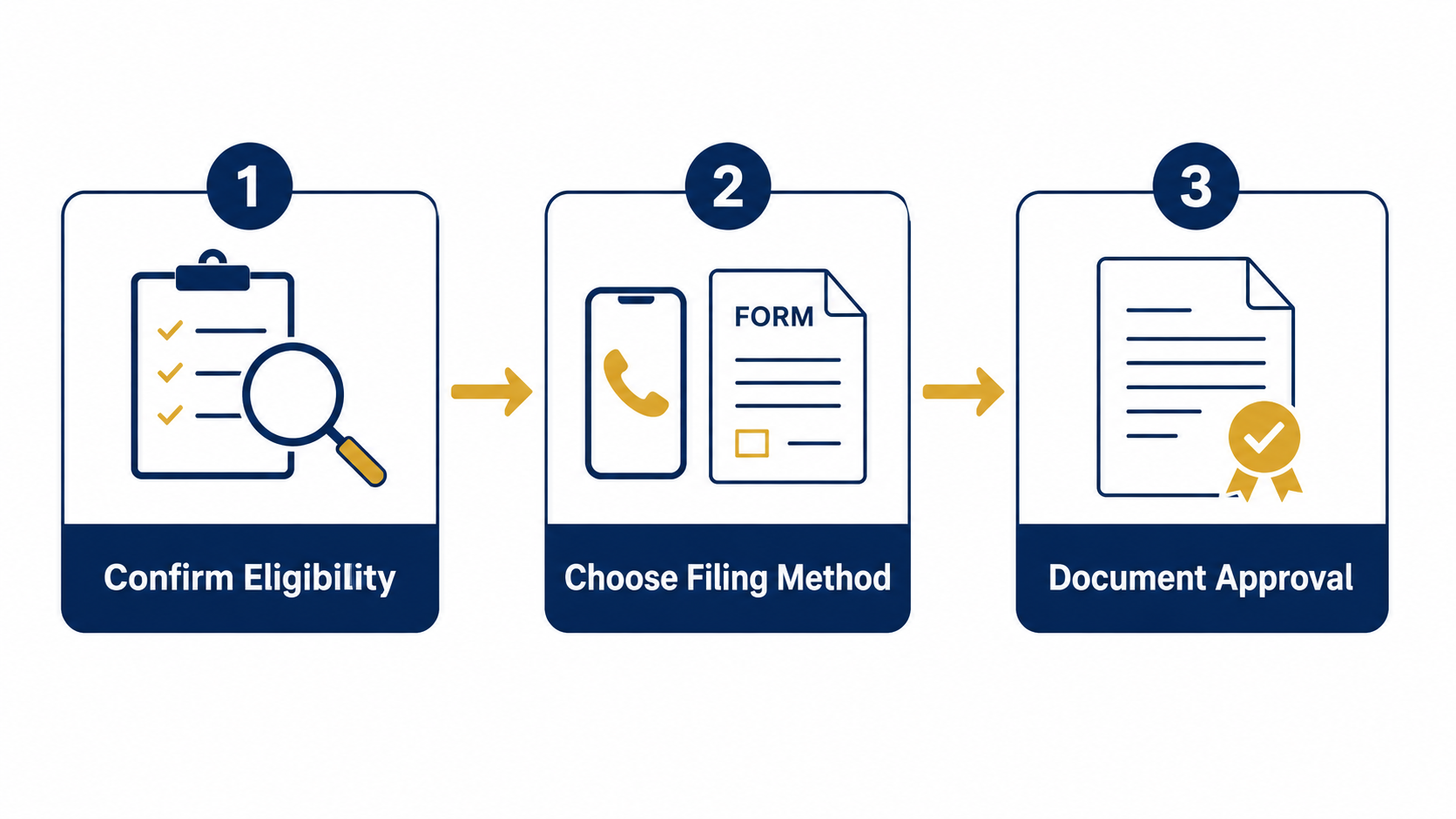

Step 1: Confirm Eligibility

Three requirements must be met before the IRS will grant FTA.

First, no penalties of any kind in the three tax years immediately preceding the year you want abated. The IRS reviews the prior three years of account transcripts. A single estimated tax penalty in the prior three years disqualifies the request. Pull your IRS account transcripts at IRS.gov to verify.

Second, all currently required returns must be filed. Missing returns from any year break eligibility. File any outstanding returns first.

Third, any current tax liability must be paid in full or covered by an active installment agreement in good standing. The IRS does not require zero balance. The IRS requires that you are working the balance.

Step 2: Choose Your Filing Method

Two paths exist, and one is dramatically faster.

Phone request: Call the IRS at 1-800-829-1040 (individuals) or the Practitioner Priority Service line if you have representation. Ask the IRS agent to apply First-Time Penalty Abatement. Reference IRM 20.1.1.3.3.2.1. The agent runs the eligibility check on the spot and processes the abatement during the call. This is the recommended approach for clean cases.

Written request via Form 843: File Form 843 (Claim for Refund and Request for Abatement). Write “First-Time Abate” at the top. Attach a brief statement confirming the three eligibility requirements. Mail to the address on the original IRS notice. Processing takes 60 to 120 days. Use this path when prior penalties exist that you also want challenged on reasonable cause.

Step 3: Document the Approval

The IRS issues a CP21 or CP22 notice confirming penalty removal. The transcript reflects a Transaction Code 270 or 271 reversing the original penalty assessment. Save these documents. The penalty assessment removes from the account, but the prior-year compliance history still counts. You generally cannot use FTA again on the same return type for three more years.

Common Mistakes That Block FTA

Self-filed FTA requests fail more often than they should. The reasons are predictable.

Mistake 1: Requesting FTA on the wrong penalty. Taxpayers ask for FTA on accuracy-related penalties or estimated tax penalties. Those penalties do not qualify. The IRS denies and the taxpayer assumes nothing else can be done. Reasonable cause is the correct path for accuracy penalties, and stacked relief strategies handle estimated tax penalties.

Mistake 2: Burning FTA on a small year first. A taxpayer owes penalties across three tax years. FTA can apply only to one year. Applying it to the year with $1,500 in penalties leaves the year with $25,000 in penalties unabated. Sequence matters. Use FTA on the year with the largest penalty, then layer reasonable cause on the others.

Mistake 3: Filing FTA before filing missing returns. The IRS will deny FTA if any prior return remains unfiled. File first. Request abatement second.

Mistake 4: Failing to verify the prior three-year clean record. A small estimated tax penalty from two years ago disqualifies the request. The IRS catches this in the eligibility check. The denial wastes the request and creates an internal record. Pull transcripts before filing.

Mistake 5: Accepting a phone denial without escalation. Front-line agents sometimes apply the rule incorrectly. If denied, request the IRS Appeals Office. Many denials reverse on appeal when the eligibility facts get reviewed properly. For the broader strategy framework, see our How to Get IRS Penalties Removed guide.

Frequently Asked Questions

Am I eligible for First-Time Penalty Abatement?

You qualify if three conditions are met: no penalties assessed in the prior three tax years, all currently required returns filed, and any current tax liability paid or under an active installment agreement. Pull your IRS account transcripts at IRS.gov to confirm the three-year clean record before filing the request.

How do I know if FTA was approved?

The IRS issues a CP21 or CP22 notice confirming the penalty removal. Your account transcript shows a Transaction Code 270 or 271 reversing the penalty assessment. Phone-based approvals process within 7 to 14 days on the transcript. Written Form 843 requests take 60 to 120 days for the notice to arrive.

Get FTA Applied Before the Penalty Compounds

Every month a penalty sits unabated, interest accrues against the penalty itself. The IRS interest rate sits at 8 percent annually, compounded daily. A $25,000 penalty held for six months adds roughly $1,000 in interest before the year ends. First-Time Penalty Abatement stops that growth and refunds the proportional interest already charged.

Tax Expert Today will pull your transcripts, verify your three-year compliance record, identify which penalties qualify, and file the FTA request directly with the IRS. Most cases resolve in one call.

Call (239) 441-2005 or schedule your free penalty review here. Tax advisors, enrolled agents, CPAs, and attorneys serving clients in all 50 states.

Published May 9, 2026 by Dr. Pellumb Kabashi « Back to Learning Center

Have a question this article touches on?

Tax Expert Today LLC, based in Naples, Florida and serving clients across the United States.

Schedule a Consultation (239) 441-2005